Both the bulls and bears can agree the Official Cash Rate (OCR) needs to go up to curb inflation, but opinion is divided over how quickly this needs to occur.

Economists concede there is no clear cut answer around whether the Reserve Bank (RBNZ) should hike the OCR by 25 or 50 basis points at its next review on Wednesday.

ANZ chief economist Sharon Zollner says the central bank is "between a rock and hard place", meanwhile BNZ head of research Stephen Toplis maintains it's a "coin toss" as to which way the RBNZ will lean.

Financial markets have priced in a 45-point increase, according to Westpac.

When the RBNZ last reviewed monetary policy settings on February 23, it paved the way (in its commentary) for hiking the OCR in larger increments than the usual 25 points.

However, Russia hadn't launched its attack on Ukraine then. While the war is creating enormous amounts of uncertainty, raising questions over the future of global trade, it's also hiking fuel costs and disrupting supply chains, exacerbating inflation. Aggressive OCR hikes cannot curb inflation caused by such supply-side cost pressures.

But, with inflation well above the RBNZ's 1% to 3% target range at nearly 6%, there's also an argument for serious action.

A case for upfront pain to avoid inflation spiraling out of control

Zollner believes the RBNZ needs to hike the OCR by 50 points, from 1% to 1.5%, on Wednesday, and then again at its next review in May.

"Inflation is far too high. Core inflation is far too high. Inflation expectations are far too high. And firms’ pricing intentions, which have been the best inflation indicator of all, are stratospheric and at this point, still rising," Zollner said.

"The biggest regret from this starting point would be losing inflation targeting credibility and seeing inflation expectations become truly unanchored. Fixing that would require far higher interest rates, and very likely a deep recession and sharp rise in unemployment...

"For now, it’s still entirely reasonable to both hope and forecast that the inflation problem can be resolved with a “soft landing”, a relatively gentle slowdown that doesn’t involve an ugly unemployment rate. But the higher inflation expectations are allowed to go, the slimmer those hopes become.

"In that context, near-term growth risks are very unfortunate, but are not a reason to tread cautiously with OCR hikes...

"Double-speed hikes are not without risks either, of course. The housing market in particular is vulnerable – it can’t be anything else, after rising 40% in less than two years – and those two years being a period in which New Zealand Inc became poorer via the loss of tourism...

"At this stage, it’s a case of pick your poison. Yes, aggressive hikes now raise the odds of a hard landing for the economy in the near term, but going too slowly would raise the risks of an even harder landing further down the track."

A case for caution and letting the markets do some of the heavy lifting

Toplis "hesitantly" expects the RBNZ to hike by 25 points on Wednesday and then 50 points in May.

He noted how the situation in Ukraine had developed since the RBNZ last reviewed monetary policy settings. What's more, higher mortgages rates, the "cost-of-living crisis" and falling house prices have sent consumer confidence south.

"Were the RBNZ to hike 50 basis points in April, then we have little doubt the market would fully price a further 50 basis points for May and, most likely push the terminal rate through 4.0%," Toplis said.

"This has the potential to drive the household sector into much greater submission than might be considered optimal...

"A further 25 point nudge in the cash rate, accompanied by a stern warning that a more aggressive interest rate track will likely be forthcoming, when it releases its May Monetary Policy Statement, might be a better approach.

"This would largely keep the mortgage curve where the RBNZ wants it, allow the RBNZ to get public buy-in with stronger rate moves if uncertainty diminishes, while reducing the risk of throwing the economy quickly into recession if the adverse impacts of the war and Omicron multiply.

"Many folk point to what the Fed is now indicating as justification for the RBNZ to move more aggressively. We do not see it that way. Rather, the Fed’s leanings validate what the RBNZ has already done...

"For the RBNZ, it is the domestic mortgage curve that best represents the yield curve that will have most impact on the local economy... If the RBNZ was to raise rates only 25 basis points in April, this would probably still be sufficient to see mortgage interest rates head higher...

