There've been a lot of retail interest rate changes recently; we have struggled to stay on top of them.

The flurry is probably not over with Wednesday's Reserve Bank (RBNZ) Official Cash Rate review upcoming and cuts a live possibility. We will have more on that on Sunday.

The changes have involved both home loans and term deposit (TD) offers, and the impetus has been led by the major banks who have had strong signals from wholesale interest rate markets, even if the RBNZ has not yet moved. Global financial markets are also on the move.

So it seems timely to take a break and assess whether any of the changes have got out of line. Have TD rates fallen faster than home loan rates, for example? Have banks used the noise to improve their margins? It's easy to be cynical and jump to conclusions that reinforce preconceived biases. But what is the evidence in the trenches?

We are in the middle of a general sinking of interest rates, so perhaps drawing conclusions now is a bit premature. Besides, individual bank rate setters not only respond to their cost of money, they also respond to loan demand, and to competitive pressures, all of which can be unforgiving.

So any analysis at this point is necessarily interim. We expect all the aforementioned forces still to be in play until well after the Wednesday RBNZ decisions.

With those caveats, here is where we stand at the end of trading Friday, August 9, comparing the current levels to a very arbitrary point at the start of the year. (There is nothing special about a January 2024 start point for this comparison).

| Carded rate offers | |||||||||

| 1yr fixed mortgage | 1yr Term deposit | Spread | |||||||

| 1-Jan-24 | 9-Aug-24 | change | 1-Jan-24 | 9-Aug-24 | change | 1-Jan-24 | 9-Aug-24 | ||

| % | % | bps | % | % | bps | bps | bps | ||

| ANZ | 7.39 | 6.85 | -54 | 6.10 | 5.60 | -50 | 129 | 125 | |

| ASB | 7.39 | 6.85 | -54 | 6.10 | 5.50 | -60 | 129 | 135 | |

| BNZ | 7.35 | 6.85 | -50 | 6.10 | 5.40 | -70 | 125 | 145 | |

| Kiwibank | 7.35 | 6.75 | -60 | 6.15 | 5.65 | -50 | 120 | 110 | |

| Westpac | 7.39 | 6.85 | -54 | 6.10 | 5.50 | -60 | 129 | 135 | |

| Ave main banks | 7.37 | 6.83 | -54 | 6.11 | 5.53 | -58 | 126 | 130 | |

| Cooperative | 7.30 | 6.79 | -51 | 6.20 | 5.65 | -55 | 110 | 114 | |

| Heartland | 6.99 | 6.69 | -30 | 6.30 | 5.80 | -50 | 69 | 89 | |

| SBS Bank | 7.55 | 6.85 | -70 | 6.15 | 5.80 | -35 | 140 | 105 | |

| TSB | 7.39 | 6.85 | -54 | 6.00 | 6.00 | 0 | 139 | 85 | |

| Selected others | 7.31 | 6.80 | -51 | 6.16 | 5.81 | -35 | 115 | 98 | |

The first point to note is the big banks as a group have hardly moved the spread between fixed home loan rates for one year and the equivalent term deposit offers. Of course, it will be less than in this table because borrowers are generally much more active in seeking and getting discounts from carded rates. This is a competitive pressure that is stronger when loan demand is weak. On the other hand, banks are very much less likely to offer 'better' term deposit rates - essentially for the same reason. So actual margins will be less than in the table.

The second point to note is rates are very volatile right now so what looks like a big move, such as for BNZ, will likely close up quickly.

The third point to note is challenger banks seem to be being squeezed. They are in an uncomfortable position, suffering narrower spreads and writing much smaller loan volumes. It's not a recipe for making market share gains from strength. And among the larger banks, it's Kiwibank that's in the tightest position on this front.

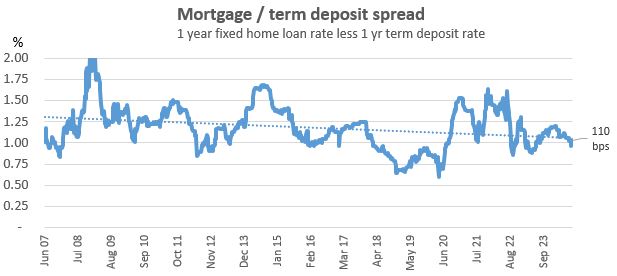

Differences from the start of the year are one thing. But how has the overall banking sector fared over the long run? How do current spreads compare since, say, the Global Financial Crisis?

