ANZ New Zealand, NZ's biggest bank, posted a 7% drop in annual profit as loan impairments rose and derivatives used to manage interest rate and foreign exchange risk swung to losses from gains the previous year.

ANZ NZ's September year net profit after tax fell $164 million, or 7%, to $2.135 billion from $2.299 billion in the September 2022 year, the first time it topped $2 billion.

Loan impairment charges jumped $144 million to $183 million. Derivatives, used to manage interest rate and foreign exchange risk, swung to a loss of $127 million from a gain of $235 million.

Operating income rose $468 million, or 10%, to $5.013 billion, with net interest income up $478 million, or 13%, to $4.239 billion. Operating expenses increased $13 million, or 1%, to $1.659 billion.

ANZ NZ CEO Antonia Watson said home lending rose 3% across the September year, with business and agriculture lending down 2%, or $850 million, due to lower commercial property lending and customers "remaining cautious about taking on further debt." Customer deposits rose 2%.

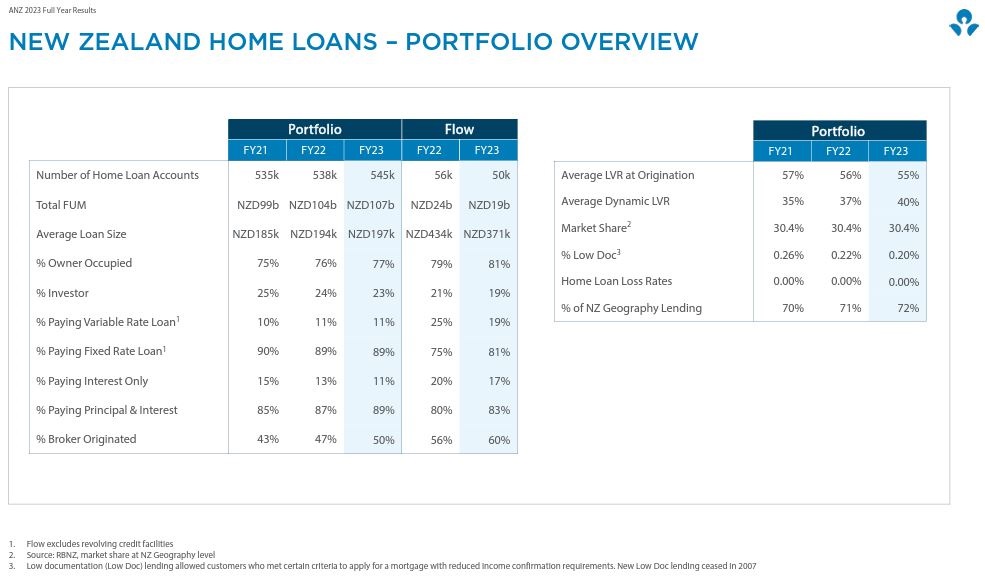

ANZ NZ lent $19.3 billion in new home lending over the year, down from $24 billion in the September 2022 year. Housing lending market share was flat at 30.4%, with ANZ NZ's total lending book rising $3 billion to $107 billion. Housing comprises 72% of ANZ NZ's total lending.

Watson said the bank was prepared for a potentially difficult year ahead.

"New Zealand is probably headed into tougher times. Inflation is expected to remain above the Reserve Bank's target range, interest rates will likely be higher for longer and unemployment is expected to rise," Watson said.

"We've done stress testing across the [mortgage] book and at current interest rates we see it as continuing to be pretty manageable in terms of how many customers end up in arrears. [It's likely to be] in the hundreds more than the thousands. The big question is whether we get another series of interest rate rises."

According to Statistics NZ, the cost of living for the average household increased 7.4% in the 12 months to the September quarter, with interest payments increasing 27.3%.

More stress expected

Watson said ANZ NZ expects to see more stress among businesses and mortgage holders.

"The majority of our home loan customers have moved onto higher interest rates, and most have adapted well. A third of home loan accounts are ahead by six months or more. But around 34% are on rates lower than 5% with around a third of those rolling onto higher rates over the next six months."

With an increasing number of borrowers falling behind on payments by 90 days or more, ANZ NZ has increased the amount of money put aside for potential bad debts by $144 million, increasing total credit impairment provisions to $857 million from $751 million. Of these, $792 million are collectively assessed, and $65 million individually assessed.

