Westpac New Zealand's interim profit fell 33% as its loan impairment charge surged, and last year's one-off gain from the sale of life insurer Westpac Life wasn't repeated.

Westpac NZ's net profit after tax for the six months to March fell $214 million, or 33%, to $426 million from $640 million in the six months to March 2022.

Net operating income fell 2% to $1.372 billion, and operating expenses rose 11% to $624 million. Westpac NZ's loan impairment charges surged to $154 million from a benefit, or write-back, of $10 million in the March half last year. The bank's cost-to-income ratio rose to 45.5% from 44.9%.

In the March half last year Westpac NZ recorded $140 million worth of "notable items," gains not considered reflective of Westpac NZ's ordinary operations, that boosted income. This time around there was nothing.

Excluding the sale of Westpac Life and other notable items, Westpac NZ says net profit was down 15%. Westpac NZ has previously disclosed a one-off $126 million gain following the Westpac Life sale for $400 million to Fidelity Life Assurance Company.

"While operating expenses increased, much of the extra spending has gone on risk, regulatory and technology projects that will set us up strongly to deliver for customers in coming years," Westpac NZ CEO Catherine McGrath says.

The bank's net interest margin rose 14 basis points to 2.10%, which was attributed to rising interest rates improving deposit spreads and returns on capital balances. Although term deposits now account for 46% of customer deposits, up from 38%, that's still down from pre-Covid levels of 50%.

Lack of clarity on impact of extreme weather leads to impairment overlay

McGrath says there's not yet clarity about several key issues for homeowners and businesses severely impacted by Cyclone Gabrielle and flooding in the North Island.

"As soon as the outlook is clearer, we will be able to work with our customers to agree the best way we can support them over the longer term. Due to the current uncertainty, we have made a [$66 million] weather event impairment overlay," says McGrath.

She told interest.co.nz the weather overlay covers homeowners and businesses, particularly in the agriculture sector. McGrath says $52 million is attributable to business lending and $13 million to lending to households.

"Flooding in Auckland weighed particularly on the retail [loan] book due to the impact on the housing portfolio. In the Hawke's Bay businesses and growers were particularly impacted," says McGrath.

In terms of the clarity Westpac NZ's awaiting, McGrath says this includes firstly, clarity around the impact from Cyclone Gabrielle on orchards, especially apple trees, in the Hawke's Bay, which won't become clear until spring. Secondly, what next week's government budget offers in support for victims of recent extreme weather events, and thirdly, the insurance process playing out for affected customers.

"The combination of understanding the impact on those orchards, understanding the government support, understanding the insurance payout, it's at that point customers can start to make decisions about what sort of support they'll be looking for from us in the medium to longer-term," McGrath says.

Worsening outlook

Another factor within the $154 million impairment charge is the deteriorating economic outlook impacting households and businesses, she says.

“Our economists are forecasting a recession this year. The global outlook remains uncertain and funding markets are moving around. In addition, inflation and consumer spending remain high, increasing the risks of a hard landing," McGrath says.

“The rising cost of living has squeezed households and interest rates have risen quickly. While we are not currently seeing significant numbers of customers requiring hardship assistance, demand is slowly increasing, and we expect it to rise further as the outlook worsens.”

McGrath says Westpac NZ has introduced new programmes to identify and contact customers who might need extra support. Westpac staff have begun calling 600 customers per month, identified as being at higher risk of encountering financial stress. She says Westpac NZ is also writing to about 7,000 customers per month who are coming off fixed-rate home loans to let them know they could lock in a new rate 60 days before expiry, to give them certainty about repayments. And about 1,000 of those home loan customers facing the largest increases in repayments, or "thought to need extra guidance," are receiving follow-up phone calls, she says.

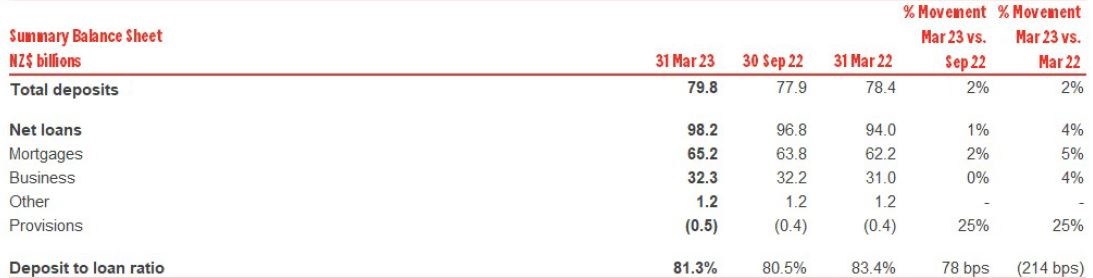

Meanwhile, McGrath says Westpac NZ grew mortgage lending by 5% to $65 billion, business lending by 4% to $32 billion and deposits by 2% to $80 billion.