The basic answer is they have been in a long-term narrowing trend.

This chart tracking is actually measuring things slightly differently to the table above. It uses simple averages of all banks, not just the ones in the above table. And some small outlier banks often have uncompetitive rates for longish periods. And some banks come and go. HSBC as a retail bank is no longer active. Heartland and others have arrived over the longer period of the chart.

But even with those caveats, it is clear that bank margins are thinning. That is not so tough on the banks doing high volumes of transactions but it is very tough on those not.

So, now when we draw 'conclusions' about bank margins, we have some recent and long-term data to base them on.

For example, if you were a shareholder in Kiwibank, would you risk substantially more capital into a sector where margins seem to be shrinking in the business lines you need to grow, like retail mortgages? Especially when you know your four larger competitors are going to fight to hold or grow their share anyway?

35 Comments

How convenient the Government has floated the idea of selling Kiwibank. On the interest front, for those like myself with TD's, of which this investment type has been labelled by some in derogatory term, is it not financially reassuring to be receiving it than to be paying it? Granted that a mortgage is largely unavoidable and a pathway to full house ownership, speculating on quick gains using others money has got us in this mess. I remember when saving was encouraged and examples of compounded interest went up on the blackboard.

Some of my TDs will be cashed in within 6 months as I carry out a $300k renovation that kicks off next week. In the spending the $300k I will create jobs. But mostly, I'll be 'creating' something - a vastly enhanced asset - that currently doesn't exist. The return from this enhanced asset will last many, many years and will contribute to further 'creation'.

Compared to a TD, this activity - primarily an investment activity - helps NZ Inc far more than 'putting money in the bank' for a tiny real return so the banks can fuel the housing ponzi and make billions in profits that get shipped overseas. So yes, I don't have much time for TDs.

Our TD's come out over two months post Christmas. We are seriously looking at spending some on upgrading to another residence. There's real weakness showing up in the upper brackets and we intend to take advantage of this.

Exactly RP, so as TD's become less attractive, houses become more attractive, up go the prices!

"TD's become less attractive"

For some TD's will always be attractive. In our case we want to enjoy the rewards for living within our means. We've saved plenty - the time is approaching to spend some.

Well done for highlighting how ignorant Kiwis are when an "investment" is considered. (The annualized ROI of residential property is only a tiny bit better than TDs unless the land on which the property sits appreciates significantly due to ... well ... you know the three rules: location, location, location.)

We're really not that bright, are we?

Like many investments, there's nominal gains to be made passively investing.

But a more involved property investor can make significantly more than the market "average". There's no scope with a TD to make any more than the retail rate. You then need to move onto riskier propositions.

Good on ya, mate.

I saw this without knowing anything about your current house so take it more as a hypothetical.

If you accept that the super rich (you and I) already consume more than our fair share of planetary assets, don't you think using resources to add even more 'luxury' to your current lifestyle is really a wasteful use of limited resources?

Like I said, this is more a hypothetical/philosophical argument rather than a criticism of your personal choice to renovate.

If we actually took our morals seriously, we should be living in a tent and volunteering all of our spare time.

Instead if we buy an electric car, donate some crumbs to a charity, and get angry that the governments not fixing everything, we can pretend that's anywhere close to doing enough.

.

I do kind of agree with you, Agnostium.

It's a rental - great location for schools, supermarkets, healthcare and all within walking distance. I'll be bringing up to date (lots of insol) and adding a bathroom, a new kitchen and a bedroom with the old kitchen being converted into another bedroom. The existing tenant (a plumber), who has been there forever, is bringing in two aged relatives and we've been talking about this reno for a few years now. My ROI on the reno money will be about 6.5%. Not huge. Well, that is until the tenant's kids finish school/uni, and the tenant heads back to the provinces and a new tenant enters at market rent.

I'd prefer to bowl it and provide far more dwellings but Council's daft zoning rules prohibit anything except a single dwelling at this time. Given it's location, with excellent walkability, our footprint on the the planet would be less if it weren't for Council.

So, a thought for you: Who elects the Council and sanctions their daft zoning rules?

All the inferiors you have to share society with?