ANZ NZ loans at least 90 days past due, but not impaired, rose to $658 million at September 30 from $452 million a year earlier. Residential mortgages comprised $598 million of the total, up from $355 million. Watson said home loans at least 90 day past due were at 60 basis points, or 0.60%, of the bank's total housing book, up from 36 basis points a year earlier. The annual home loan loss rate, however, was unchanged at 0.00%.

The bank's serviceability test rate for home loan applicants is now 9.1%, having been as low as 5.8% in the 2020-2021 period.

Watson described the year as a game of two halves. According to Aussie parent the ANZ Banking Group, its NZ unit's annual net interest margin (NIM), the difference between what the bank borrows money at through the likes of deposits and what it lends it out at, rose 17 basis points to 2.64%. However, the second half-year NIM was down six basis points from the first half-year to 2.60% from 2.67%.

"The slower housing market meant banks were fighting even harder for customers, global inflationary pressures saw wholesale interest rates rise, and many New Zealanders moved their savings from on call accounts to higher interest earning term deposits," Watson said.

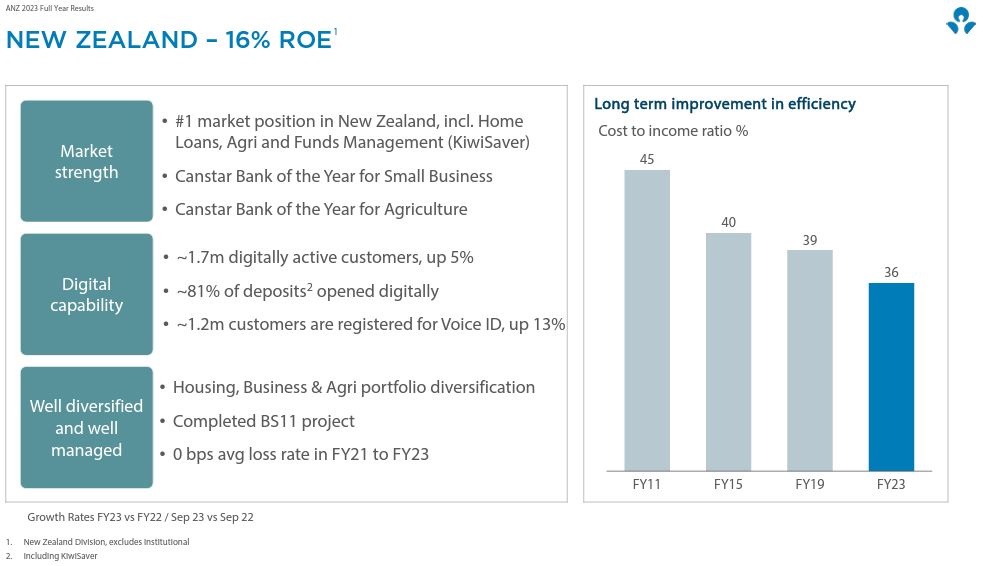

The ANZ Group put ANZ NZ's annual cost-to-income ratio at 36.3%, down 190 basis points. Its second-half cost-to-income ratio rose 180 basis points to 37.2% from the first-half's 35.4%.

ANZ NZ's gross impaired assets rose 24% year-on-year to $131 million, equivalent to 0.10% of gross loans and advances versus 0.08% a year earlier.

'Your average household, is in pretty good shape'

Shayne Elliott, CEO of the ANZ Banking Group, sounded fairly upbeat about NZ, which delivered its parent a 16% return on equity. NZ was "a story of quality and resilience," he said.

"What we're seeing in New Zealand, despite the fact that it's had sort of faster and bigger rate rises [than Australia], and is a little bit more vulnerable as as an economy than Australia, the reality is that the data says that the consumer, small businesses, remain very robust. They used the Covid period to shore up their balance sheet so they saved a lot of money, they cut back on their spending and so, the household, your average household, is in pretty good shape," Elliott said.

"Now, that's not to diminish the fact that there are clearly some who are struggling and there's more struggling today than there was six months ago. But interestingly, there's not more today than there was prior to Covid. So actually, the stress levels are reasonably well managed at this point. So, if New Zealand is a lead indicator for Australia and we think it is, even though there are some differences, that actually bodes pretty well for the resilience of our customer base and the broader community."

