Kiwibank has trimmed its mortgage test rate by 50 basis points following the Reserve Bank’s Official Cash Rate (OCR) cut last week.

A Kiwibank spokesperson told interest.co.nz on Monday afternoon Kiwibank is now using a home loan serviceability rate of 8%, down from of 8.5%. The reduction comes after the Reserve Bank trimmed the OCR to 4.75% from 5.25%.

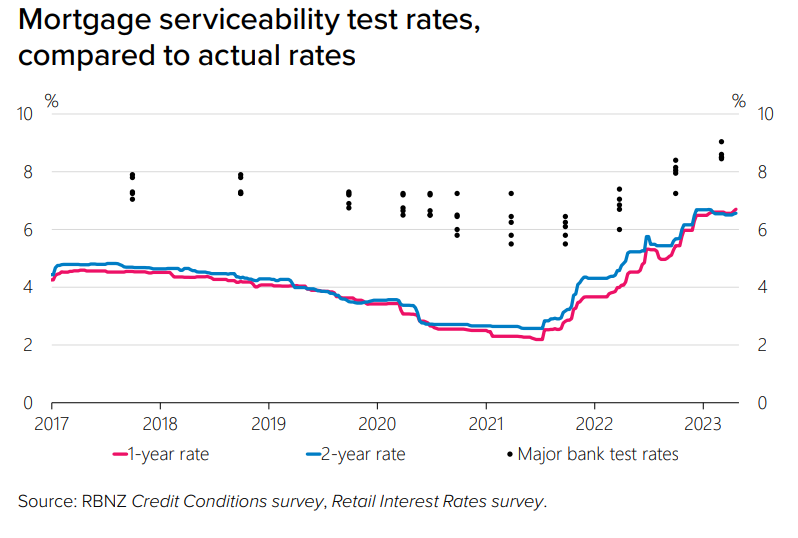

Banks use mortgage serviceability test rates to gauge the repayment capacity of would-be home loan borrowers’ if interest rates rise. A lower test rate increases borrowers' borrowing capacity.

Kiwibank had confirmed last Wednesday following the OCR decision it was still testing at 8.5%, but the test rate was under review.

Following the cut to 8%, Kiwibank appears to have the lowest mortgage serviceability test rate across the country’s five biggest retail banks. Kiwibank had home loan exposure of $26.945 billion as of June 30.

Interest.co.nz asked the country’s biggest banks last week if they had plans to review or lower their mortgage serviceability test rates after the OCR announcement.

Westpac confirmed it was planning to cut its home loan serviceability rate to 8.15% from 8.65% with the change effective from October 14.

ANZ NZ, New Zealand’s biggest mortgage lender, said last week its affordability test rate was 8.5%.

On Tuesday, a spokesperson said its loan affordability rate had been dropped from 8.5% to 8.05% as of October 15.

BNZ told interest.co.nz last week that its current mortgage serviceability test rate was 8.5%.

ASB confirmed on Tuesday that the bank is still testing mortgage serviceability at 8.7%.

“Our current test rate is under review following our recent reductions to our fixed and floating rates,” a spokesperson said.

With mortgage rates and the OCR now falling, test rates are also on the way down. However, sharp interest rate rises from the record lows of 2020-21, meant by May 2023 the Reserve Bank estimated about 25% of outstanding mortgages by value were stress tested by banks at lower interest rates than were then prevailing. ANZ NZ's test rate reached 9.1% last year, having been as low as 5.8% in the 2020-2021 period.

*The chart below comes from the Reserve Bank's May 2023 Financial Stability Report.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

15 Comments

They'd be better off focusing on a job security test.

isn't the idea of a stress test to test how you'd handle things if rates go high?

If they keep moving the stress test up and down as rates go up and down it rather negates that. Like rates are lower now so we'll lower our stress test because there no way rates could ever go up again.... yeah right.

I've mentioned this a few times on here. There is zero merit in the banks dropping their test rates, except to increase the loan book size. As we found in 2021, some banks were working on a 5.5% test rate. 12 months later those borrowers would've refixed with an interest rate starting with a 6. Incompetence from the banks.

I think the banks should have more skin in these test rates. Legislate that the stress test rate becomes the ceiling interest rate on the full loan term (e.g. 30 year) that can be charged.

Delinquencies and mortgagee sales are still fairly low so it seems that the test rates were good enough on the whole.

Isn't the jury still out on that one?

So far the only people falling over are those who have lost jobs. And test rates wouldn't have helped them.

Good enough for the bank.

How many businesses are seeing a reduction in discretionary spend as borrowers cut back on small luxuries because they're now putting say 50% instead of 30% of their pay towards the mortgage?

No legislation required if the RBNZ shifts DTIs in a meaningful way and a timely fashion.

Will they though? Who knows. Probably as per usual - always late taking the punch bowl away.

Restrictions will be light, late or removed…they’ve cooked it, as much hate as it gets on here…what will fix it (as in the numbers not the long term health of our economy)…wealth effect via house prices. They’ve left it too late & the govt with austerity aren’t playing the game…it’s an absolute f**k up…hey, hope I’m wrong, got a bad feeling I won’t be.

No, I think you let the banks be free to assess their risk. They are the subject matter experts after all, just need to have a bit more skin when making their qualified decisions. As it stands:

- Borrowers

- Losses from higher interest rates taking more of their pay,

- Extending the loan term (if not already maxed), longer loan life with more interest dollars to the bank,

- Interest only or mortgage holidays (principal amount gets deferred/still bears interest) with more interest dollars to the bank,

- Mortgagee sale = loss of deposit and still on the hook for remaining debt with interest.

- Banks

- Mortgagee sale = return of some/most money, borrower on the hook for the rest with interest.

(banks) just need to have a bit more skin when making their qualified decisions

I sort of agree, but of course the more risk they take on then the higher interest rates they'll charge to compensate. So it will be the consumers who pay. If banks don't set different interest rates for different LVRs/DTIs then it will be low risk borrowers effectively subsidising high-risk borrowers.

Higher interest rates = lower principal amounts borrowed, assuming people are borrowing to their max.

Which mathematically is a good thing, because a smaller principal amount disappears considerably faster with increased repayment amounts from pay increases.

The only issue is that notwithstanding the OBR, the banks (and lenders) probably believe they are still backed by the taxpayer. So "let's take a punt" says bank management, I'll only be here for 3 years anyway.

Fair point, i wonder what the minimum test rate is.

lots of people are locked out of buying because of the test rate, its a balance of trying to make it more affordable for people while providing them some protection, it will also be based of their predictions of interest rates.

Keep them too high and its too hard for FHB, too low and people over leverage.

I suppose uncertain times warrant a high test rate.

at that end of the day interest rates can still go higher than the test rate but it is more unlikely that mass groups of people will default.

"Banks use mortgage serviceability test rates to gauge the repayment capacity of would-be home loan borrowers’ if interest rates rise"

But hang on! Why does it matter if mortgage interest rates are going to fall? As The Banks know, "if interest rates rise", and let's add the word 'unexpectedly'. Just as they did when all and sundry were calling for (and even being told by the RBNZ to 'get ready for') a negative OCR. And what happened?

Dropping the OCR is fine IF we target any new Debt into the right, productive space. And encouraging amateur property speculation is not it; dropping the Mortgage Serviceability test rate for new Debt to be applied to buying another renter, is not it.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.