"Our current central view is that the cash rate will peak at around 3.0% early in 2023... This would amount to a cumulative increase in the cash rate of 275 basis points, in under 18 months. This is an aggressive tightening by anyone’s standards.

"Only once since the implementation of the Reserve Bank Act have we seen a bigger move. That was during the Bollard reign when the cash rate was increased a cumulative 325 basis points between December 2003 and July 2007. The criticism back then was that Bollard was not aggressive enough. This time around the speed of adjustment is almost certain to be much faster."

162 Comments

Remember the RBNZ has moved the OCR as much as 1.50% on past occasions. You cannot rule out that they will only hike by 0.50%. While it is unlikely they will hike in a greater increment this time (despite the need to - note UN Food Price index +30.5% in the past year) should they do so then it will indicate the Kotuku has taken flight, or is that fright?

Either way, Mr Kotuku has excess adrenaline in his system.

The RBNZ is way too late and too timid in tightening monetary conditions. They need to raise the OCR to 2.0% right now, and to 3% in May. Anything less will simply force the RBNZ to go even higher later on.

... yes , a mea culpa that they got it wrong & overjuiced the housing market would redeem some of their lost mana ... rather than double down on their mistakes , and undo the error too slowly .... 100 points now , a further 100 next month ...

The government needs to cop a " Will Smith " too , for given the Reverse Bank an extra mandate ... Orr's sole focus ought to be the inflation rate ...

Imagine what it would do to the exchange rate and carry trade

Imagine what it would do to the exchange rate and carry trade

The carry trade is not what it used to be. Have you seen JPY recently?

NZD will tumble making inflation higher if rates are not raised .50, NZ has to do whatever the FED tells them . With emergency rates still in place housing market has been over cooked a 40% to 50% decline should be expected over next couple of years.

Agree it has to be 50bps. If the market has already priced in 45bps, then wouldn't 25bps effectively cause the financial markets to ease?

50 points - definitely.

That will lead to a better return for those with term deposits - particularly the elderly - who have had a tough time over the last few years.

TTP

In that context, near-term growth risks are very unfortunate

Yep, if RB hikes it up and the economy contracts or worse tips over, Adern and Robertson's chances of re-election will shrink and they will not like that.

This govt sends the RB smoke signals of what or what not to do and their preference will be for a slow lift imo

That’s the problem - RBNZ should be independent and shouldn’t care or be influenced one bit by politics.

In general it is independent. In practice Grant Robertson has quite a few tools in the Reserve bank Act that he could use to twist RBNZs tail. Just doesn't want the political fallout. Easier to blame the RBNZ

My view is that there is a difference between tipping the economy over, vs getting off the emergency cash injection as quickly as possible and getting back to something more closely resembling long term averages.

Anyone with half a brain can see that the fiscal response to covid was reckless and over cooked.

If that causes them to get the boot next year, that's their problem.

Our problem is that the basic cost of Putting a roof over our heads is 12x our incomes...

What's the long term average?

The rate has been trending down for decades, the assumption being the economy needs juicing because growth stalls as an economy ages.

Like, I know there's a big boner for the current housing "crisis" but it really looks like only a small component of a larger problem.

Perhaps our quality of life has peaked and we just haven't accepted it yet.

Perhaps our quality of life has peaked and we just haven't accepted it yet.

Do you say this renting or siting in you sofa inside your own house?

fluffybunny

It was the monetary policy not the fiscal policy that was overcooked.

The difference is crucial.

KeithW

It was the monetary policy not the fiscal policy that was overcooked.

The difference is crucial.

KeithW

As usual, you're on the money Keith.

Indeed. The fiscal policy saved the day. The monetary policy drove credit money into asset bubbles - for what?

Keith, fiscal policy includes the use of government spending to influence the aggregate demand for goods and services and inflation. I'm not sure that that's gone so well.

Anyone with half a brain can see that the fiscal response to covid was reckless and over cooked

Quite an ironic statement, the fiscal response was not overcooked, it was the monetary response that was overcooked, it seems you may have used the wrong half of your brain for that post. All good though you got 30+ upticks… It sadly confirms once again the level of (mis)understanding of many commenters...