I'd take some of that immense wealth and use it working out how to enjoy life a bit more.

People will do all kinds of mental gymnastics in order to justify spending money.

And on the other side of the coin, people likewise engage in similar mental gymnastics in order to justify not spending any money.

I spose if they don't have the imagination, they're not able to dress up self interest enough to sound like it's anything but.

We should cut the pension for rich retirees to help pay for the large fiscal hole we have.

CTP 🎬

I'd say the voter mandate for that is a while off.

If anything I think the wealth disparity is higher than ever, with youth and middle class families feeling it hardest.

Why should a 70 year old multimillionaire get free money from the current taxpayers. Let’s cut the burden off now.

I don't disagree that's a reasonably quick way to reverse some unnecessary spend.

I'm just saying though, such a thing only occurs with the political will, and it's not a measure larger parties will want to touch until the demographics made it less unpopular.

Until the young and middle-aged voters actually engage in politics with critical thought of their own, as opposed to what hey see in the news or are told by family and friends, or the number of baby boomers declines, I can't see it happening.

Oh they're engaged for sure, unless you're suggesting young and middle-aged voters quit their jobs and all vie for a career in politics?

Otherwise, they can only vote for what's on offer. Or protest I suppose?

CTP 🎬

As a voting force this age group is expanding fast. For the sake longjohndrop aspirations, Government will need to act on this problem group two decades ago.

Regardless of what my position might be when it happens, I'm not planning for the government to be pitching in much at all.

Ditto.

But at what point does this taxpayer say it’s enough. When tax cuts are $2-20 per week for the majority of households, why should a multimillionaire get $500-900 per week for free.

Its pretty simple

I don't take the pension as it puts me in higher tax bracket so I'm doing the right thing if that's what you are implying, Maybe if you drop our tax rates after 65 years old we would more likely not to take the pension so would that help. I worked extremely hard and paid a lot of tax so why would I not be abled to collect the pension, thats how the system was designed, Maybe the people who didn't pay much tax shouldn't get the pension either. In the end we all seem to get the same pension ,is that fair.

That is the right thing to do. If you do not need the pension, then you shouldn't receive it. Certainly if somebody is still employed, then they're not retired so why should they receive a benefit? A person's costs don't magically go up $20k p.a. overnight when they hit 65. Your thinking is quite common from the Boomers, that the pension is some loyalty rewards scheme and your comment about people who have paid not as much tax shouldn't get it really shows this.

Sorry to say, but there's nothing special about paying tax all your lives. Most people will do this. The more you pay is not because you necessarily worked harder than others, but you were graced with fortune that your skills were remunerated more handsomely than the folk down the street. For example, I pay more tax than a nurse yet I work from home 8 - 5 sitting at a desk. Yet by your logic the nurse should be less entitled to the pension????

The pension is not a loyalty reward scheme for tax payers. Couldn’t agree with this more.

"individual bank rate setters not only respond to their cost of money, they also respond to loan demand, and to competitive pressures, all of which can be unforgiving."

Bingo!

In essence, the lower rates go, the more the banks try to lend out, but if borrowers don't see and economic return on the risks associated with that, they won't borrow. And so they won't buy - anything.

And it all boils down to not being about the amount of Debt we have, but what we do with it. Change that and drop the OCR to 0% if you like. But make sure our collective Private Debt is redirected away from its current application.

What is the banks return on capital? That’s the test.

if there are better margin in say farm lending, why don’t Kiwibank get into that sector ? Can’t at the moment as insufficient capital.

The spread is interesting but isn’t fractional lending much more significant when comparing TDs to mortgage rates?

For me, what I’d like to see spread to wholesale rates over time. Which bank has the lowest spread etc.

The lending comes before the depositing. (Which is why, for me, Inflation is an expansion of the money supply caused by new Debt. The CPI isn't a measure of 'Inflation'. It is an Index that measures the Price Changes caused by Inflation (of the money supply)

"When a loan is made by the commercial bank, the bank creates new demand deposits and the money supply expands by the size of the loan....A country's central bank may determine a minimum amount that banks must hold in reserves, called the "reserve requirement" or "reserve ratio". . Some countries, e.g. the United States, the United Kingdom, Canada, Australia, and New Zealand, and the three Scandinavian countries, do not impose reserve requirements at all."

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.