The Reserve Bank (RBNZ) says the number of people and businesses defaulting on their loans is rising but remains at relatively low levels.

Retail banks told the central bank they expect the proportion of non-performing home loans to rise to 0.7% by the end of the year, half what was seen after the Global Financial Crisis (GFC), and up from 0.5% now.

The RBNZ said in its May Financial Stability Report that the impacts of high interest rates have been contained so far and if anything have been less severe than anticipated.

Most residential mortgage borrowers have repriced onto much higher interest rates, with the average now 85% of its projected peak. While the vast majority are coping with this stress, some are not.

Loan arrears and non-performing loans are around the levels experienced during the Covid crisis and are well below what was seen following the GFC in 2007/08.

RBNZ data shows $1.76 billion of banks' $352.4 billion worth of housing loans outstanding at the end of March was non-performing. That's 0.5% compared to 1.7% of agricultural loans and just over 1% of commercial property loans considered to be non-performing.

The RBNZ data also shows just 300 housing loans were impaired as of March 31.

Banks expect mortgage stress to increase as the economy slows and interest rates remain high. However, how bad it gets depends on economic activity and labour market conditions.

The RBNZ said it was “encouraging” the increase in borrower stress had not accelerated.

Business failures, which have been unusually rare in recent years, have begun to pick up in interest rate sensitive sectors — such as the construction sector.

Commercial property is another sector that has been under pressure, with debt service costs suddenly much higher, and demand for both office and retail space much weaker.

Higher milk prices have helped ease pressure on the dairy sector, although it remains heavily indebted, while the sheep and beef industry is struggling with falling meat prices.

Businesses and households are generally borrowing less money. This means aggregate debt levels as a percentage of the economy are falling, helping to improve resilience.

Stable for now

Average mortgage rates have risen from 2.8% in 2021 to 6% today, and will continue to rise to about 6.5% at the end of this year.

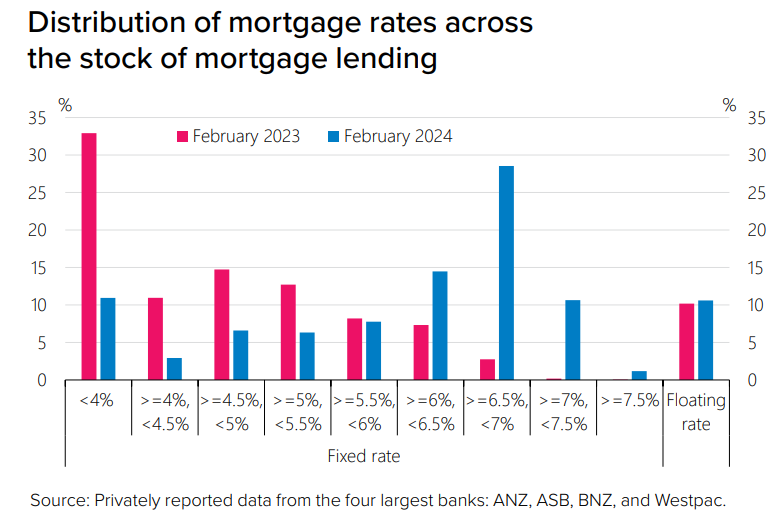

Only about 10% of mortgage lending remains at fixed rates below 4%, likely those who chose the longest fixed rate terms during the pandemic years.

Borrowers appear to have cut discretionary spending and, in some cases, slowed the rate at which they are repaying the principal on their loan.

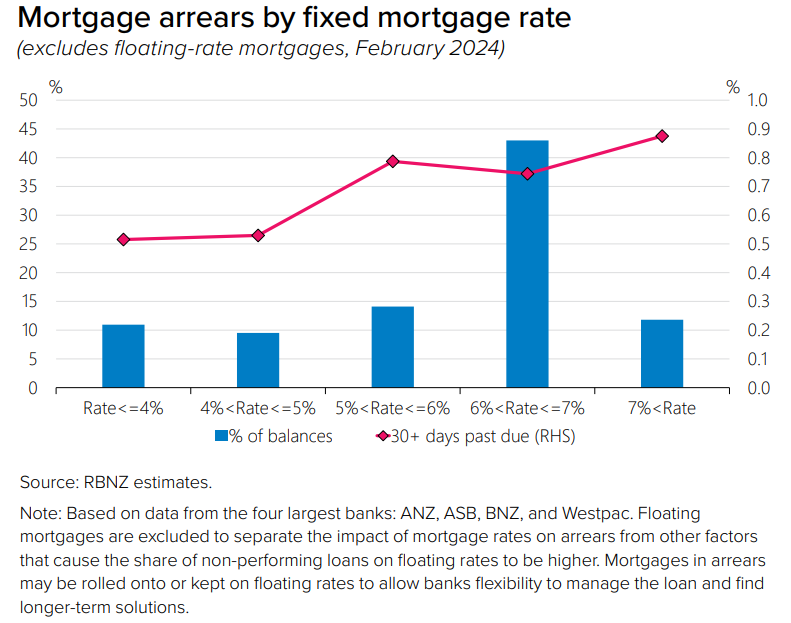

These actions have not been enough for about half a percent of all borrowers, who have fallen 90 days behind on repayments and have been classified as non-performing loans.