Yeah, that was weird. Fiscal was underdone, if anything (and in the view of the RBNZ too).

people were drawn in by emergency rates and FOMO now we are starting to get back to real world everyone who jumped into market at 6 to 12 X income will be under pressure as prices fall and they have to come to terms with loosing deposit and in negative equity for years.

Your predictions are as accurate as your spelling. Losing not loosing unfortunately

DTRH is losing out

Their chances will shrink HW? They've gone already. Women (who gave her the last election) have flipped from Ardern in large numbers already, the yield curve has inverted in the US a couple of times in the last month or two, so a recession is on the cards there, and we will follow. Labour's economic ineptitude is moving toward full bloom. Batten down the hatches people. Winter is coming.

Yawn its going to be another 25bps rise. Could be wrong of course but its not me that's wrong its the RBNZ because it should have already done a couple of 50bps rises starting back in Feb .Better for me all round if it goes up, can only dream of a 4.8% TD rate I had in 2014. Glad I put money away for 12 months and not shorter thinking the big TD rises we just a matter of days away, 2 months in and its not moved an inch yet.

I'd almost guarantee you'll see a 12 month TD with a 3 handle from a well-rated bank by the end of May.

Probably so, but even it will be insufficent return to compensate the depositor for inflation.

Carlos67 - You say a 25bps. Most people on this site voted with upticks that most of your forecasts are wrong. Going by that, Im going to say it will therefore be 50bps .

"Reserve Bank between a rock and a hard place, ....."

Are they themselves not responsible for creating this situation ?

Even now will fail to take hard decision required - for long term gain, short term can be delayed but not avoid - choking / slow death has already started .

The Labour Govt in their profound wisdom changed the RB mandate (not more mandates aaargh)

Tied Rb hand behind back so I do not think you can lay this situation we are in at Rb feet

Exactly. The dilemma is a creation of the RBNZ's own making. The rollback in interest rate to rock-bottom levels in 2020 was an accelerant that set the housing market ablaze with a 40 % rise. Now??? Dilemma. Solution? Afraid to douse the fire because the housing market is too sacred an animal to be sacrificed or even hurt.. So kick the can further down the road with a timid 0.25 bps.

It would appear we are at, if not very close, to the point where it’s very hard, if not impossible, to kick the can any further.

Central banks have succeeded in doing so from 2008 - now, via falling interest rates and QE.

But the inflation we are seeing is like central bankers kryptonite. It makes their position and philosophy very weak. They need the risk of deflation so that more QE can be used. Real inflation that isn’t transitory destroys everything they have done of late because they have no way controlling it without destroying the economy - and people realising how weak our economies really are when the solution to every problem cannot be resolved simply be creating more debt via ever decreasing interest rates.

Isn't the question now 50 or 75? They can't do 25, that would be negligent.

Nope its already been a case of being negligent months ago, just watch them add another 25bps just for confirmation. The Titanic was able to maneuver faster than the RBNZ.

That was negligence with plausible deniability. The picture is so clear now they'd be tattooing the word on their foreheads.

I should clarify I don't believe RBNZ have acted in a way that is negligent. They actually showed some bravery being one of the first of the herd to exit transitory la-la-land, and make no mistake, Central Bankers are a herd-bound breed.

And the housing market it captains is unsinkable…full steam ahead with zero interest rates through a pandemic, outbreak of war, and global supply restrictions.

Would love a 50bps, but don't think it will happen..according to anz, 50 bps rises next 2 meetings.. wow.. there'll be a lot of people reeling... we'll start to see a rise in mortgagee sales later this year... B&T will have to reintroduce their 10am mortgagee slot

Wow I just gave a thumbs up to a DGM.

I agree with you both - it will be .25 unequivocally

Their credibility to fight inflation is way more important than protecting the property market. The time when they had the luxury of protecting asset prices has passed. It's clear the US is about to move in 50bps so RBNZ will be comfortable in doing so also.