“We’re in a stable and well-capitalised position and are well-placed to support our customers.”

Westpac NZ's press release is here.

33 Comments

Greater loan impairment charge. Looked up what that actually means (link). https://www.auditnz.parliament.nz/resources/working-with-your-auditor/c…

It can be sumarised as carrying amount (the loan/debt) exceeding the recoverable amount (value). Provisionally this is another Bank preparing for loss making sales/mortgagee sales etc.Makes you wonder what they think is about to unfold...

Indeed.

But increasing the Impairment Provision on a bank balance sheet can also be a way of 'socking profit away for the future'. It's amazing how in different times bank profit announcements of "Westpac New Zealand's interim profit rose 33% as its loan impairment charge fell" seem to get overlook as the share price surges.

Besides, it takes a bit of heat off the bank(s) from those who complain about the high Aussie bank profits.

A lot of people on this board using Impairment Charge and Impairment Provision interchangeably. Any IFRS wizards around to clarify the distinction here? Looking at Westpac's statements, they are two different things reported separately so it'd probably help the conversation to get it right. Looks to me like Impairment Charges are things that have occurred (the bank can point to a particular asset and say it's impaired) and Impairment Provisions are forward looking estimates based on predictions of future conditions and the quality of groups of assets.

That's correct, under IFRS 9 companies have to report their forward looking Expected Credit Losses and this feeds through to reported profits.

As you noted, Impairment Charge and Impairment Provision gets used interchangeably.

So $426 million in profit isn't high? They said they had less revenue, more expenses, and they still make almost half a billion in profit in 6 months, while a number of their customers are struggling.

Is there any other industry in New Zealand that comes even close to those figures?

The canary ain't singing so good no more.

I always think it is slightly disingenuous to pump up loan impairment charges to reduce declared profits. The profits were still extracted from the public at almost the same level as last year, it's just that more of those profits were set aside to cover the potential costs of bad loans.

That said, it is clear that RBNZ is achieving its goal of creating a recession and misery for hundreds of thousands of families. As if collective sadness will reduce the price of the imports (and exports) that determine the vast majority of our prices.

They also created misery for hundreds of thousands of families as they reduced interest rates, allowing house prices to become 10x wages, locking younger generations out of home ownership while property investors/speculators reaped the rewards.

So excessive movements in interest rates in both directions can be very harmful.

Yes, rapid changes in rates (up or down) are always and everywhere really stupid. In fact, monetary policy as a whole should be taken outside and put out of its misery.

Yes dropping mortgage rates to offset consumer item deflation is a silly idea (basically the last 30 years of high globalisation) as all it does is pump massive housing bubbles and creates extraordinary systemic risk.

It creates a system that requires ever endless amounts of cheaper debt to sustain it. And if that doesn't happen - it all comes crashing down (which might be happening right now).

That's the other thing that would make sense. Suppress profit to avoid tax.

Provisions reduce tax now but that profit roles onto books in later years if provisions are not used.... smoothing yes but also prudent here.

This has a "Jesus Christ, Iceberg dead ahead" feel about it....

The only two cards holding up the house are flimsy unemployment and boomer spending.

Westpac are a useless bank. If your profit is rogered when you hold the Government purse then what does that say mr Orr and Mrs Robertson

Government departments and agencies don't trust Kiwibank with taxpayer money. ACC that owns a quarter of its equity also banks with Westpac.

That's the quality of political leadership in NZ - they're either blatantly stupid to retain millions of dollars in NZ by forgoing this low-hanging fruit or have vested interest in protecting bank profits.

I don't understand why the government doesn't put at least some of its business through kiwibank. Supporting local business, as it were.

Maybe there's a conflict of interest I'm not aware of?

One can only conclude that they are either contractually tied to WBC or KB are unable to meet the NZG's performance/SLA requirements.

I mean, what sort of a message does that send?

Systems and services weren't there.

Probably one of the reasons KiwiBank had to try to implement SAP, but SAP failed...

WPAC do not have a life insurance business to sell every year.... plus increased provisions. Still a great biz. Troubles ahead for sure , thats what provisions are for. Its putting money aside now to fix the plane after the expected hard landing.

