HSBC, which announced in June it was quitting New Zealand retail banking, says it's selling its NZ mortgage portfolio to a NZ subsidiary of Australian non-bank lender Pepper Money.

HSBC says the agreement with Pepper Money, which is listed on the Australian Securities Exchange (ASX), is expected to include about $1.4 billion of mortgages. The deal's expected to go through by late November, subject to approval from the Overseas Investment Office. Pepper Money has had a presence in the NZ mortgage market since 2011 when it acquired GE Capital’s Australian and New Zealand home lending business.

"The sale of the mortgage portfolio to Pepper Money will ensure our customers have continued financial solutions and support. The mortgage portfolio sale is part of the wind-down of HSBC’s wealth and personal banking (WPB) business in New Zealand, which was announced in June 2023. The wind-down of the rest of the WPB business will continue in phases with adjustments made to accommodate the sale of the mortgage portfolio," HSBC says.

"HSBC will continue to operate its wholesale banking business, which includes commercial banking and financial institutions & government, along with its markets & securities services business. Each of these businesses is primarily focused on supporting internationally oriented clients that benefit from the HSBC Group’s unique global network and international financial capabilities."

An HSBC spokeswoman says the value of the deal wasn't being disclosed.

For borrowers on a fixed mortgage interest rate, HSBC says this will remain for the duration of the agreed term. Meanwhile, the wind-down of HSBC's deposit business will continue in phases, it says, with some adjustments made to accommodate the sale of the mortgage portfolio.

"We remain committed to supporting you and will do everything possible to ensure a seamless transition," HSBC says.

A big step for Pepper Money

HSBC, best known for its "premier" service, is an interesting combination with Pepper Money, which provides home loan options for people who don’t meet banks' lending criteria.

Pepper Money doesn't take deposits and is funded by money raised through professional, or institutional, investors from the likes warehouse facilities and securitisation programmes including residential mortgage backed securities (RMBS) and auto asset-backed securities (ABS).

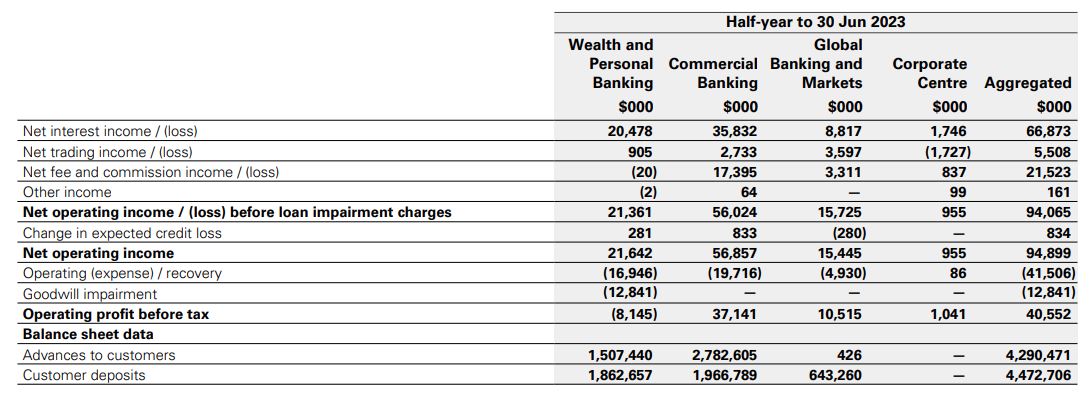

As of June 30, HSBC NZ's wealth and personal banking had home loans of $1.5 billion, and customer deposits of $1.87 billion. HSBC NZ made unaudited half-year profit of $29.2 million. In comparison Pepper Money had NZ assets under management of just A$300 million as of the end of 2022.

Pepper Money says it'll fund the deal in a similar way to how it funds its loan origination activity, and as it has funded other loan book acquisition in the past. That is through a combination of senior and mezzanine funding with Pepper Money contributing the first loss equity.

"The portfolio being acquired is a prime, seasoned and well performing portfolio, and the level of first loss required reflects this," says Pepper Money’s CEO, Mario Rehayem.

"Pepper Money has been servicing mortgages in New Zealand since 2011 when it acquired GE Capital’s Australian and New Zealand home lending business. Since then, Pepper Money has continued to grow its presence in this market with establishment of an end-to-end mortgage platform and nationwide rollout of a full suite of residential home loans (prime, near prime and specialist loans) in 2019."

