Our first article in this series highlighted how much banks pay mortgage brokers for the business they funnel to them.

Now we want to take a slightly deeper dive into these flows.

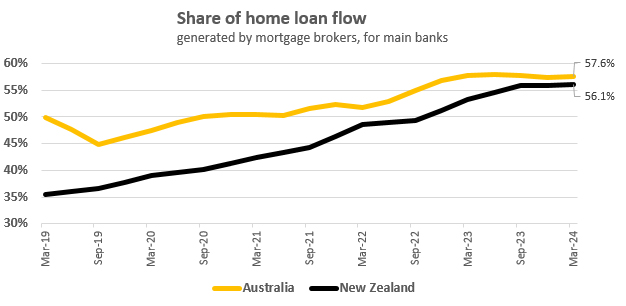

It has long been assumed 'Australia' is a broker-dominant home loan market and 'New Zealand' isn't. But from our recent dig into bank-disclosures, this no longer seems to be the case.

Transparency varies between institutions, but we are fortunate the largest New Zealand bank, ANZ, is very transparent in these matters on both sides of the Tasman. BNZ is similar, as is its parent National Australia Bank. ASB is very opaque, but its parent, Commonwealth Bank of Australia, is as transparent as both ANZ and NAB. Westpac gives limited visibility. Locally Kiwibank is yet to step up although it says it will. But at least it's better than laggard ASB.

From these disclosures we found there has been a rather rapid rise in the role of mortgage brokers here, to the point where the difference with Australia is small now.

Over the past five years, the broker share has basically risen ~20 percentage points from about 40% to nearly ~60%. We think Kiwibank has outperformed that 'growth', rising by ~25 percentage points from 37.5% five years ago.

A key reason for this overall drive-shift has been the appetite of ANZ for more of their home loan business to arrive from brokers. This has given the market shift some significant heft. Westpac has been the other driver, somewhat surprisingly, but probably because its in-house channels underperformed.

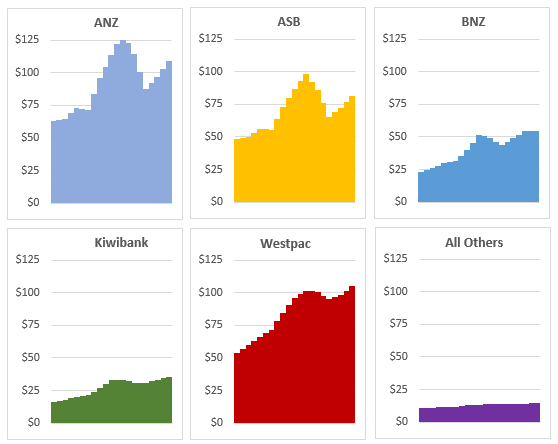

The following chart-set tracks the dollar commissions each main bank has probably paid to mortgage brokers for the business they refer. All are estimates, some tighter than others for the same 'transparency' reasons noted above. We will update these estimates as better sources reveal themselves in the future.

($ million, at annual rate, quarterly to March 2024)

Of note is that both Kiwibank (~62%) and Westpac (~61%) now basically match ANZ (~61%) in terms of their flow coming via the broker channel, that ASB is probably the highest (~66%), and BNZ is lagging (~47%).

On that basis, both Kiwibank and Westpac had record-high broker flows in the March half year.

The data also shows the period when ASB pulled back from home loan growth after their masters at CBA became uncomfortable with them writing business that was not profitable. They are now back in the market however. Even though it didn't garner headlines at the time, it seems ANZ pulled back similarly at the same time for the same reasons.

ANZ and Westpac are the two banks likely to be paying more than $100 million per year to brokers.

Now that the Kiwi broker channel is beefing up and looking more "Aussie," it's attracting the attention of the Australians. Although the big Aussie broking channels are not here in force yet, its peak body, Finance Brokers Association of Australasia, has arrived hoping to roll up the local industry into one larger and more persuasive advocacy force. (It will be no surprise to learn that the 11,000+ member FBAA is based in wide-boy Queensland).