The RBNZ moved before the FED so is already ahead of the ball... At least in that respect. Much like our banks are already ahead of the RBNZ.

Exactly the market swap rates are already moving ahead of the too slow central banks.

No real accountability.

They screwed economy fundamental with their manipulation of TRANSITORY INFLATION, when everything was pointing towards hyper inflation as early as January 2021 but ...........

Even current democratic system needs to be made better as today once elected are worse than ....as give them license .......till next election.

They screwed economy fundamental with their manipulation of TRANSITORY INFLATION, when everything was pointing towards hyper inflation as early as January 2021 but ...........

Disagree. Inflation (not hyperinflation) was way out of control even before Covid. Most people are just not aware of it and what inflation is. People generally think that the CPI is the best measure of inflation. They think the real rate of inflation is thereabouts what is reported in the media or announced by the politicans.

Furthermore, it's clear that Orr and the smart people will prefer financial repression over the bubble. The NZ economy relies on the bubble so they will want to prevent its demise at all costs. They will justify their actions internally but this is also about their own self preservation. Imagine being held responsible for the collapse the bubble. Look at the RBA across the ditch to get an idea of how they might behave.

Jenny to say that Mr Orr is in deliema is not correct as it is not him but economy and through economy, it is we the people who are screwed.

He is experimenting with other people's life and money so where is the deliema, this discussion of .25% or .50% is in public but he is clear in his mind that it will be .25% and has no deliema and this 0.25% also as is forced.

All to social news suggests that central bankers are screwed but reality is that it is not them but we the people are screwed

https://markets.businessinsider.com/news/bonds/fed-balance-sheet-reduct…

Hmmm....burn every person in NZ with hyperinflation, or dent the ego of a limited number of housing speculators. Should be a no brainer but with Orr you never know.

Even if he does not rise as required, is bad for people.

https://www.cnbc.com/2022/04/07/carnage-is-epic-in-bonds-due-to-feds-in…

To throw young workers and savings-dependent pensioners under the bus to protect speculators (again)...or not?

The RBNZ and many other central banks are in a dammed if they do or dammed if they don't situation. Either way this is not going to end well. It's clear that inflation is going to stay higher for longer. The world continues to get inflationary shocks and there are more to come. The Ukraine and Shanghai are recent examples of these. The conflict with Russia won't be ending anytime soon and an attack on Taiwan is still a risk.

"This has the potential to drive the household sector into much greater submission than might be considered optimal...

"A further 25 point nudge in the cash rate, accompanied by a stern warning that a more aggressive interest rate track will likely be forthcoming, when it releases its May Monetary Policy Statement, might be a better approach”.

Isn’t this what the RBNZ did in February? Can’t keep kicking the beaten can down the road forever. Orr maybe they can.

Kicking the tin down the road has been the approach so far - can delay ( though not now as the process has started) but cannot avoid the inevitable.

Like life cycle of birth and death, economy cycle cannot be avoided though can delay death but than will be a painful death and even morphine ( printing and distributing cheap and easy money) will not help to soothe the pain.

14 years….

That is how long we’ve managed to kick the can. GFC 2008 - now.

But the ability to do so gets even harder every time because each time the central banks intervene and save the debt/asset bubble, the intervention has to become more extreme and with greater and greater unintended consequences. It might get to the point soon where even joe blogs on the street has more economic common sense than our central bankers…because they have corrupted themselves in the persist of making the unsustainable (debt growth) sustainable. Like any other state system that has control and never wants to admit that it has made mistakes, so it simply doubles down on its errors - completely lacking in humility and transparency.

It's the most massive case of welfare dependency we've ever seen. Traditional "beneficiaries" have received a pittance in comparison to the wealth transfers to these folk over the last years.

The OCR should not have been lowered way back in 2015 and then we would have gone into the pandemic with a lot higher OCR much like we went into the GFC.

