TSB is growing commercial lending to the likes of property developers and lending to small and medium sized businesses (SMEs), as it also strives to hold its share of the housing lending market, CEO Kerry Boielle says.

Speaking to interest.co.nz after TSB posted a 71% surge in March-year net profit after tax to $34.04 million as expenses tumbled, Boielle says the bank's looking to support the "smaller, early medium end of the SME market."

"That's something that our customers tell us, actually, 'we'd love to bring more of our business banking to you if you could fill this product gap.' And so we're focused on filling those gaps at present and engaging more with that SME market," says Boielle.

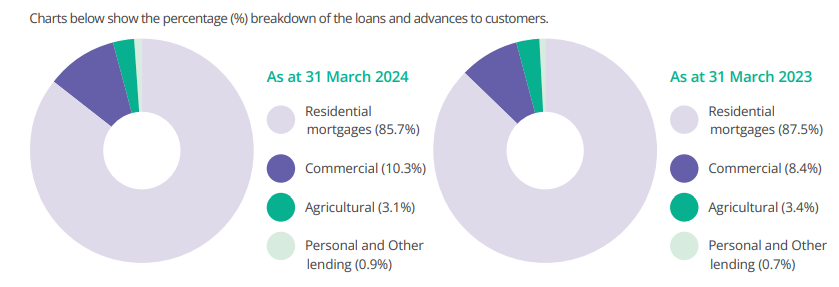

This, she adds, is helping lift interest income after net interest income fell $1.8 million to $185.770 million in TSB's March-year. Commercial lending, being business loans and commercial property lending secured by residential or commercial properties, grew $176.620 million, or 30%, to $769.891 million. That means it was 10.3% of TSB's total lending at March 31, up from 8.4% a year earlier.

"We've started to grow into commercial lending, property development, some of those areas. But it's really important that's done in a way that is digestible and you don't try and do too much too fast," Boielle says.

As of March 31 TSB's housing lending stood at $6.4 billion, having risen $186.122 million, or 3%, year-on-year. However, it dropped to 85.7% of total lending from 87.5%. Whilst "a little bit of the share in our balance sheet" might shift, Boielle says TSB doesn't want commercial lending growth to come at the expense of existing customers and current housing lending market share.

Reserve Bank data shows system-wide housing lending grew 3.1% in the March year.

Meanwhile the agriculture sector is not a focus for TSB.

"That is not an area of expertise for us. And being a smaller sized bank, we can't be all things to all markets," Boielle says.

'Resetting to move forward'

TSB's annual net operating income fell $11.756 million, or 5.5%, to $201.165 million. On top of the decline in net interest income, other income dropped almost $10 million, or 39%, to $15.395 million. The bank's annual net interest margin was 2.02%.

Boielle says income is on the rise again this financial year. TSB has been doing what some other banks have been doing in terms of moving away from insurance and wealth and more to core banking, thus the drop in other income.

"Our interest expense was higher last year as well, led largely through changing some fundamentals in our balance sheet and how we hedge and so [there was] some resetting to move forward," she says.

TSB says "market factors" had an impact on revenue over the past year. As interest rates have risen from their Covid-19 lows, depositors have shifted money into term deposits and savings accounts from transactional accounts, thus lifting the bank's funding costs.

"Covid also saw a breakdown in the historical relationship between wholesale and retail rates, which has normalised over the last year or so. This created some timing issues with the accounting for our hedges, providing a benefit in prior years which has equalised over full-year 2024," TSB says.

'Right sizing'

The bank's annual operating expenses tumbled $36.994 million, or 19.5%, to $152.317 million. Boielle says this was due to TSB "resetting the cost base to a more appropriate size and structure going forward." The last few years have seen investment in "legacy gaps" such as technology and compliance programmes.

"We filled some gaps and now we're right sizing ourselves going into the future."

The "right sizing" included shutting seven branches last year and another couple recently, meaning TSB now has a total of 14 branches.