The ANZ Banking Group posted an A$21 million fall in net profit after tax to A$7.098 billion. Annual dividends per share rose 20% to A$1.75, its return on equity was up 54 basis points to 10.9%, and its common equity tier one capital ratio rose 105 basis points to 13.3%. Group NIM rose seven basis points to 1.70%.

ANZ NZ's press release is here.

The ANZ Group press release is here, and the investor presentation here.

31 Comments

haw haw .... "jolly good show ol' boy" says I from my luxurious Point Piper mansion, complete with helipad and 270 degree view of good ol' Sydney harbour & town ....no matter what happens with bourses, markets and you lot, the working plebs, our ilk always come out on top ....haw haw

interesting their loans to OO has dropped by 2% since 21 but the loans to investors are up 4% in the same period 66/34% now

and 1st home buyers only make up 8%

will only be country of renters in the next 20 years

Heard a comment on radio I think, suggesting statistics point to 50% of retirees in 2050 will be renting. That's not really that far away

You'll own nothing, and you'll be happy.

You renters, that buy your own places, you'll continue to pay rent to us ... and you'll be happy.

It's becoming like religion, i.e. you'll only enjoy your "purchase" when you're dead.

"If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around them will deprive the people of all property until their children wake up homeless on the continent their Fathers conquered ... I believe that banking institutions are more dangerous to our liberties than standing armies ... The issuing power should be taken from the banks and restored to the people, to whom it properly belongs."

Sounds a little Marxist though...

What is interesting though is that from Jesus Christ and the moneychangers, through Adam Smith, Karl Marx and the like, to the original inventor of Monopoly, have all highlighted the outcome and consequences of following certain ways, yet the rulers have taken it as their playbook.

And what have we, the people done?

Is this of any note? https://www.rnz.co.nz/news/business/495514/blackrock-mistakenly-publish…

Sages, spiritual teachers and indigenous peoples throughout the ages have taught the same thing. The human conditioning, becoming slaves to their possessions. Unable to give unconditionally, always expecting a return.

The tragedy is that many of these teachings have been hijacked and corrupted by those in power. Note the taking of Wu Wei from the teachings of the Tao Te Ching (Taosim), translated into laissez-faire, to become free market economics. The total opposite to the true teaching.

I think the idea behind the modern saying is that some will own everything and everybody else will have to rent everything.

non record profit? what has ANZ been doing wrong?

turns out, the banks also need to manage their interest rates or they go bust.

they had good cash profit, but their assets used to manage interest rates got hit hard. hence total profit down.

Operating income increased. Which could argue is where to look due to the mark to market adjustments.

You can see some of the impact in their numbers in the investor presentation - LVR for those >80% has gone up significantly due to drop in value of homes and those more than 90 days late on NZ home loan payments has doubled to 0.5%. They've also kept expenses flat, and cut 200 staff over the last 18months in NZ.

This is what I find intriguing.

Rates are up, margins are up. Income is up. Expenses are relatively flat. Profit is down.

those more than 90 days late on NZ home loan payments has doubled to 0.5%

I get the feeling this is the Key. The biggest residential lender by volume may be bleeding more than what the figures suggest. WIth values down, they will be bending over backwards to ensure mortgages don't get to this stage, let alone a full default resulting in a sale.

With the impending Christmas Period and the ensuing debt fuelled present buying, I get the feeling the traditional post Christmas debt hangover will be extreme come february.

The Cartel rolls on more stealing $2 billion this time.

I hope the 3 egos have a Serious look at this Aussie banking cartel.

At least we own TSB , Kiwi bank etc we need to support these banks and keep the profits in NZ.

On top of this they control our housings market with there Ponzi as well.

Why have we let this happen NZ?

We don't teach economics and finance as core subjects at high schools.

For those that don't know - when any suggestion along these lines is made, the finance industry lobbyists go into overdrive convincing our politicians that only the three "R"s are required and economics / finance is best, like sex, taught at home.

We had home economics at school - the practical utility functions.

Most people only learn economics from the govt. (who are useless at it), the media (who are only parrots) and the banks.

I studied it as part of my university degree and learned it's a crock of shit. Why do you think it's not taught in schools? Would the students also be guided to critically assess it and be empowered to learn ways and means of not adhering to it?

