BNZ's annual profit rose 7% to a fresh record high as income, lending and net interest margins all grew.

BNZ's net profit after tax for the September year rose $92 million, or 7%, to $1.414 billion from $1.322 billion the previous year.

Total operating income rose 10% to $3.131 billion with net interest income up 15% to $2.504 billion. Operating expenses rose just 2% to 1.076 billion. The bank booked credit impairments of $89 million versus a write-back of $37 million the previous year.

BNZ says its net interest margin rose 13 basis points year-on-year to 2.15%, while its cost to income ratio fell 271 basis points to 34.4%.

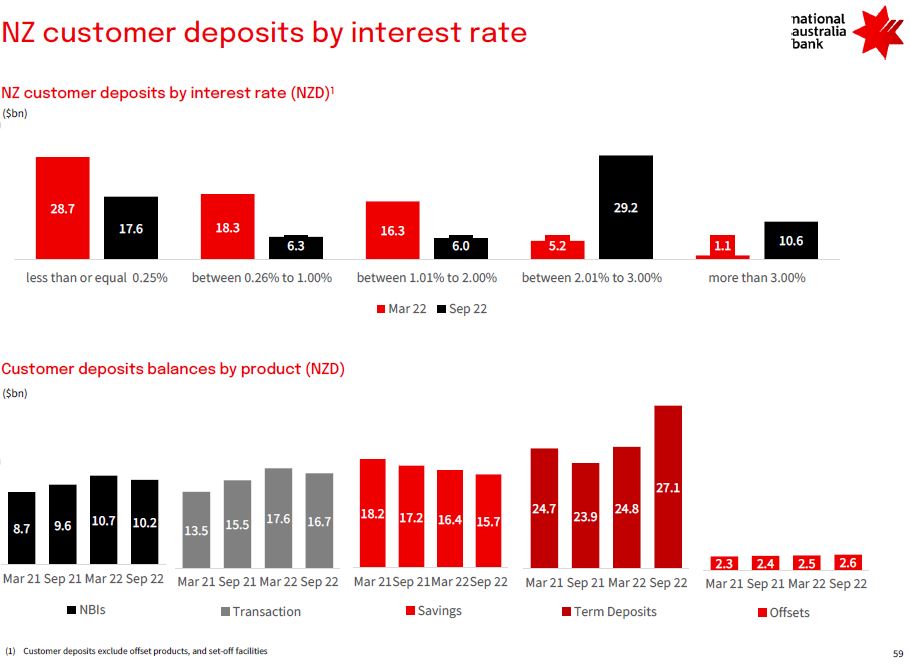

Figures in parent National Australia Bank's results release put housing lending from its NZ unit up 4% year-on-year to $54.8 billion, with business lending increasing 6% to $44 billion. Overall gross lending increased 5% to $99.7 billion and customer deposits rose 5% to $72.3 billion.

"While New Zealand's economy has shown resilience, and the majority of our customers are in good shape, with interest rate increases and the rising cost of living more New Zealanders are going to find it tough," BNZ's CEO Dan Huggins says.

Big four banks' combined profit tops $6.2 billion

BNZ's annual results complete a quadruple of record annual profits for NZ's major banks. Earlier this week Westpac NZ posted record annual profit of $1.047 billion. Last month ANZ NZ posted record annual profit of $2.299 billion. And in August ASB posted record annual profit of $1.471 billion.

That means the big four banks combined posted annual net profit after tax of $6.231 billion. That's up $738 million, or 13%, year-on-year from $5.493 billion in 2021.

BNZ's parent National Australia Bank (NAB), meanwhile, posted an 8% increase in annual cash earnings to A$7.104 billion. It's paying A$1.51 in annual dividends, up A24 cents year-on-year, and equivalent to 68% of cash earnings. NAB's net interest margin fell six basis points to 1.65%, and its return on equity rose 100 basis points to 11.7%. The group's common equity tier one capital ratio dropped to 11.51% from 13% a year earlier.

Over the year to September 30, NAB says BNZ's housing lending market share declined to 16.3% from 16.5%, its rural lending share rose to 21.4% from 20.7%, its business lending share dipped to 22.4% from 22.5%, and its retail deposit market share fell slightly to 17.8% from 17.9%.

NAB's management discussion and analysis release is here.

39 Comments

with interest rate increases and the rising cost of living more New Zealanders are going to find it tough

It's almost like banks benefit the more society suffers.

They've been beneficiaries of taxpayer handouts via the FLP. Good times. Hope they remembered to bring their social license, lest they face backlash from the taxpayers who've been supporting them.

If they go broke and the government steps in, does to government then own the banks, the depositors? Just how do banks unwind?

