The number of home loan borrowers switching banks is rising.

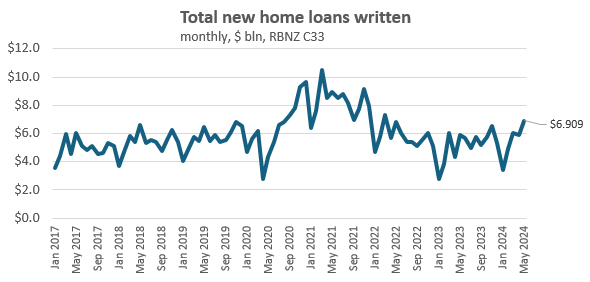

Banks made $6.9 billion in new residential mortgage lending in May, the most in two years. In the longer term perspective this isn't that special. But of some note, this was driven by borrowers changing banks.

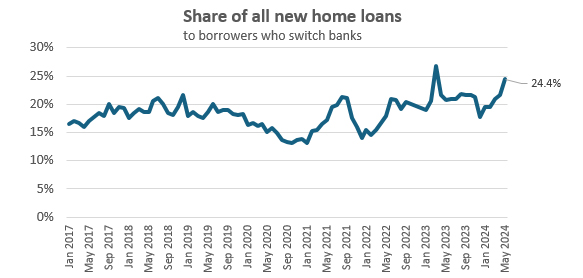

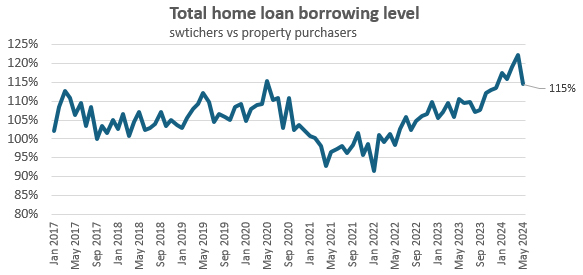

In fact almost a quarter of new residential lending by number were for these switches (ignoring top-up activity), near the highest level since this data series started in 2017. (On the other hand, loan top-ups remained little-changed at about 11.5% of all new lending.)

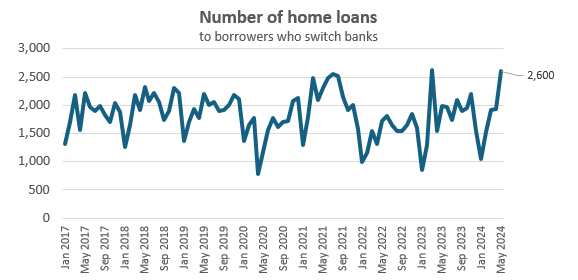

In May that involved 2600 borrowers who switched (just shy of the March 2023 record high) ...

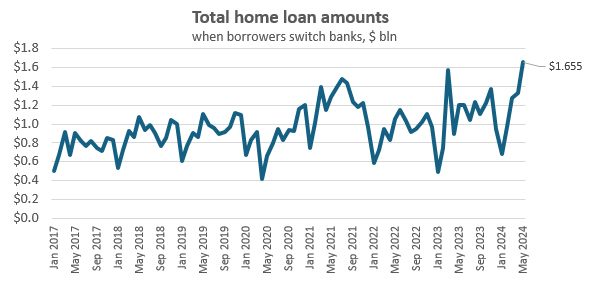

... and they switched $1.655 billion in loans ...

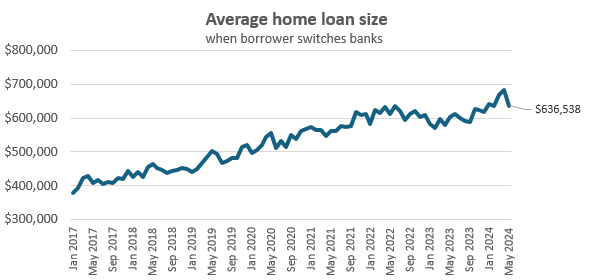

... at an average mortgage size of $636,500.

That was 15% higher than the average loan size for new borrowers taking out a mortgage for a home purchase.

In the post-Covid housing market boom, the total number of borrowers who switched banks peaked at 25,700 in the year to October 2021. The impetus to switch fell away and quite quickly, retreating 30% to 18,200 in the year to January 2023. But since, as household finances and job prospects combined to squeeze personal budgets, it has risen steadily to be up 23% to a 22,400 annual rate of home loan switching. That is a sizeable pool in competitive play.

But it would also be fair to question that explanation. Home loan borrowers are staying with short fixed terms. And the interest rates on short fixed terms (six to 18 months) are far higher than for fixed three to five year levels. A lower rate would give a lower mortgage payment, so are borrowers really chasing that?

(Opinion: I have suggested elsewhere that the shorter terms and resulting higher churn might be related to the rise in mortgage broker activity and advice. Readers can draw their own conclusions on that. Hopefully the regulators, the Financial Markets Authority and the Commerce Commission, are looking at this too.)

8 Comments

Customers are chasing the cash backs plus trying to pull equity out of their houses to pay for living costs.

The good news is that they still have enough equity to change banks.

It would be interesting to see if people were switching between the big 4 or switching to non banks.

I’m still deeply confused about how these numbers work.

surely switching banks nets out to zero on the lending stats?

what am I missing ?

It would net out to zero in total lending (assuming same amount repaid as reborrowed), but new lending stats see the switch as a new mortgage created and thats all that is counted.

Thanks for the clarification.

Ha the obligatory crack at mortgage brokers at the end from David as always.

David, so I don't get it - you're saying that there has been more competition in the banking sector, and likely due to Mortgage Advisers 'churning' business, and yet your last comment insinuates this is a bad thing and that the FMA and Com Com need to do further investigation.

Yet it's as clear as day that MA's are good for competition and are favoured by consumers. After all, if consumers didn't like dealing with MA's they wouldn't be increasing in market share.

Do we collectively trust the banks to just keep dropping mortgage rates and offering recurring retention offers to their borrowers without any pressure?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.