"we need to support these banks and keep the profits in NZ"

I doubt National and Act see it the same way. I think it would be more likely that they would try and sell Kiwibank

Lol doubt it, our new prime minister was hand-picked by the chair of ANZ board. Which stinks of corruption BTW.

Quick explainer - huge bank profits are a feature of our system, not a bug...

- Bank loans create customer deposits - so the more private debt we have, the more customer deposits are in the bank.

- RBNZ requires banks to have a given amount of equity relative to total customer deposits.

- So, combine 1 and 2 above and it is clear that the more private debt we have in NZ, the more equity banks have to hold (equity = investors cash etc).

- If we have $600bn of customer deposits in banks, and RBNZ require 10% equity, then banks need investors to stump up $60bn of equity.

- If investors expect a 13% return on that $60bn of equity, then bank profits need to be $7.8 billion after tax.

As we have seen in recent years, banks can provide juicy returns like this by simply setting interest rates on loans higher than interest rates on deposits, and adjusting lending rates more quickly to increasing market rates than deposits rates (and vice versa).

combine 1 and 2 above and it is clear that the more private debt we have in NZ, the more equity banks have to hold (equity = investors cash etc).

I like your description of the flow above. As Richard Werner says, banks are not really in the business of lending money. They're in the business of buying promissory notes. Not many people understand that. Even if they work for a bank.

Thanks. Banks will of course *always* create brand new money to buy promissory notes (e.g. a signed mortgage agreement) if they think that the borrower will be good for the repayments.

Obviously, if a bank provides a 12% to 16% return on equity in a safe international currency held in one of the safest banking systems in the world, they will never struggle to find investors willing to commit their equity either!

Banks also need to hold certain levels of liquid assets as described here. https://www.rbnz.govt.nz/-/media/project/sites/rbnz/files/regulation-an…

So can a bank in NZ sustain without deposit? This would mean they don't need much shareholders equity, but may need liquid asset to cover credit risk.

With risk weight of mortgages are lower, they don't need to hold much capital against it. Isn't it ?

Also these mortgage backed securities are considered highly liquid asset . (LSAP purchased these along with govt bonds )

So just wondering why would a bank attract depositors? May be not to make this easy one-sided game sooo obvious?

.... more equity banks have to hold (equity = investors cash etc) ....

Are you sure is this the same 'equity' being used here ? some RBNZ docs calls 'assets - liabilities' as equity as well.

My (probably overly crude) understanding is that bank shareholders (which can be a parent company) have to stake a given amount of equity. RBNZ set minimum requirements for this equity. When NZ banks make a profit, they return this to their 'parent equity holders' who I presume are their parent banks in Aus. Happy to be corrected though.

That is correct. Bank depositors themselves are kind of unsecured creditors to the banks. Most people don't understand this either. But as you allude to, the Antipodean banking system is among the safest on the planet. I'm not going to argue with that.

I don't think 100% of profits go to shareholders. Usually the payout ratio is less than 100% and what doesn't get paid out is retained earnings (which contribute to the ongoing growth of the equity number).

Yes that's my understanding too. Banks can play with this ratio to suit their strategy of course. Ditto what they choose to put aside for bad debts etc.

jfoe,

'If investors expect a 13% return on that $60bn of equity'. But should they? We all know that those banks are too big to be allowed to fail, so surely the ROE should be significantly lower.

I would go much further and change the model to something like the one proposed by Irving Fisher almost 100 years ago in 100%Money. I imagine you know of it. Put simply, his proposal was to require that any deposit that could be withdrawn or used to make a payment on demand be backed by sovereign money-and that banks which offered such deposits be permitted to do no other business. This proposal was adopted by economists at the University of Chicago and became known as 'The Chicago Plan'.

...

ANZ NZ has increased the amount of money put aside for potential bad debts by $144 million

Are these for just plain write off or mortgage sale related expenses ?

Remember sometime back during a realty talks over BBQ, a mate 'revealing' banking secrets of just giving away mortgages if you are stressed

economic hedges used to manage interest rate and foreign exchange

mmmm, trading losses, in years when trades went right these are called profits..... (we then slap each others backs and pay big bonuses....) but the financial media lapped it up...

Let me pull out the world tiniest violin and a microbe to play it. Don't worry it has more ethics than NZ property market investment leaders aka our bank overloads. Just move us to the battletech universe strand, we are already half the way there.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.