Nothing is in isolation... house prices would also have been lower, a good thing for many

But this is about the Fed…if we raised rates it would have strengthened the currency and hurt our exports. Imports would have also been cheap giving lower measured inflation or even deflation.

All roads lead to the Fed and their monetary policy. It’s hurting countries all around the world because they don’t have the same capacity to devalue their currency at the same rate as the Fed and hence why we are seeing countries get into financial difficulties.

Orr will go hard and fast with 0.25% - no regrets...

Nifty1 you are absolutel correct as for likes of Mr Orr even 0.25% as forced is hard and fast.

When banks say they have 'priced in' a 45 points rise on average, that basically means they have gambled on that increase and they will make money if they're right.

If you look at year on year change in credit card spending, house sales, rents, house prices, wages etc they are all turning the curve sharply. Demand is already crashing because consumer confidence is slumping and high prices of imported, non-substitutable goods like oil are sucking disposable income out of the economy. Mortgage rate increases are scheduled in throughout the year as fixed terms expire, which will add to the demand reduction.

Hiking rates in this environment is a recipe for unemployment, which will reduce demand further and create a doom loop. And, the idea that crashing demand will reduce the prices that are driving CPI up (petrol, building material, rates, insurance etc) is really, really stupid.

Watch Bank of Japan and ECB this week. The former has already taken control of thebyield curve. I think ECB will do the same. They will be proved right

Joe, just last year 5 year mortage was appox $97 per week and today is appox $138 So is rise of appox $40 per week per $100000. So earlier for a 1.1 million house with 20% deposit was appox $900 per week and today will be appox $1240.

Yes, and people will be increasingly exposed to those increases as their fixed terms expire. My point is that the impact of the mortgage rate increases on aggregate demand is ongoing and increasing - we have already got some big demand reductions programmed in.

He will go with 0.25% as it will be best to reduce the damage to mortgage holders. Raising it too much will potentially crash the economy. A lot of fixed rate mortgages will be coming up for re fix later this year and will cause major inceases to servicing the loans, potentially leading to negative equity for recent purchases.

Your logic doesnt hold water, it aint all about mortgage holders, thats a narrow view of the world. Negative equity is going to happen, mortgagee sales will happen, mostly to the overstretched, ranger and jetski, speculator leveraged up the wazoo types.

He will go with 0.25% as it will be best to reduce the damage to mortgage holders. Raising it too much will potentially crash the economy. A lot of fixed rate mortgages will be coming up for re fix later this year and will cause major inceases to servicing the loans, potentially leading to negative equity for recent purchases.

These are unusual times calling for unusual solutions. My solution would be to freeze mortgage interest rates and bank deposit rates. Deposits could still be made but only the withdrawal of a set small percentage of deposits would be allowed over a set period much like the prescribed process of the OBR. This would allow the banks to retain their liquidity and for a time few if any more new mortgages would be created; it would be explained to the banks that they have made exorbitant profits over the past few years and that now is the time for them to give something back. This process would effectively remove housing interest rates from he inflation index.

I can't see any evidence that the price of fresh vegetables has unduly escalated in past weeks. Perhaps local growers in the likes of Kumeu, Pukekohe, and Bombay would be permitted to open dedicated off-road selling stands in highly populated areas. This should lower or remove fresh vegetables from the index.

An adequate warning that families from now on can't have more than two children if that would mean sponging off the tax-payer to feed them.

No hang on, it's already working itself out. It should be explained to the homeowners that they have made exorbitant profits over the past few years and that now is the time for them to give something back.

I'll look forward to explaining to my bank how I can't possibly be in negative equity because apparently I've made exorbitant profits despite only owning one home and never selling it.

Quite a wide ranging review there Streetwise.... excellent by the way

I agree - but then again we shouldn’t have used the wealth effect and increasing domestic demand by reducing mortgage rates to crazy lows in the first place.

A principle of the world is that you reap that which you sow…we created this situation through our decision making. Now we must deal with the consequences. But we have created a society that wants to benefits without the consequences.