FBAA has a compelling pitch; "protecting the future of our industry and dealing with regulatory matters of the day." FBAA's "proven track record" of batting back Australian regulatory restraints has been successful. After all, none of the substantive reforms recommended in Australia by Hayne or the Australian Productivity Commission, not to mention Trowbridge, have succeeded at the political phase, all due to effective lobbying.

Here freedoms to operate are limited by the financial advice regulatory regime overseen by the Financial Markets Authority, with financial advice provider licensees required to file their regulatory returns by 30 September.

New Zealand brokers are also facing sceptical assessments by our Commerce Commission. Thus local mortgage brokers are likely to welcome FBAA's help here.

*The Financial Advice regime came into effect in March 2023. The FMA’s Financial Advice Provider page has more information that could be useful too. As mentioned, all FAP licensees need to file their regulatory returns by 30 September.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

35 Comments

Any idea what the percentages of the loan cost these numbers represent, plus the effect of trail commissions.

At 350M, we have some pretty decent sized businesses clipping the ticket.

Good question, RBNZ data show total interest income by banks is $10,731,000,000, so $350,000,000 is 0.033 (3.3%). However, if we assume all commission income related only to residential lending (which is not entirely the case), that would be 350/5103 = 0.069% (6.9%)*

https://www.rbnz.govt.nz/statistics/series/registered-banks/banks-incom…

Therefore mortgage advisers make up circa 30bps* depending on how you measure it, but this includes origination and management. If the entire industry disappeared, how much would you trust the banks to drop mortgage rates by 30bps and following on from there, is there a better outcome for consumers?

There are approx 2,000 (reasonable estimate) advisers + 2,000 (poor estimate) support staff in this industry not including costs to operate. Can be profitable, but majority of businesses have <10 people in them. There are only a handful of large operators.

*edited

Your calculations are out by a factor of 100 (should be 3.3% and 6.9%) but I'm not sure that can be directly translated into the bps addition to the rate. I've never had a problem negotiating MA-equivalent rates or better by dealing direct with the bank, although it does involve a level of persistence that many would not be able to muster.

There is a place for MAs when it comes to helping first-timers and the less forthright into lending, but once people stop thinking the bank is doing them any favours by gracing them with a massive debt, and start realising they're the customer who is gracing the bank with a massive asset, the value of an MA in the equation sinks dramatically.

You're right sorry. 3.3 - 6.9%, then to multiply by the average mortgage rate right now of say 6% (600bps) (across all current fixed terms), that's approx. 30bps of the mortgage rate.

Mortgage rates should be the same across all channels, but you'll find no MA differentiates themselves on rates as ultimately that's not why people work with MA's. If they do, they could very easily just do this themselves directly at their bank. Data obviously shows that circa 40% of people still do that.

However, where the bank have added operating cost for MA's, they've reduced operating costs by removing excess bonuses from bank lenders and culling back branches. If we then measure the net cost of MA's as a distribution channel that would lead to a different outcome. I wouldn't be surprised if the banks in the end save money through all this.

once people stop thinking the bank is doing them any favours by gracing them with a massive debt, and start realising they're the customer who is gracing the bank with a massive asset, the value of an MA in the equation sinks dramatically.

Love this. A buyer goes to the bank and asks them if they would allow the buyer to make the bank profit over time via interest. Sounds like the start of a joke but is the reality.

I wouldn't trust the banks very far to drop the 30bps if the industry disappeared.

I would certainly trust them to add on a further 30bps if the 40% who still deal direct with a bank started going through a broker though.

It's an industry which exists, isn't entirely without utility, but there is definitely an issue with ticket clipping, and much like REA's I see absolutely no justification for commissions to be based on % of the loan size.

You are missing the simple fact that the banks would need to employ more staff to do the work that MA's do for them, so your numbers are wildly inaccurate

KB's number most likely include their own NZHL as they have on their books only 400 advisers now, most of which were onboarded mid to late last year.

All this shows, is that consumers prefer working with Mortgage Advisers rather than the bank directly more than before. It promotes competition and leads to better outcomes. There is not a single bank that will say, "forget applying here, x bank is more competitive, apply there!".

The higher the proportion of business that comes from independent channels, the more voice advisers can have to influence the banks. Industry advocacy has for a long time been very poor for MA's so individual advisers are compensating by speaking up themselves.

