Reserve Bank (RBNZ) Deputy Governor and Financial Stability Manager Geoff Bascand has clarified the regulator wants to get itself in a position where it can apply debt serviceably restrictions to banks’ mortgage lending, but this doesn’t necessarily mean it will apply these restrictions straight away.

Bascand told interest.co.nz the RBNZ will at the end of this month start consulting on whether these tools should be part of the RBNZ’s macroprudential toolkit.

“But we still have to go through a process of deciding whether they would be worth introducing and whether the benefits would outweigh the costs,” Bascand said.

The RBNZ has repeatedly said implementing a debt-to-income (DTI) limit could take “at least six months” following the design and calibration of the tool. Meanwhile setting floors on the test interest rates banks use in their debt serviceability assessments could be implemented sooner.

“We’re keen to have these part of our toolkit and we’d like to be able to apply them,” Bascand said.

“But we’ve still always got to make that decision; are they needed? Are they not needed?”

The RBNZ in December 2020 asked Finance Minister Grant Robertson for permission to use debt serviceability tools. In August 2021 he said yes, on the condition the RBNZ avoids negatively impacting first-home buyers “as much as possible.”

LVRs could be loosened if DTIs are brought in

Asked whether the RBNZ would loosen loan-to-value ratio (LVR) restrictions if it introduced debt serviceability restrictions, Bascand recognised LVRs are set at “quite a tight level”.

“So, one could think potentially about some slight change in mix,” he said.

“The settings will depend very much on how high the risks are at the time.”

LVRs help prevent borrowers from falling into negative equity, while DTIs help build borrowers’ buffers against serviceability shocks, like interest rate rises.

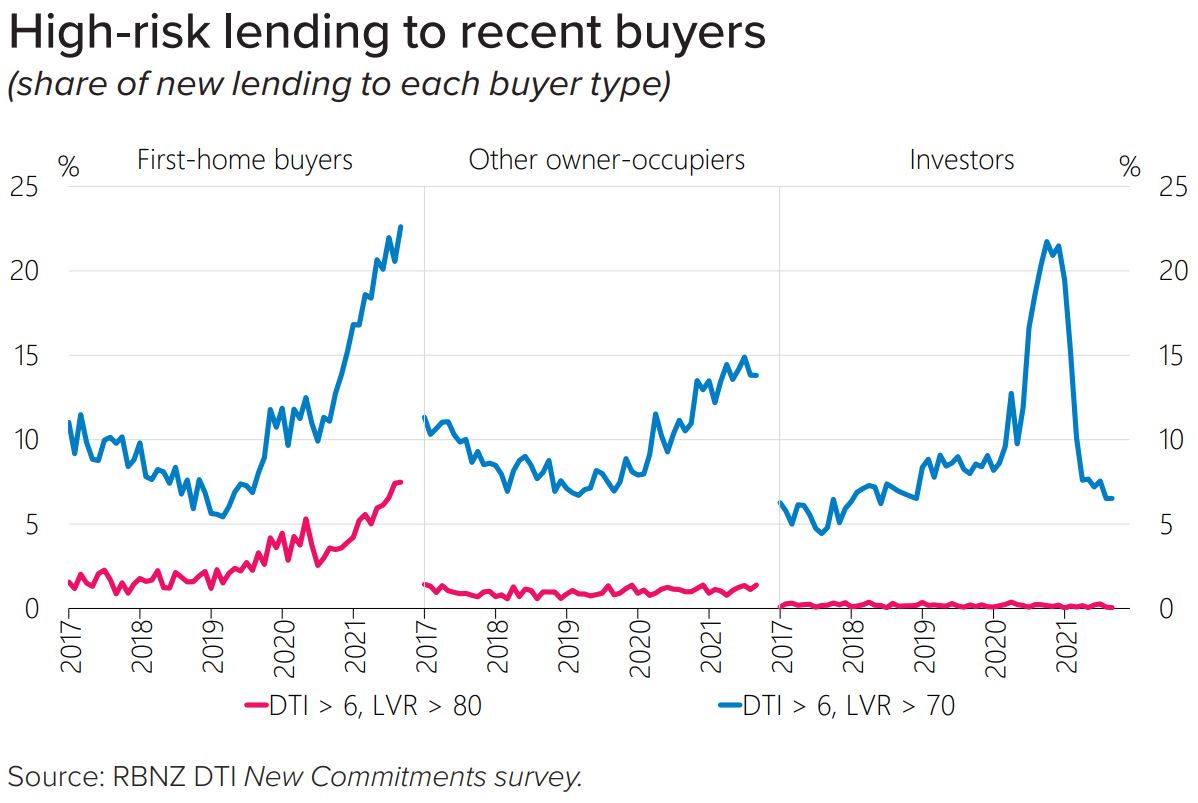

Bascand worried about the cumulative effect of high-risk lending to FHBs

Bascand defended the RBNZ’s decision to effectively target first-home buyers with its recent tightening of LVR restrictions.