We want cheap mortgages, exploding debt levels, and some of the worlds most expensive houses?…well good for us. You can have those things but history and principles say that these inputs almost always result in financial crisis including widespread debt defaults and a resulting crash of some form. So are we sure we want the housing market that we have? Apparently if it is a no (because you can see the consequences) you are a doom goblin.

We have behaved in an ignorant fashion and ignorant people create the conditions for bad outcomes.

Yes.

People remortgaging now will mostly have mortgage rates starting with a 4. Do they really need to start with a 5 or 6.

5% or 6%, or even 7 or 8 or 10%, is still much lower than it has been at times in the living memory of Generation X.

Knowing that NZ was at historically the lowest interest ever rates in my lifetime, and knowing that rates couldn't drop down much further, the approach I took was to mitigate the risk of rate increases occurring, so I fixed for 5 years. Then when the rate did fall about 1% lower and when it became clear that rates were starting to rise, I did the maths and worked out that it would be worth the break fee cost. So a year ago I re-fixed at the lower rate, also for 5 years.

Now, I have a rate of 3.39% for the next 4 years, and interest rates are unlikely to fall from where they are now in the next 3 years, and likely to increase further given that inflation is still much higher than some current mortgage interest rates, and no bank will want to make a loss on the loan, let alone lose their capital to inflation.

That means I still have 4 years at 3.39% to continue to pay off the mortgage as fast as I can.

Even if interest rates are 10% in 4 years from now I'll have paid enough of the principle back to be able to afford a 10% interest rate with only a couple of months impact on finally paying it off compared with the current interest rate.

Admittedly I had a good sized deposit, and I bought in a part of NZ that had lower house prices.

Ya gotta do what ya gotta do to get security, and if that means relocating, then that's what ya gotta do.

Those who don't stress test their ability to pay higher interest rates and factor that into their long term planning, and took out a large mortgage with only a tiny deposit and little head room to accommodate interest rate increases are doomed to wear the cost of their own decisions.

Comfortable middle class Gen X households selling their 1 mil houses and trading up to 2 mil houses. Borrowing the difference. 1 mil at 2.5%. 25k per year in interest. We can afford that on our 160K combined income! Why not. The new house will be worth 3 mil in another 3 years. Nek minnit they are re fixing at 5% and mums 70K salary is completely used up to service the mortgage interest alone. Heaven forbid that one of them looses their job.

In Q4 2022 354 million lent to 291 Auckland Owner Occupier borrowers (not FHB) with DTI > 9. 1.2 mil average with average income 133k. Very low risk for the bank. LVR is fine . Prices would need to half before the bank is at risk of loosing if they foreclose on you . The mortgage is full recourse anyway. But that family will be wiped out.

The RBNZ has laid a mine field and now they are walking though it. Just hope they have the data on where the mines are.

Well said except it's 'losing'

Ultimately they are responsible for their own financial decisions. Can't blame the bank nor the RBNZ, nor the government. If they choose to over extend themselves then that is their own fault.

David

Well done on a number of accounts:

- Breaking terms albeit at a cost can be advantageous. Over the past decade with low/falling interest rates most have gone for short terms and breaking a term has not been common but with upward pressures it needs to be more widely considered

- right move going long term as the signals from the RBNZ and bank economists has been that the emergency low rates are over and the RBNZ have indicated steady rises in OCR

- really great to see you being prudent and paying down your principal.

Your post is by far one of the better ones I have seen for some time on this site.

It only took 6 months to recover the cost of the break fee through saved interest.

If your considering a loan, then do your maths with at least 5.5%.

Are you me?

Well you did say that you had made your last post. Hurry up and get off

I see you are still making well informed and intelligent comments.

Not.

Reminding you of your own own foolish words Monsieur Mouse... its time you ate your own words and be true. There again you often make foolish and misguided attacks on other genuine commenters. So whats new for a lifetime renter

Nasty comment Flying High.

Very nasty indeed.

You insult someone by calling them a "lifetime renter" because it makes you feel strong and clever about being a house hoarder. But frankly, it shows you to be a nasty person.