The share of lending that is 30 days past due, which is a leading indicator, has climbed to almost 1%. It is now above the 2020 peak and higher than it has been since 2013.

Banks expect the proportion of non-performing loans to peak at about 0.7% at the end of this year before easing. This figure got as high as 1.2% in the years following the GFC.

Job losses are often the cause of non-performing loans and the number of arrears will likely increase as the unemployment rate continues to climb.

This will impact bank profitability but is unlikely to threaten their stability, the RBNZ said.

“Very few households are in a position of negative equity and banks would likely face relatively small losses in the event of an increase in borrowers defaulting”.

While residential mortgages are looking relatively resilient, commercial property loans are on much shakier ground. This sector makes up about 8% of NZ bank lending.

The RBNZ said remote working and online shopping trends had caused an increase in vacancies for office and retail properties. Now, the slowing economy could worsen the problem.

The central bank also said the Government’s plan to remove depreciation tax deductions for commercial property could also add to existing cash flow pressures.

If cash flow stress gets too severe, some property owners might attempt to sell up. However, that may be difficult as the market has become much less liquid.

“A global commercial property slowdown could further exacerbate this as it could weaken foreign investors’ appetite for property in New Zealand. This would further reduce the pool of potential buyers,” the RBNZ said.

*The charts below come from the RBNZ's Financial Stability Report.

23 Comments

Higher milk prices have helped ease pressure on the dairy sector, although it remains heavily indebted, while the sheep and beef industry is struggling with falling meat prices.

Considering the immense pressure that CNY, JPY, KRW are under, I can't really see how that will translate into juicy export receipts from milk powder.

"Considering the immense pressure that CNY, JPY, KRW are under, I can't really see how that will translate into juicy export receipts from milk powder."

re export receipts ... See my comment below as to why this recession could be at least as bad as the GFC. Unlike 2008, no white knights riding to buy white gold this time around.

re export receipts ... See my comment below as to why this recession could be at least as bad as the GFC. Unlike 2008, no white knights riding to buy white gold this time around.

Just witnessed a video clip of in-store Japan showing 1 liter of milk selling for JPY198 (NZD2.13) in a discounter supermarket.

Infant formula in China is increasingly dominated by domestic brands.

A mortgagee sale can easily result in a 15% discount on a market sale by other means, in certain circumstances.

They choose auction because it allows the perception of a 'hands-off' selling approach to show that the price was fair market value, when ironically choosing the method they do results in anything but.

AND the price to the owner is less of a concern to them than is selling at a price that covers their lending.

All this is true and is when there is a breakdown in communication between bank and mortgage holder. Where their is some payments being made and good communications, banks are currently choosing to not foreclose.

Its interesting how accounting rules may come into play , but they have also been told by RC into banking to treat customers fairly....

Its an interesting one to watch playout.

They are way less concerned about forcing sales of investment property.

"Defaulting doesn't cause house prices to suddenly drop... Who would know that the property is in default ?"

Welcome to the internet age where google can find out all sorts of stuff - and a bit of leg work can find out even more. (A phone call to the agent can be all that's needed.)

I've never bought any property - or even made an offer on one - without finding out the situation of the owner first.

https://www.nzherald.co.nz/business/auckland-property-investors-urged-t…

"The RBNZ said it was “encouraging” the increase in borrower stress had not accelerated." and what about the enormous increase in listings over March 2024?

"The basic problem can be seen in the March figures, when Realestate.co.nz received 11,455 new listings, but in the same month the Real Estate Institute of NZ recorded just 6521 sales."

I do believe those are related to increased borrower stress but the banks have decided to give them time to offload. Everything to avoid the mortgagee sales!

If they're early in a 30 year mortgage, say in the first 10 years, they'll have paid off so little of the principal that interest only won't have a huge effect when incoming money from wage/salary is zero. They could seek a repayment holiday for a few months ... while they line up a destressed sale ... or if they're lucky, find another job that'll probably be paying less.

Methinks the banks are optimists. This one will be every bit as bad as the GFC.

Remember the RBNZ slashed the OCR from 8.5% to 2.5% very quickly when the GFC hit. And yet all the pain came way after and lasted for years. Jobs went, mortgagees sales took off, skilled people left NZ for better paying jobs overseas, etc. etc..

This time it will be different? Alas no. Economies are like oil tankers ... slow to stop, slow to start and slow to turn around even if there is water to do it in (and NZ has little water to make the turn in as overseas markets won't be riding to our rescue like we had with China in 2008).

Only 0.7% at this stage, thought it would be more as pretty much 95% of people have already rolled over onto higher rates so the only thing that will make it worse from today going forward is unemployment. At what percentage would you call it a big problem ? currently it isn't a problem.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.