Note, the 'skeptical assessments' by Comcom have been apologized for publicly by its Chair. They've since engaged the industry to learn about it rather than read about reports from offshore to make an assessment.

The problem is that the broker commission is paid by the successful bank yet the mortgage broker is supposed to be acting in the best interests of the borrower. Australian Royal Commission was going to address this obvious conflict of interest and require the borrower to pay the commission. The howls of protest to the liberal government from the property/broker industry were so deafening, because they knew that borrowers would not want to pay (even though they're still paying for it via the bank margin), that recommendation was ignored.

I find it quite confusing as to why David has it in for mortgage advisers, we contract to the banks to do their work for them, yes they are paying advisers more but I bet their staffing levels (particularly branch based lenders) have fallen to match. Our clients are generally better off by using our services, both in price and knowledge as to how to repay their mortgage faster. How can a free service that educates people on how to save money at the bank be a bad thing?

But it's not a free service. The banks aren't just absorbing the cost, they're passing it back to the customer. Go around the adviser some time and try it out. Worst comes to worst you fail, then go to an adviser afterwards.

BNZ tried out the direct service as did HSBC. How did that work out I wonder, maybe consumers are waking up to the fact that the management of the home loan can change the costs. Buying a property safely has an impact. All of this advice is required. The clients are voting with their feet.

Buzzwords and waffle.

The service was direct for over a hundred years before MAs came along. MAs basically replace the front end lending clerks that existed in-branch before the more centralised operating model used by banks today was introduced.

I'm not sure what you mean by buying a property "safely." The bank must be satisfied the debt is manageable before any lending contract is signed, but their decision is based on information passed to them via the MA, which from experience can include some creative accounting.

Now rather than dealing with a clerk at a bank, the best bankers have all left to become MA's. Clients now have a better service, better experience and are voting with their feet as Hamish says.

Buying a property safely refers to the advice surrounding the purchase. Yes banks do a stress test, but they do not advise a client around their property purchase, their circumstances, whether it's suitable to buy that first home/IP/etc. in their situation.

It's the same thing as taxes - people are entirely able to file and submit their own tax returns, and for most straightforward situations it's not overly complex. Yet, people still employ accountants to get it right and to make sure they file their taxes 'safely' - is the entire accounting industry redundant for that reason?

As a result, through COVID, mortgage borrowers (particularly those who worked with advisers) are better off and have withstood the conditions.

Sounds to me though, you've had a bad experience with one MA and now painting the entire industry with that brush.

And how do people pay their accountants? Via an hourly rate. Imagine if an accountant charged a percentage of the tax. If MA believe their service adds value, then there should be no problem getting the customer to pay for it. This whole 'saves time for the bank' thing is spurious... someone still processes it back office, and customers still want to be able to walk in to a branch from time to time, so they need to exist still.

Correct me if i'm wrong, but if the bank is paying you then isn't the bank your client and not the borrower?

@Te Kooti Yes it is a bizarre situation and we have to walk the tightrope of duty of care to both parties but the strong emphasis is to the person borrowing the money. We are dictated by the FMA to do the right thing by the borrower and have to show that we do that when they do file reviews and the banks do reviews as well to make sure we are doing things by the book too

Thanks.

I'm all in favour of mortgage brokers even though the current model is conflicted. Then again, would borrowers actually pay for the service, possibly not? In fact, housing in general is a giant web of conflicts, agents, developers, media....

Even beyond the base conflict of who pays for the service.

The remuneration structure only further enhances this.

Why is the commision based on a percentage of the loan amount? To encourage brokers to bring in larger loans to the bank surely.

Commission's are always used to incentivise sales are they not?

Understand your issue, but 1. By extension should the bank not make more money on a bigger loan? and 2. What is the alternative?

As a mortgage adviser I also do a lot of top-ups for $10k-$20k which pay me less than the minimum wage for the time spent. It is not all rainbows and skittles

Rubbish argument. The bank holds more capital on a larger loan (if you dont know that, I worry about your advice!), so obviously the interest income needs to be higher. And, as you no doubt know, there is an expectation of a lower margin on a larger loan. I'd certainly negotiate harder if my loan was double.