154mil provisions, assume 50% retail home lending 77 mil, assume about 150k per custie - thats 513 custies losing home at 150k loss each....multiply this across all banks and prob see 2500 mortgage sales where prices come in 30-40% below their purchase.

business lending losses must be building as company liquidations increasing

In the fullness of time (post the distressed selling phase) will we see billions in losses reported? - probably. This is the ugly reveal of the receding tide. Bargains coming - cash is king.

These 2500 will set the price for others, locking people into homes they cannot afford.... more problems 6 months later, this could reach into 2025/2026 easy. Read up on the London market as it moved into negitive equity after 1987, it was not subprime driven and rates where cut. I think it could run 2 years full profit for each bank if its ugly, thats 2bil at ANZ alone, so yeah could run billions One would expect RBNZ to cut to try and reduce the hardness of the crash once the plane flames on impact...

For a growing number, the housing ATM is now "OUT OF SERVICE"

They way things are going, house prices could be down 25-30% (or more) across the country before unemployment rises to a level that is concerning enough for central banks to cut interest rates.

And it may take years for these lower rates to flow through to mortgage holders who are on fixed rates (e.g. 2-3 year fixed terms). So they will be paying high rates, in a recession, with rising unemployment. Not a good place to be.

Apparently RBNZ have stressed tested the banks to cope with a 47% fall is house prices (from Nov-21 levels). This is not adjusted for inflation either. https://www.rbnz.govt.nz/-/media/affb8d6c421e487f842ee54de3359907.ashx

But - this will NEVER happen - right?

The RBNZ say in that stress test link ...

It is our first stress test since 2014 involving high interest rates. Banks noted the difficulty in modelling the impact of higher interest rates, given the lack of historical data. This highlighted some limitations for the stress test modelling of new economic risk factors. A number of banks indicated they are investing in their modelling capability and that this stress test proved a useful exercise.

Could this be interpreted as saying some of the banks were guessing?

The scenario the RBNZ used ...

In the scenario, which begins on 1 April 2022, the New Zealand economy experiences:

o Falling house prices of 42 percent (47 percent from the peak in November 2021);

o Equity prices falling bn/ 3-8 percent (42 percent since December 2021);

o The unemployment rate rising to 9.3 percent;

o Gross Domestic Product contracting by 5 percent;

o The OCR peaking at 5.5 percent and the 2 year mortgage rate at 8.4 percent; and

o In addition to the economic scenario, banks are impacted by and required to model a 1- in-25 year cyber risk event.

To be honest, that's such an extreme scenario that I simply don't believe any NZ banks would be able to answer it sensibly. Kind of reinforces my view the banks were guessing in their responses.

Much less extreme scenarios have brought financial systems to their knees. I'm reminded of savings & loans crisis (80s/90s) and that event that happened just 14 years back. Hmmm ... (Think happy thoughts! Think happy thoughts.)

One would expect RBNZ to cut to try and reduce the hardness of the crash once the plane flames on impact...

So before the election perhaps? (Cutting it fine!)

Before Christmas? (Maybe)

By March '24? (Likely)

Well I can dream. Another dream is we sack the RBNZ's MCP and come up with some sensible banking regulations for NZ residential property that ensures affordability (I like the affordability definition that a renter should be able to afford they house they living based on the rent they currently pay).

Customers are mainly managing now, get into trouble H2 and those who cannot resolve problems likely to be sold out H1/2 2024, this has ages to play out, Banks have to do all they can to help customers in hardship. IMHO peak mortgagee sales will be H2 2024.

(I like the affordability definition that a renter should be able to afford they house they living based on the rent they currently pay)

It's a fair definition. And the best way to ensure that is .. surprise surprise .. DTIs, followed by higher interest rates. Seems we're going to do it backwards here though...

True. End of the day as long as they unwind the exploitive nature of stacking debt and inflating prices, while pulling the ladder up of home ownership with a side of tax avoidance I will be happy. The only really winner here is bank profit, which as everyone can see is huge. Nothing productive is created.

This might be why some branches were *allegedly* rejecting 95% of mortgage applications.

better headline -- Westpac only gouges kiwis for $426 million in the last 6 months!

Yep typical company in New Zealand it expects to make more and more money every year. Budgets only ever go up no matter how well you did the year before. When you have a bumper year, instead of adding a percentage to what the budget was they add it to what you actually did for the following year to try and kill that commission payment.

Ah... an ANZ employee....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.