As of November 1, only 10% of banks’ new lending to owner-occupiers can go to borrowers with deposits of less than 20%. Previously this allowance, which banks largely use to accommodate for first-home buyers, sat at 20%.

Jim Reardon, CDS Consulting managing director and former Westpac treasurer, is among those who have criticised the RBNZ for its approach.

He made the point banks’ high-LVR lending allowances will be below 10% in practice, as banks tend to give themselves buffers to avoid breaching their limits.

“An operating limit of 5% would effectively leave most first-home buyers out of the housing market," Reardon warned.

“Restrictions on first-home buyers would have long term social impacts as a generation of potential homeowners are destined to become lifetime renters.”

While a 20% fall in house prices would see 22% of mortgage lending to first-home buyers in the year to July in negative equity, it would only see 5% ($5 billion) of all mortgage lending done in that year in negative equity.

That $5 billion is equivalent to only 1.6% of banks’ mortgage books.

Bascand said the RBNZ was worried about the cumulative effect of banks doing a lot of high-risk lending.

“I’m not trying to paint a panic picture that our system is immediately under enormous stress, but you could see the risks rising, especially when house prices have such a high risk of a fall,” he said.

Asked why the RBNZ was targeting a specific type of borrower, while making the case the financial system as a whole is stable, Bascand said, “The financial system’s resilience is partly built on the measures we have taken…

“Banks don’t take all that sufficient care by themselves unless we restrict them.”

Capital requirements not impeding business lending

Interest.co.nz also asked Bascand whether the amount of capital the RBNZ requires banks to hold for the different types of loans they issue (housing, business, agricultural, etc) is supporting financial stability in the long run.

Banks’ loan books are increasingly heavily weighted towards property. For example, housing lending reached 70% of ANZ NZ's total lending this year - up from 67% in 2020, and 63% in 2019.

Bascand said the RBNZ’s framework takes a “sensible” risk-based approach.

“Business lending is more risky. That’s why we ask them to hold more capital for that,” Bascand said.

“There are some risks in the housing sector, and the total amount of capital we’ve asked them to hold is to make sure they’re covered for that.”

Bascand didn’t believe requiring banks to hold a bit more capital for housing loans and a bit less capital for business loans would prompt them to reweight their loan books more in favour of business lending.

He noted banks aren’t capital constrained. Rather, businesses are hesitant to borrow in the current uncertain environment.

He said the RBNZ has “quite conservative” capital requirements for mortgage lending by international standards.

Bascand maintained the competitiveness of the banking sector has a greater bearing on businesses' access to funding than bank capital risk weightings.

First part of video interview focuses on mortgage lending; second part covers business lending.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

65 Comments

After Orr's years of pleading for DTI he seems reluctant and unprepared to implement it. The crazy levels of lending at historically low rates puts the system at risk...then fix it because last time i looked that is the job. Yes some will have to take nasty medicine, but they did it to themselves while overdosing on debt based greed pills. Just announce it and let the market sort it out. Some people love markets dynamics on the way up, and some love them on the way down. You cant keep everyone happy all of the time.

These guys are at fuckn check mate - They cannot actually raise interest rates without it all falling down - something they will be painfully aware of.

No really, mortgage interest rates can top out at 6% and different measures are needed beyond that like the DTI on FHB because looking at the graphs above, its only going to affect FHB anyway. Rising rates is now pricing FHB out of the market anyway. RBNZ have already made the huge mistake of emergency low rates and now they are left hoping they can slowly crawl out of the hole without anybody noticing.

Interest rates at 6% will collapse discretionary spend in a country where the economic powerhouse has been locked down for months - probably long before then.

Don't forget this entire shitshow of a country is set up under the proviso that people spend more than they earn just to cover the basics.

Once that goes away, a lot of jobs and businesses that are already on the fence go with it.

Certainly will affect discretionary spending significantly.

It will also nuke the FHB market, which in turn will have a big impact on the residential construction sector, which has become heavily reliant on the FHB market over the past 3-4 years. That will take a while to hit building (building may not be whacked till 2023), as so many projects are already in train, but it will start hitting consultants heavily exposed to that sector in 2022.