Commission encourages people to borrow more than they need, and then MA have the nerve to on-charge clawbacks if the loan repays. The alternative is a cap on commissions and/or a set hourly rate the customer pays - like they do to accountants and lawyers. On the matter of small top ups, if you're getting trail commission, you're getting paid most of the year for nothing, so sure you can swing a free top up. Or, charge an application fee.

@ General Comment That's incorrect, adviser clients generally get better interest rates than if they go directly, not all of the time but most of the time. Its a fallacy to think that the lowest rate is the best way to save money on a mortgage, that's where advisers can help clients save money too

So my MA was right and I should have fixed my loans for 1 year, 2 and 3 years in May 2021, not all for 5 years like I insisted because it was blatantly obvious by then what was going to happen? I should have just taken the higher rate over that 5 years rather than push my MA to get the extra 20bps off because...?

Clients are often getting better rates through MAs because the industry has adopted the Apple mantra of creating a niche product then convincing people they need it. If more people dealt directly with the banks and backed themselves then they'd be getting the same or better rates direct.

There's no magic involved in paying off a debt quicker, no secrets, no cheat codes, it's simple mathematics.

Everything is blatantly obvious after the fact :) You seem to be of the view that all banks are the same which they are not, there are some products that suit a client's requirements considerably better than what some banks offer.

I price check our adviser from time to time and I can usually match them but for me, it's less about price and more about the admin they take off me.

I rate our mortgage adviser and having dealt with BNZ/ANZ directly for our lending, the pace that our adviser can push things through is superior to the service I can get out of the banks directly, that's not worth nothing.

Also being able to pick up the phone and say I want to do xyz, and leave them to come back to me with a result is preferable, than having to chase my application with the bank.

Source for this comment please?

While I get the sentiment, as every business has to pass on their costs to the clients. Have you done the costings around what has a higher cost, i.e. mortgage advisers Vs additional staff, branches etc. I guarantee the banks have.

I think it's similar to insurance advisors. One good thing IAs and MAs can do is to help clarify information on options and choices, which is otherwise difficult for an individual v. a bank, where there is a clear information dissymetry.

Having said that, the cost of the service and motivations will always be a challenge. I've met some great MAs, but still looking for a good insurance advisor.

Interesting to take the gross amount, I wonder if you would also include the interest receipts instead of the profit that banks make, when writing about banks. You do realise there a cost to deliver the exceptional service most of use deliver as mortgage advisers.

I wonder if many aren't ex-bank employees that hit a pay-ceiling and then became part of the bank's casualised workforce. I.e. some 'brokers' are little more than tied agents.

The fundamental problem with the RBNZ is by definition they don’t want a bank run on their watch so they become paranoid obsessed with caution and controlling what the banks can and can’t do which is effectively communism by stealth. The only job we require the RBNZ to do is facilitate the transactional system NOT control the banks

And indeed just as it’s generally accepted that weaker businesses may go under while stronger survive so to should banks go under. Why should bank shareholders enjoy an almost risk free environment when all other sectors face normal everyday risks

The only job we require the RBNZ to do is facilitate the transactional system NOT control the banks

Wrong and hard disagree. Banks are driven by profits, and the RBNZ's mandate is financial stability. Does NZ look like we are in a state of financial stability after the RBNZ dropped the LVR's in 2020 and created the FLP? What did the banks do when this happened? They lent as much money as humanly possible at wild DTI ratios with nothing but profit in sight as they had carte blanche form the RBNZ. Yes the RBNZ was foolish in this, however it was a prime example of why we have these controls for the banks given their very different motives. Any bank would be able to tell inflation would rear after such levels of liabilities created for mortgages and stimulus form the GOVT, yet they stress tested very low thinking the good times would be forever.

I don't want a bank run either, and have no confidence in them regulating themselves. I'm glad the RBNZ is doing the job, even if I may criticise them sometimes.

Do you remember the GFC? A bank, or banks, failing is much more impactful to society than a steel factory or retail store closing its doors.

Moving regulatory and compliance risk off the books aren't they? FMA and RBNZ have resources to chase a half dozen banks but not hundreds of independent brokerages.

Is there any way that you able to strip out the 1st Home Loans from Westpac's numbers?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.