The mortgage business is a volume business.

Despite what borrowers may think, making home loans profitably is best done with significant scale. And if you don't have it, it is a hard barrier to break.

Gains can be hard-won, but they only seem to be minor, very minor year by year.

The best 'long-term' set of data by institution we have is the RBNZ's Dashboard data series, which has been going now for a bit more than six years. Over that whole period since June 2018, home loan market shares have really moved very little. True there are some shifts, but you have to have the full five-year-plus perspective to find them.

And the key takeaway is that the small are weak. They may be challengers, but together they are making almost zero progress in growing market share. But there is always an exception of course.

You have to look hard to find the changes.

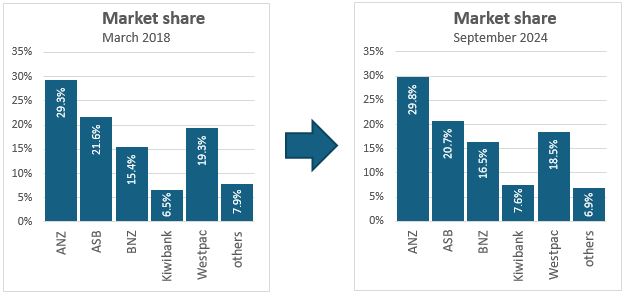

Here is a summary of the changes from March 2018 to September 2024.

| Lender / market share | 2018 | change | 2024 |

| % | % | % | |

| ANZ | 29.3 | +0.56 | 29.8 |

| ASB | 21.6 | -0.86 | 20.7 |

| BNZ | 15.4 | +1.05 | 16.5 |

| Kiwibank | 6.5 | +1.02 | 7.6 |

| Westpac | 19.3 | -0.79 | 18.5 |

| All others | 7.9 | -0.97 | 6.9 |

Over those six years, the best any bank did was to grow its share of the home loan business by +1%.

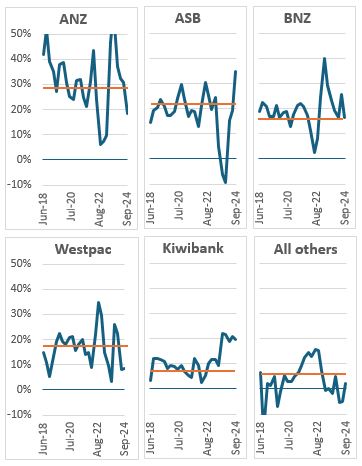

But as any manager knows, what really matters is what is happening at the end of this review period. Who has the momentum?

And here we can see that only one bank can really claim that: Kiwibank.

Kiwibank has been able to grow its home loan market share by taking more than a 20% share in each of the past five consecutive quarters. Given they have the smallest mortgage book of the big five, that is quite some achievement.

But a closer look tends to suggest Kiwibank has essentially won most of its gains at the expense of the other challenger banks.

In the charts above, the red line represents the overall embedded share of a bank's home loan business. Gains above that line means the bank is taking business from its rivals. Below that, they are ceding market share to their rivals.

These perspectives also reveal the own-goal ASB conceded when their Aussie masters prevailed on them to not chase "unprofitable business". They have had to work hard to recover from that mistake, but they are clearly not there yet even with a recent push.

The other bank making progress over the medium term is BNZ. They have the smallest market share of the big-four, but mostly they operate above the red-line, taking share from their rivals in most quarters.

But it is also clear from this data that it is hard to sustain market share growth. Do well, and your rivals respond. Only Kiwibank has been able to sustain a recent expansion - and yet the larger BNZ activity has resulted in a slightly better long-term result.

State-owned Kiwibank has a long way to go, but it does seem on a better track than most of its rivals. It certainly is batting above the average.

"More capital" is the usual (political) refrain to help them continue to become a full major. But the providers of that capital (equity market investors?) are going to want a return on their investment. "More capital" won't be available for a discounting strategy. But "more capital" will work if Kiwibank has benefits that attract borrowers other than price. (And don't forget, Kiwibank starts behind the eight-ball on average returns for shareholders.) It will be a hard-sell by Kiwibank's board to attract the capital they need unless the business itself can deliver the returns investors expect.

8 Comments

House financing may be a machine incorporating scale to achieve efficiency yet paradoxically house building remains essentially a cottage industry. It's an amusing paradox of the local property market, on the one side there is massive consolidation into just a few banks and on the other there are thousands of man-and-a-van builders.

I don't know if it's ever been different here, but there are huge regulatory requirements restricting the ability to create a new banks. Which are required given we allow banks credit creation, instead of money-lending.

But the corollary is, there can be no small local banks to grow. A finance company is a small start, but compliance/regulatory costs can be absurd, and they have no competitiveness with the credit-creators, leaving them to fight for the dregs.

If the banks actually had to lend out real money, we'd likely have a lot more - and more failures too. The rules as they are favour the incumbent.

People forget that banks are just businesses, and we enshrined that forgetfulness when we gave them credit-creation, elevating them to a special place and ceding ultimate sovereignty of our economy. Highlighted by the RBNZ's folly over Covid.

Little of this applies to a Man with a Van.

For comparative purposes, Japan has around 600 banking institutions, including both major and smaller banks. This figure reflects a robust banking landscape that serves a wide array of customer needs. Among this 600, there are approx 218 private sector banks that comprise city banks, regional banks, foreign banks, trust banks, and other specialized banks. The majority classification is Shinkin banks, cooperative financial institutions primarily serving SMEs and local residents.

OK, bigger country and economy. But if you consider that the Japanese have not been spending like drunken sailors since the 90s, it should give you a subjective frame of how competitive the environment is.

Interesting trends.

I moved to Kiwibank around Aug 22 ( when they started gaining market share) and dropped them a few weeks ago when they weren't competitive at all.

ASB this time around were most aggressive and competitive, and looking at market share over prior 12 months, it makes sense - they lost market share, then got aggressive and gained customers back in Q4. Suspect someones bonus was on the line and they decided to create a bit of competition in the market with matching any customers rate and bettering it. Highest cash back % too, with favourable clawback of only 3 yr term instead of 4.

It's a shame Kiwibank weren't able to keep me as a customer, their offer was just too low.

I'd really like to see them become nz's biggest bank.

I'd like to table an idea I havent seen before - every new kiwisaver member has a percentage allocated into a kiwibank soverign fund to help them build capital and expand. Idea being that kiwis would then own a percentage of kiwibank ( & it's returns) and their own national bank, with the idea being to get it bigger than the aussies who r&p our profits. kiwisaver in nz is still tiny at only $111billion, but even a small percentage could help kick this off. a rolling snowball gathers pace as they say..

This is a very simple story - the banks which have invested in growing their broker channels have won the most new business.

Kiwibank will keep winning so long as Steve Jurkovich is in charge

Seems odd to me. If you are going to offer competitive rates to brokers, why not offer them to the general market too? Kiwibank haven’t had good advertised mortgage rates for a while.

Kiwibank are pretty aggressive on pricing typically

The big advantage of growing the broker channel is you gain access to an additional 2000 people in your distribution network. It’s also the largest channel for new business and market share is increasing every year vs retail

"Seems odd to me. "

Brokers are dealing with the "here and now" every week/month. The "general market" is waiting for a fixed term roll over. The former is a significant number each week/month ... the latter, less so. JJ, as I said, you need to work on your mathes.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.