2022 will be interesting indeed.

The projects underway that have question marks over their supplies will struggle and anyone without anything locked in just isn't happening anyway.

We're facing the very real prospect that a huge chunk of consented supply for the next 12 months may just suddenly not happen.

So higher interest rates, less FHB action, but severely constrained on the supply side...

Sounds like a recipe for stagflation to me.

Stagflation, indeed.

The FHB market has already been nuked by 30% house price increases and the increases still have not stopped yet. Interest rates are still going up almost weekly. If your not already in then your out for years.

"Geoff Bascand: LVRs could be loosened if mortgage debt serviceability restrictions are introduced; a change in bank capital risk weightings won't encourage more business lending"

No intent in controlling ever growing house price and have been correct when one say that people in RBNZ has no intent and was obvious with their delaying tactics in implementing DTI and now if forced to implement will loosen LVR - Whatever reason they me give but reality is that it is to offset DTI so even though DTI is enforced will not have the desired effect.

Secondly why are they saying that it will take atleast six month to implemet DTI and at the same time mentions that they have not yet decided if to go ahead or no with DTI. So if not yet decided why are they talking about six month.

Important, it is clear that they are playing with time to deflect from DTI as when will six month start from the time given permission or will take six month to year to decide and than another six month....

Six month.....DTI.....what a farce and this people have audicity to talk about helping FHB where actually all they have is to support and promote ponzi.

who'd a thunk it?

Derek on DTIs

Orr " We're consulting and if your consulting properly you consult with an open mind"

Derek " Housing sustainability , there were suggestions to what was the appropriate level of house prices might be...is there a figure , and is there a suggestion like groups like Demografia that 3 times household income is the optimum level of house prices"

Orr " On your three to one ratio, NO, no sympathy , not sure what it relates to " ..in the past we have provided a ratio of ( Bascand ) 6-7 times .

Whatever and if implemented, DTIs will only be a watered down and carefully constructed tool for the tool box

I think the crew at RBNZ need a full scale rewamp. I know commenters will pounce on me in RBNZs defence. They are as incompetent with their policies as this government has been with its election promises.

When they asked for the DTI tool, one would have thought they would have known what to do with it when given the tool. They asked in Dec 2020 and in Dec 2021, they still don’t know what to do with it.

Tools like DTIs and LVRs are meant to be preventative measures, not remedial ones. The RBNZ can sit around consulting on these things for months if they want, but the point is moot. It's far too late for either of those things to be effective.

Exactly, they stop new people from getting near the cliff. They don't stop the ones that have already gone over and are in freefall, and they definitely don't fix up the ones that went splat at the bottom.

https://businessdesk.co.nz/article/finance/john-key-says-house-prices-w…

For once agree with John Key that house price will not fall as RBNZ will do everything to keep up the ponzi. This is validation of RBNZ role in housing ponzi, whichwe already knew.

At that point it just makes it really damn obvious that housing is not a market but a welfare scheme for the wealthy.

Young Kiwis should be getting very angry at this blatant intergenerational wealth theft.

To be safe cut the OCR while you're at it & crank up QE again...

Banks have other ideas.

Yes let's all become billionaires on Paper. Let's pay a bag full of cash for a loaf of bread.

When it's printing more is the solution?

This is a theoretical conversation, DTI's are in play today. We are currently trying to re-finance one of our mortgages, we are facing a brick wall in terms of the hoops we need to jump through. DTI mechanics are being used today as our cashflows from rent etc are being discounted almost to nothing.

We are in a very fortunate position and will still be able to make it through these hurdles due to our primary income but I have been shocked by the level of resistance from the banks, having been in this game for 20+years it has never been as restrictive.

Can you provide any more detail? Why and how are they discounting your cash flows?

Hi Brock,

In the past our rental income has been discounted in the region of 20-30% to allow for periods of no-tennancy and costs for property maintenance and management. This is an understandable and proper level of conservatism to protect the bank from over-valuing those income streams.

The assessment of those discounted cash flows was then added to our primary income less our own house-hold costs and the resultant was our servicing ability.

At this time as far as we can tell the discounting of our rental income is in the 70-80% range at the moment. A quite radical change and one that the banks are not really able to defend other than "preferring to weigh personal income more highly" aka we are implementing DTI measures.

As I said I think we can still get there but beware if you are about to re-finance, your journey may be bumpy!

Interesting indeed.