"Running branches is expensive. There's a lot of security required, there's the bricks and mortar of that," Boielle says, plus leases, property maintenance, the expense of holding and moving cash. Transaction volumes are down significantly at branches, she adds, citing the example of a 55% drop at one branch. Investment and focus has been shifted into technology and customers' digital experiences. Some branch staff were redeployed to TSB's contact centre, while some were let go.

There are no shot-term plans to close any more branches, she says.

TSB recently hired Roxanne Salton as Chief Digital Officer. Salton comes from the same role at Southern Cross Health Society, from where Boielle joined TSB as CEO in January, succeeding Donna Cooper who left last June. During the March year five directors left TSB's board and three new directors joined.

The key for TSB, Boielle says, is being big enough to have a broad range of products and services matching what's on offer at the big banks, whilst being small enough to provide genuine personal service that cares about the customer getting the right outcome.

"So it's being the right size, I think, for the business. Perfect amount of bank, we call it."

Shareholder wants higher RoE; CCCFA court date

Although TSB's annual return on equity rose significantly, it was still only 4.6%. Boielle says shareholder Toi Foundation Holdings wants to lift this to its cost of capital, which is significantly higher than the current return on equity, and an "appropriate return."

"They're wanting to make sure that that's done in the context of long term growth. So our business would acknowledge that our return on equity is not where we would like it to be. We have plans to lift it, but not knee jerk plans. We've got a long term build and grow strategy which our shareholders are supportive of. And I'm confident we'll see that lift year on year on year to get us more in line with our peers."

Having self reported historic consumer credit fee issues to the Commerce Commission in 2022, the consumer watchdog filed civil proceedings against TSB in May alleging breaches of the Credit Contracts and Consumer Finance Act (CCCFA). TSB has admitted the claims, and civil pecuniary penalties will be decided at an August court hearing.

"We've worked with the Commerce Commission over an extended period to get right into the detail. They are all relating to historical fee issues that occurred a number of years in the past," says Boielle.

Customer remediation has been undertaken under the guidance of the Commerce Commission, with the issues relating to consumer and residential mortgage lending, in terms of "the way fees are calculated, the way they are required to be calculated, and evidenced and worked through."

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

5 Comments

TSB is heading in the right direction but they are right now the worst of both worlds - too small to have a meaningful product portfolio or great digital experience (e.g. PIE funds, mobile app that works, competitive mortgage rates) and too big to have decent service - 20 min hold times are pretty common now to talk to someone. ANZ and ASB are generally under 5mins once you get past all the number pushing and disclaimers.

I hope they succeed for New Zealand's sake, they are what Kiwibank never became.

Would be brilliant to see TSB and Cooperative Bank do to the banking sector what Southern Cross has achieved in the health insurance space.

Imagine how different our economy would look if community-owned providers dominated these lucrative markets instead of foreign-owned players.

Fantastic bank that wants to support business.

Well done take the lead TSB now up to all New Zealanders to support them.

I am one of those NZders and I have nothing but praise for the way they run there business.

Looking like very strong leadership now something positive for Kiwis at last well done TSB.

I've been supporting TSB and Heartland for the last 6 years. I try and not use the aussie banks for anything as I believe they are fleecing their customers. They have made improvement in their products and mobile apps during the time and are competitive with ANZ for an everyday kiwi. Great to hear them looking to support commercial and SMB.

My home loan has been with TSB for more than 5 years and they have always been super helpful and flexible, and always provided a great rate. Granted ive had 60%+ equity for most of the time. But getting additional revolving credits setup etc has never been difficult.

Phone service has got worse but leave your number and they call back quickly. And always amazingly personable.

Gaps... They dont have a japaense yen settling account which is a pain. So I have to use a big bank for that. They dont have a good PIE savings account. Their term deposits are not that market leading.

I fill their gaps with Heartland for short term savings. Its difficult to beat their call account or their 32day saver.

Good post. TSB is a good bank indeed. Maybe they should try and merger with the likes of Heartland in order to create a mid-range bank able to meaningfully compete with the AU banks ?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.