My only hope is that all the banks do not start pleading poverty and in need of a taxpayer funded bailout in the next couple of years after all these massive profits. No way you can have a banking collapse on the back of these numbers.

No way you can have a banking collapse on the back of these numbers

Oh yes you can. Easy. Pay out all the profits as dividends to the Shareholders and bonuses to the execs. Then when the loss occurs in a future financial period, limit the liability to the value of the shareholding (which by that point will have tanked) and claim insolvency.

The entire management teams will have to relocate to Australia, as they'll be pariahs in New Zealand.

Remember the days when Rod Petricevic was being roughed up in a St Heliers cafe after driving his Porsche up and down Remuera Rd past folk he'd left bare of their savings. https://www.stuff.co.nz/sunday-star-times/latest-edition/3106501/Angry-…

"No way you can have a banking collapse on the back of these numbers"

Remember the BNZ in the early 90s? It comes so quickly. I was working for Westpac in the 80s/90s when all this went down. The bad debts were best described as an avalanche, it was so overwhelming for not only the staff but the banking system itself.

You would hope we have a few folk in government with the morals to stand up for the taxpayer if banks ask to be rescued, and rather than flogging the bank off for a few mates' to get rich the taxpayer gets equity and control of the banks in exchange.

Quota assigned leadership, not merit assigned. So not sure on those morals things. Also hoping. But woke poisons everything

I remember the early 90s. Was in early teens at the time. Dad was made redundant from Glenbrook steel mill with many many others. No work for him anywhere. Used redundancy to invest in a franchise business with about 20 other guys from the mill. Guy running the franchise did a runner overseas. Interest rates hit late 20s. We lost our house. Dad refused to go on the benefit (stubborn British pride). I recall a period of 4 or 5 years where he earned less than the dole (family with 5 boys, I know what hunger is like, immigrant families can be very isolated with no extended family/contacts etc).

This covid spending binge is going to cause a lot of pain. It's only starting.

They will... it's implicit in the license to operate.

Wonderful business to be in - all upside!

Biggest gang in NZ

Branch closure and cashless all happening at the same time. Try do a deposit over the counter and see what happens.

Doesn’t worry me as I hardly use cash anyway but goes to show things are changing fast in the back ground.

Sill can't make a weekend interbank transfer. No customer service either, 9-3 lifestyle

Somehow all three banks have bucked the trend on inflation with small increases in operating expenses (2-3%) in the previous financial year. The same has been observed in the financial releases from Woolies, Meridian Energy and Foodstuffs.

While SMEs crash and burn under high inflation, oligopolies have the market power to pass on the full COGS increase to customers and also cut back on operating expenses.

Rigid cost controls

Not much of a pay rise last year

Will be pay rises this year but not impacting past

Lack of spending on systems?

Moving back-office functions offshore (Bangalore, India), shutting branches, utilising parent company IT assets, etc. In short, putting less back into the NZ economy as they suck more resources out of it.

yeap, thats exactly why that type pf thing needs to be regulated for banking in this country.

There is no excuse why ASB have been able to close all branches in Palmerston North area (population around 100k, plus Feilding with almost 20k) apart from one minimally staff branch in the mall where you wait for hours to get service and weeks to see a banking advisor.

Historically yes, but BS11 making them bring back much and have parent failure plans in case of Seperation, Outsorcing to parent has Definitiely lowered costs. Most will continue to operate most of treasury from Aussie datacenter, not many capital markets end of day operators left in NZ now.

Deposit protection is in the pipeline, not sure go live date but RBNZ putting the team together to take deposits and manage them at the moment.

Banks follow regulators direction, just remember if it turns out that 65:1 leverage on the mortgage books is wrong, its because the RBNZ said thats acceptable. RBNZ have to step in if anything goes wrong as we need our eftpos account for buying groceries the next day. Credit markets will close to all NZ banks if one fails.

I think the model will be OCR / BS11, a haircut on deposit assets (until dep protection kicks in). like RBS etc RBNZ would take large shareholding and equity holders would be effectively wiped out in a failure....

It would have to be much worse then 1987-90 IMHO, but history does have a way of surprising you.

It's a heck of a lot of export earnings canceled out isn't it.

What confuses me is the outcry at $billions floating offshore yet as a country we're still mad keen to bank with them. The government has limited ability to regulate this problem away and they shouldn't have to - these banks aren't the only show in town so vote with your feet and more profits & jobs stay in NZ. Every dollar counts and as a bonus you're helping grow the scale of locally-owned banks too.

Today morning on brealfast show, National leader was grilled and had no response for WHY IS HE NOT HAPPY IF BANKS ARE IN PROFIT AS PRIVATE BIG ENTITY and he had no answer.