Along with FHB demand being nuked, this could nuke a fair bit of investor demand.

Yes it certainly will, what interests me most is what the banks will do. I think they are playing me as they know my detailed financial position but what if I was not able to earn the income I currently do refinancing would be out of reach using these mechanics...what then? Foreclose? Bankrupt me? You may want to dust off your trusts and move some things around, there are some interesting times ahead...

I have had a similar scenario with financing a new property with ANZ a number of years ago. Went to Broker all sorted. Individual banks change policies based on their current book. Never dealt the bank since always a broker as they know what banks are doing what at the time.

I don't know your particular situation, but I suspect many investors with 3+ properties will have to sell some of their portfolio to deal with the coming DTI world.

Sounds like they are planning much higher borrowing costs.

Yes it certainly does but the way they are going about it seems confused to me. Surely if they wanted to protect against that they would simply increase the interest percentage in their calculations (like they have always done)? As has been mentioned above, servicing was always measured against a theoretical repayment level at a higher level of interest (6% or thereabouts) so ensure the average borrower was able to meet their obligations if interest rates increased. It's already part of their model. All they had to do was increase that rate to say 8 or 9% surely?

This seems like an intent to implement DTI without really having the clear line of sight to how it should work. Taking away rental incomes is a nuclear option to me, it will, if implemented in this clumsy manner, brick the investor market. Not in a lowering price of housing stock kind of way, although that may be an upside, but in a bankrupting the mum n dad investor (who still make up 80% of the investor market) kind of way.

Sad for your difficulty in re-financing but heartened that at least individual banks are showing responsibility. How can the RBNZ possibly justify their do-nothing position?

"our cashflows from rent etc are being discounted almost to nothing."

Isn't that the crux of the problem?

20 years ago at most; dare I say it - all, income from an investment property was cash-flow positive. Negative Gearing was a thing of the future.

When Debt is reliant upon Capital Gains to 'service' it, it's a risky business. When a whole country's economy is dependent upon that continuing, you know you have a problem.

DTI's are another way of saying "Restrict the issuance of Debt", and the sooner that happens and the tighter that is, the sooner the economic Sword of Damocles hanging over our heads might be removed.

(And yes. You're right. DTIs are fact of life with lenders this very day)

Interesting observation.

They stay in their ivory tower. See No Ponzi - Hear No Ponzi - Say No Ponzi.

Now, as under pressure are forced to act, coming out to prepare that they may but will dilute and manipulate.

Whatever any experts or people may think and expect but RBNZ has only one agenda and they are ready to do anything and everything to support the ponzi. This interview highlights their rigidness and arrogance in supporting the ponzi.

Geoff......did say, Ponzi

“I’m not trying to paint a panic picture that our system is immediately under enormous stress, but you could see the risks rising, especially when house prices have such a high risk of a fall,”

But the choice of words and how they're expressed is part of the whole problem. The messages are contradictory and mixed. Even in this single sentence, it's a muddle of heightened DGM but the speaker is suggesting that he's not putting forward a panic scenario.

Point taken.

To me, he'd have been better not mentioning 'panic picture', 'enormous 'stress' and' house prices have such a high risk of a fall' in the same sentence!

I have only one question for this guy or these two guys. RBNZ governer and it's deputy. Are you guys really blind or pretending to be blind?

Can they not see what they are doing to our country and it's next generation.

Even the government is letting blind people make RBNZ policies.

It does seem incredible to simply not care.

To housing as to climate, eh. Live it up, pass the cost on.

The govt is also blind, so it's the blind leading the blind at the moment. I think JK might be right. We've reached peak pricing or will do this summer, if it ever gets here. No one's adding any real value. Certainly not the govt who are intent on segregating our small culture & with the banks just clipping the ticket on residential property, where's the value there? There is none. Perhaps we're being set up to be a large retirement village(?) although I would have liked to see some investment in our fragile health system alongside it.

Agreed. No value for anyone but the banks profit margin. Kinda feels like we have all be conned into endless debt.

Not me - I gave up years ago and accepted renting. At least I can still afford popcorn.

Still a bit gutted that I probably won't get to see a negative OCR this time around. That would have topped off the comedy show fer sure.

Which ever way they go it is going to be a cluster F.

The mess will take at least a decade to resolve so for FHBs, buying a house any time in that period may well cost them their equity. Catching falling knives etc. And if this does not happen and at best prices remain at these levels they will never be able to buy one anyway. Either way they are stuffed if they remain.