A person's value is not determined by how much real estate they own.

You excuse house mouse for his insults and then add a few more angry insults for good measure. I am allowed to hold my own opinions, which are not what you are trying so desperately to imply

Btw why did you edit your pejorative comments, your mouth running away from you huh

Anger issues? Drinking again Flying High?

I cannot wait for the airlines to start operating fully, so we can fly anytime and anywhere. I guess that will bring down inflation as ticket prices drop :)

Excellent comment Jfoe

Excellent comments from Toplis, as I have said before by far the best bank economist.

"For the RBNZ, it is the domestic mortgage curve that best represents the yield curve that will have most impact on the local economy... If the RBNZ was to raise rates only 25 basis points in April, this would probably still be sufficient to see mortgage interest rates head higher...

Not productive GDP qualifying investment.

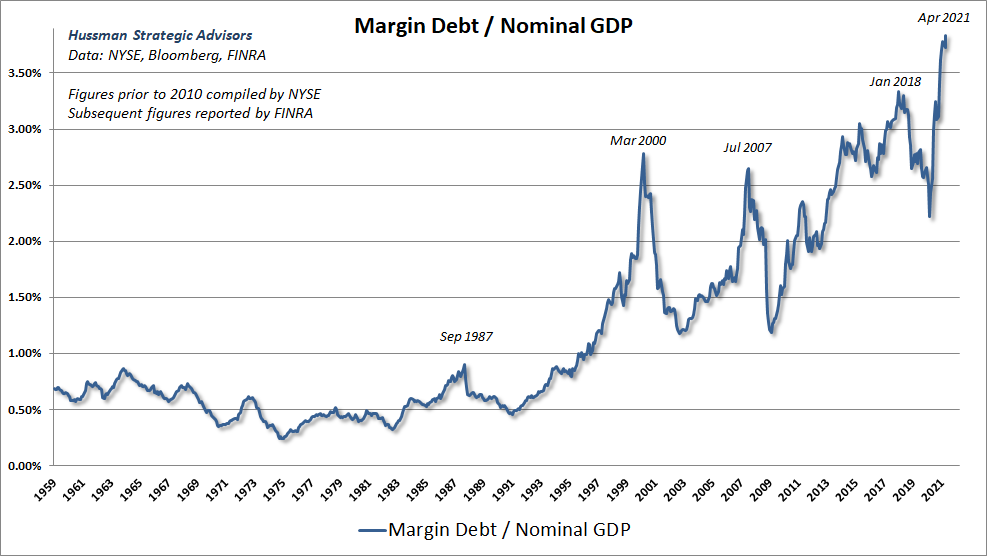

Policy makers sometimes flatter themselves with the idea that holding interest rates at untenably low levels makes it cheaper for borrowers to obtain funds. Unfortunately, it does so only by transferring income from people who are trying to save for the future. Replacing Treasury securities with base money may make savings more “liquid,” but it doesn’t suddenly make people abandon their retirement plans in favor of consuming today. Low rates also don’t magically create productive investment opportunities.

What economic activities suddenly become viable at zero interest rates that were somehow not viable before? Only projects so unproductive that any positive hurdle rate would sink them. The main activities that are encouraged by zero interest rates are activities where interest is the primary cost of doing business: leveraged real estate transactions; “carry trades” that employ enormous amounts of leverage to profit from small yield differences; and speculation on margin. Presently, margin debt as a percentage of GDP is at a historic extreme.

https://www.hussmanfunds.com/comment/mc210614/

{kind=link}

Oh God. Every person of influence should be forced to read that last paragraph from Hussman for as many times as it takes to sink in.

Yes and you can see the correlation in the margin debt/gdp chart with that of our own housing market.

Its almost entirely reliant on falling discount rates…if discount rates ever rise it will collapse as the the income can’t be generated to create a positive return (call IRR/NPV or whatever you like) to sustain the price of the project/house.

People should remember that the RBNZ is not mandated to raise the OCR. Rather, it has a mandate around CPI inflation and employment.