Government and RBNZ should be blamed specially FLP, what stopped Mr Orr from stopping FLP. Jacinda Arden raising concern that banks are profitable should also raise a question for if banks are in losses, financial system may fall specially with no deposit protection insurance in NZ.

When PM and her ministers are raising question on bank profitability are actually highlighting their ineffency and frustration.

May be it was a dumb question... the question should be at who's expense is the profits being made and how did this happen!

Maybe he was thinking about in 5 years time when he gets the shoulder tap from the banking overlords, that a certain soundbite of him being critical of bank profits might look poorly.

show some love, throw a TD out at 6%..thks

I guess its hard to lose money when your overheads have dropped due to cutting staff and closing branches and reducing the remaining branch hours to a third of what they were pre-covid.

Today the 2 year bond rate stands at 4.65%. We borrow money on the international markets at 4.65%. Paid for by the NZ taxpayer. The RBNZ lends money to Australian banks at 3.5% via the FLP. Yes we are paying them 1.65% to borrow money from us.

Today they then lend that money to NZ tax payers on a 2 year fixed mortgage at 6.09%. They make 2.59% for lending us our own money.

Corruption in plain sight. The RBNZ is not operating in the interests of the NZ taxpayer, it is operating in the interests of foreign banks. For this situation that should be rewarded with being tarred and feathered and banished to a gulag., We give our governor a 5 year extension at nearly a million a year. I say tear down the existing structures if this is the corruption it spawns.

Valid points but we live in a democracy. Long love the democracy where parties need donations (money) to win elections.

The one who pays expects something in return even if it's a donation. Easy to figure what kind of policies and laws will be pushed through the system.

Again a valid point and why precisely the RBNZ is supposed to be independent. They are not elected. If the money in the economy gets to decide the policy, I would question whether democracy has any value at all.. It creates an environment where policy continues to ring fence wealth for the few. That is an unsustainable situation and will collapse eventually when society only works for a handful of people.

The NZ System for commercial property lending and business lending only amplifies the wealth for the few.

It would be interesting to see the stats on:

Average profit per NZ Company operating in NZ.

Verses

Average profit per Australian Company operating in NZ.

Question. We are reading a lot about corporates making record profits this year, being up X% on last year's earnings etc.

I don't have capacity to fully make sense of these reports.

Do these record profits account for the inflation (covid spending printing binge). If their profits are up say X% on last year (arbitrary number). And inflation is more than that. Then haven't they actually lost money in real terms?

If that is the case, then all these Mainstream media articles aren't accurate to say the least..

Nope. Because profit is profit. If you're meeting increasing costs and still posting profits, then you still have margin.

Sorry prpbably being dumb dumb asking.. what I mean is

Scenario:

Say companyX last year made $100 profit. This year they made $110 profit.

$10 more than last year. A 10% increase in profit.

But inflation was 20%.

Shareholder gets $110 dollars to spend.

But that $110 is worth less in buying power than the previous years $100 profit.

so profits look like more because there is literally more money floating around. But the value of that profit in real terms is less.

The banks have certainly made some tidy profits but how would they go if a bank run hit them? They paint a picture that inaccurately reflects their true position in the market place. The more they support the hiking of rates...the more they expose themselves and their clients to risk.

I have never managed to get property. The one time I'm grateful for that (no mortgage to worry over). But I do have kiwisaver.. When do you all think they will come for our Kiwisaver savings?

This all has an Ayn Rand Atlas Shrugged feel to it (not the movie lol)..

Not a good year....lol Moneys sinking into a big hole everywhere...Billions of dollars ACC, NZ Super ,Kiwisaver. Wont post a link but its not a good year....info is 'common knowledge'...think of it as the 1 in 7 that might turn into somewhat longer than many forecast...."My dog Sam eats purple flowers" ('Draggin' the line'...Tommy James)

reposting this in the hope some expert advises ha..

Sorry probably being dumb dumb asking this.. But have a question regarding corporate and bank profits being announced on media. The articles never seem to speak about real term value vs last year. Does it matter?

Scenario:

Say companyX last year made $100 profit. This year they made $110 profit.

$10 more than last year. A 10% increase in profit.

But inflation was 20%.

Shareholder gets $110 dollars to spend.

But that $110 is worth less in buying power than the previous years $100 profit.

So wouldn't the real profit be less than what it looks like on paper? Seems like a unidimensional perspective when they don't consider the decreased value of money in these news articles.

Seems frequently designed to sell a marxist perspective on reality perhaps (not saying we don't have problem with current state corporations, my beef is with offshore. Fix that and we remove a lot of hidden wealth

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.