The best hope for young Kiwis is to leave the country and get their start in life elsewhere where house to price ratios are more sane. Otherwise they risk being financially damaged in a way that they will never be able to recover from.

If I were the government I would precipitate, or allow to occur, a price crash of something like 30 percent or more very quickly, then lay out a path into the future where the whole structure of the house construction market will be reformed and the land development market reformed so that house prices will fall in dollar terms by say 3 to 5% per year and that combined with controlled inflation will move houses to a price to income ratio of 3.5. This value will be enshrined in law and a body something like the Reserve Bank will have sufficient levers and power to maintain that target.

Like it. I would have more than 30% though as that just covers the last twelve months more or less.

Yeah...wow. That is an actual fact and it is actually crazy. So to get back to norms? 60%? Imagine if you had just bought as a FHB!

Haha. DGM gotten what they wanted; unfortunately it had just made it harder for them to buy a house.

Karma in action!

Yep they all got suckered into voting Labour and then they all got lined up against the wall.

Get in quick?

Can never lose with property, right?

Actually, the opposite is true.

The doors are closing on FHBs.

Be much quicker!

Oh, so you are saying you CAN lose with property?

Its going to be the summer of discontent for FHB, the door is about to be slammed in their face I'm afraid. Expect price rises to finally peak in February at the same time the OCR gets another hike and banks top out at 6% rates. There could be much moaning from speculators that the housing market is flat for years after that. The financial wizards on here will actually say house prices are dropping due to inflation.

Still pushing that kiwi house prices can never drop myth?

Time to bring out this link again

https://www.rbnz.govt.nz/statistics/c40-residential-mortgage-lending-by…

A DTI restriction of 6 will only cut out around 25% of FHBs based on the most recent data. That is to say, 75% will be completely unaffected.

Meanwhile, those who own 2 or more properties with even moderate gearing and don't have an enormous salary will be shut out of the market for years. This is likely to help FHBs as the market becomes less crowded - often investors are aiming for similar properties.

Good post.

Imagine coming up through school now and hearing that. "We're closing the door in the face before you can even hit the workforce".

Everyone and me included comment / react but does it matter as can be seen that come what may Mr Orr is in a mission to kill the entire breed and create a social division.

Problem is that their is no discussion - Mr Orr and his partners should be grilled with hard question and counter questions instead of monologue statement from them or polite question and answere allowing them to get away with their agenda.

Seriously are they so ignorant or being ignorant as it suits them.

Look at ole Ponzi shister John trying to get in on the DGM act....

https://www.msn.com/en-nz/news/national/john-key-on-the-next-gfc-ingred…

What a DGM!

The truly sad, sad thing is that John Key knew all of this when he was in charge; when he had a chance to do something about it. Yet he didn't.

That article speaks a lot of sense. But no more so than back in 2007, when he was saying exactly the same sort of thing. But he was 'got at' wasn't he; on that trip to NY and that faux pas on Letterman - "You don't get out of debt by borrowing more money!", he said. Then he was taken aside, and quietly reminded of his position and what would happen if he didn't toe the line....... and here we are. Thanks, John.

NZ will be dictated by what happens in China. Its to big a customer and global financial power, much in the way that Aussie and the US are. They catch cold, and so do we, regardless of what Mr Orr does. If China has a meltdown, so do we.

China has been smart enough to realise what's coming. Ask Jack Ma. Oh, that's right! We can't.

They are relocating wealth from those who thought they had it, back to The State to cushion the storm that's coming.

That's what's coming here as well. Those who think they have wealth to survive any storm will realise that they literally can't eat their investment properties. And if there's no one that can buy them, all that will be left will be the debt.

Those with no debt will also be hit hard, make no mistake about it. But just like China is getting ready today, so have they.

Its easy to write off the debt...

The kicker is it writes off wealth and more importantly Income streams....

And hey presto, no viable consumers

Banks write off debt...hahahaha.

Yes, China has more courageous leadership than us - they have screwed up and are going to try and sort it out with a willingness to allocate pain. We just drift with hope into whatever is next.

The CCP also has a big distraction card to play whenever it needs it (after the Olympics) - they can decide when to hot up the contest over Taiwan. I guess if things get really bad here JA could order one of the frigates to be towed over to Tuvalu for a preemptive strike. Imagine the surprise on their faces.

NO, ANYONE WHO OWNS PROPERTY MUST BE PUNISHED!

Speculators yes. Home owners no. The levels of debt stacked in order to offset income tax had reached such a parasitic level that it couldn't continue. Let's face it, its putting the whole banking system at risk.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.