"Today’s announcement of Pepper Money’s agreement to acquire HSBC’s $1.4 billion mortgage portfolio is a further step in our growth strategy. It is a testament to the ongoing diversification of Pepper Money’s revenue streams. Pepper Money has continually demonstrated our strong capabilities in loan portfolio acquisition and management, over 23+ years, and this acquisition will see the business continue to build scale in New Zealand, a market which we understand well having serviced mortgages and delivered compelling customer service since 2011," Rehayem says.

Quitting with Reserve Bank branch review underway

In June HSBC said it would wind-down its NZ wealth and personal banking business over several years, and was stopping accepting new NZ retail customers with immediate effect. The bank said the decision followed a strategic review and reflected the rapidly evolving commercial, regulatory and technology environment for running a sustainable retail banking business.

HSBC established a branch in NZ in 1987 becoming the first overseas bank branch to be registered here. However, it's not locally incorporated in NZ. The Reserve Bank is reviewing its policy for branches of overseas banks, proposing all branches of overseas banks operating in NZ be restricted to wholesale business with corporates, institutions and other wholesale investors, meaning they couldn't take retail deposits or offer products or services to retail customers.

In a submission to the Reserve Bank last year, HSBC said it supported the current policy saying it; "may need to substantially change strategy in response to such a significant change in the regulatory environment."

Despite this an HSBC NZ spokesman told interest.co.nz in June the decision to exit NZ retail banking wasn't prompted by the Reserve Bank's proposed changes. The group's review explored a variety of options and the ultimate decision wasn't just about NZ with the HSBC Group having been reviewing various businesses around the world, the spokesman said. The review followed pressure from Chinese shareholder Ping An Insurance, which wants HSBC to prioritise growth in Asia.

In its latest disclosure statement HSBC NZ notes the Reserve Bank proposes that branches of overseas banks operating in NZ will be allowed three years from the publication of its final policy settings in the second half of 2023 to be fully compliant.

"The outcome of this consultation could have an impact on the schedule of the exit of the wealth and personal banking business in New Zealand via a wind-down," HSBC NZ says.

"The schedule of the retail wind-down will be reviewed once the Reserve Bank has issued a final decision on this policy."

Separately, HSBC NZ has disclosed an impairment of $12.8 million reducing the value of goodwill related to its wealth and personal banking unit to nil. Winding down the personal banking business has also seen HSBC NZ impair software worth $800,000.

The HSBC-Pepper Money deal does not require Reserve Bank approval.

*The HSBC NZ table below breaks down its operations across its four business units.

28 Comments

This is in your face stuff from HSBC. Why would they not sell it to a regular bank?

Were there offers from a first tier bank?

Unclear. I appreciate they want to offload customers asap but am interested to see how this plays out. Gong from an international bank to a non-bank lender.

I wonder if they will honour the rates people are on, or get them to refix.

I'd imagine they would honour the remaining term. That would be written into the loan contracts which they are buying.

All home loan(s) will transfer across to Pepper Money at the end of the transition period, which we expect to be in late November 2023. If you are on a fixed interest rate, this will remain for the duration of the agreed term.

And if you are on a floating rate? It gives you 8 weeks to transfer to Kiwibank (or your bank of choice) or go with the relatively high rates of PM.

This is in your face stuff from HSBC. Why would they not sell it to a regular bank?

Because quite possibly a 'regular bank' doesn't want the book. Would love to know the profile of their mortgage book. HSBC has a notorious reputation for how they operate and with whom they operate.

Unsure what previous loan rates were, the one fixed rate left for HSBC is 6mth 7.19%

From Pepper Moneys website:

Floating interest rates from 8.54% p.a. to 12.89% p.a.

2-year fixed interest rates from 8.34% p.a. to 12.69% p.a.

3-year fixed interest rates range from 8.04% p.a. to 12.39% p.a.

HSBC rates were always competitive, particularly for premier customer - typically around what TSB or Heartland bank offer

HSBC rates were always competitive, particularly for premier customer

More importantly, if the NZ mortgage market was a nice little earner, why would you sell your book?

HSBC is desperate to keep the Ponzi alive in the UK.

HSBC will launch 40-year mortgage terms for the first time as borrowers scramble to reduce their monthly mortgage payments.

The move is aimed at helping “aspiring homeowners” buy their first properties, the bank said.

It joins a number of other, mainly smaller, lenders who have offered “marathon mortgages” to prospective buyers who may struggle to otherwise afford installments on a more typical 25-year loan.

https://www.telegraph.co.uk/money/consumer-affairs/hsbc-launches-40-yea…

for hsbc it was never really a winner. from what i heard the wealth and personal banking has been a struggle for them in NZ (not profitable), and with their nz presence being a branch (of hong kong, i think) it was only ever going to get more prohibitive/costly with the rbnz changes coming into effect.

i have our home loan with them and it was a painful struggle to get the documentation from them in time before settlement date. literally down to the wire and wpb in nz it seemed more like a novelty

for hsbc it was never really a winner. from what i heard the wealth and personal banking has been a struggle for them in NZ (not profitable), and with their nz presence being a branch (of hong kong, i think)

HSBC is never going to make money out of retail banking in NZ. Their operation is purely for their HNWI customers. Up to you to piece together the puzzle as to whether or not HSBC's business is partly about money laundering.

yes, and no. don't dispute hsbc does favour certain individuals and flow of funds, however they still have their commercial side to support from an intl presence. if you use them from a corporate perspective this has been a trend for them over the last 10 years or so to retreat from the personal market in a lot of countries but having to maintain a corporate suite of products

not going to go into details but dealt enough with them around the world to know where their priorities lie

You're not outlining anything that disrupts what I just wrote.

Casino-esque

Preparing to take the L in advance to avoid going splat in a years time?

This is nuts, why didn’t KB or TSB step up and take it on - god knows they both need the scale.

amateur hour all around, none of these customers want to bank with Pepper

Because no one has the service model to keep these customers. This did the rounds for a long time, that a deal got done means the price finally dropped enough to match the retention rate

To take the mortgage book on even for $1 would require a first tier lender to have $112m capital lying around minimum to meet the regulations. Given banks are trying to increase capital to meet higher requirements, that's a bad deal. New loans that bring in 20%-35% capital, good. New loans that bring in no capital, bad.

Second tier lenders don't have the same regulations, so the starting bid could realistically have been $1.

Edit: not at all suggesting that's actually where offers and negotiations started, just highlighting the buying power of a second tier bank at the moment.

Insightful. Thanks.

I don't understand any of that.

Firstly, they are almost certain to have bought the loans at a discount to par so I don't know what your $1 has to do with it. All Aussie banks outside the big 4 trade at less than book so why would anyone pay over book for a pool of mortgages? The deposits will go as Pepper are not a deposit taker to my knowledge. Pepper will whack these into a securitisation warehouse and eventually fund them via pubic issue. $112m of capital is chicken feed to the big 4, they just don't have the risk appetite for more NZ$ exposure at the moment.

The $1 is just to illustrate a point that even if the first tier banks bought the mortgages for nothing, they still must have capital reserves to back those loans as regulated by RBNZ. Currently (previously) this was 8%, so banks must hold $8 for every $100 lent out. This is moving to 12%. So for them to take on this mortgage portfolio even before paying HSBC for the privilege, they must have $112m of their own capital set aside dedicated to the new mortgages. And soon it will be $168m. I’m not sure of each banks balance sheet currently, but given they are all pushing for more capital against their existing mortgage portfolios, taking on this new portfolio without any capital injection is a big step backwards. Even for a bank with $50b in loans, this would require about a 3% capital injection just to retain the 8% capital regulations. Let alone the increase. And that’s before they give HSBC a single dollar (which was my point above)

For Pepper Pots, they don’t follow the same regulations so do not have to have the capital to back it, hence why they have a competitive advantage to the big bank’s currently if they have the appetite for it (which they obviously do). They can buy the loans for a price and recoup the costs later.

And yes, I believe HSBC are still taking deposits, those have nothing to do with it.

For the big four, chicken feed you’re right, but as illustrated by $50b example above still a backwards step for them

Yeah, my intention is to move to KB anyway. I assume Pepper has modelled that the loan book will shrink significantly as mortgage terms rollover.

I’m in the same boat. Annoyingly it looks like pepper charge $500 to discharge the mortgage vs HSBC $150.

Hmmm - the whole thing is annoying! But yeah, that's a jump.

I hear this is to avoid opening their books to the NZ Govt around their "private banking clients". Query ...the flows of stinky money...

This may have some validity

From the main banks point of view, better to let someone else buy it lock stock and barrel and those wanting to change (given peppers interest rates who wouldn't) then the main banks can pick and choose who they take on at far less expense, and leave pepper with those that may be behind in the loan repayments so Pepper takes the loss

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.