Is raising the OCR really going to meaningfully address the CPI? It will certainly affect the economy and ultimately employment.

Demand is dead in the domestic economy, as is the housing market. What is hiking the OCR going to ultimately achieve, other than bringing the economy down?

sure it might strengthen the dollar a little bit more, but that’s a pretty marginal effect.

Given all this, I think the OCR decisions this year are to a significant extent symbolic, to make it look like the RBNZ is doing something meaningful. That’s why I think we will see 25 BP hikes.

If OCR has no effect and is only symbolic than why not raise it by 1% - if have to experiment and is only symbolic.

If can experiment by lowering leaps and bounds, surely can try in hiking as well.

And totally destroy the economy?

nope

But what I think you’re missing house mouse is that they have already destroyed the economy.

As opposed to what it sounds like you are saying which is that the current economy is good/ok if it were to be left alone.

Its not, it is currently broken and if left unchecked will be a disaster.

I agree in many respects they HAVE destroyed the economy - and it's the productive, 'real' economy. By taking the OCR too low, they massively inflated the housing bubble and have killed the financial futures of many young kiwis, It will push out of the country many of the skilled young kiwis that we really need. So yes, I agree in that respect.

However, on the other hand I fail to see how sustained hikes to the OCR will really do anything to undo that damage in a meaningful way. Yes it might crash the housing market by 20-30%, but that doesn't bring house prices down to anywhere near affordable levels. And bringing house prices down a lot is not in their mandate, anyway... in fact it could be counter to aspects of their mandate, including financial stability and employment.

And it will create others damaging effects.

I just don't think the RBNZ can undo it's poor decisions and their consequences, from 2020 and 2021. I don't blame them for their original cuts, everyone thought covid was going to be a disaster for the economy. But they certainly were far too slow in liftng the rates again from their 'emergency' lows.

There's a real risk that in trying to appear as if they are doing meaningful things by raising the OCR, they will generate a whole range of unintended consequences.

Yes agree - it’s a difficult situation.

The key point from my perspective is that every time we avoid pain (recession) we are creating unintended consequences. And you are worried about the consequences of recession…yet recessions are natural and healthy despite being painful at the time.

Our desire to avoid pain, at all costs, might appear to be good in the short term, but in the long term, it’s very damaging. Zombie company’s continue to get life support and become a drag on the economy, inefficient debt and capital get allocated to projects and assets that they shouldn’t be, bad investments have the appearance of being good investments…there are a number of bad unintended consequences of not allowing the recession to occur. Slowly the quality of the economy and society erodes.

We are in serious need of a recession at present so that can determine what is real and what is fake….at present there is a lot of fake parading around like it’s fantastic (be it businesses or debt speculators)…we will very quickly see who and what has been swimming naked…we can then point and laugh at them for a while…before redirecting those businesses and individuals to get out of the water, put some clothes on and focus our efforts on swimming together as opposed to people with no togs trying to drown those who do have swimwear.

Good perspectives, your comments are always well thought out.

... the recession we need to have to wring the excesses out of the system ... the monster property bubble needs a little prick ... Robbo & Orr have overspiked the punch bowl ... this party has to end some time ... now ... or keep kicking that can down the road ?

Is demand really dead in the domestic economy? Seems more 'lumpy' than 'dead' to me.

There are still people buying SUVs as fast as they can be imported. Builders and landscapers of all sorts are still run off their feet. There's still a cafe on every block (maybe not for much longer). Our economy is so housing-dominated that I suspect most of the money funding those things is ultimately property-based. So interest rates should actually work really well because they hit mortgages directly.

It'll be painful to see the cafes shut down. But we've made this bed for ourselves with maddeningly complacent and greedy policies. If I'm choosing between 'mortgage-holder has to cancel gym membership' and 'family living in a garage can't afford to eat anymore', I know what I'm choosing. And that is the choice to be made.

Exactly..

Disagree. "Demand" is not dead. Plenty of people are spending - and on things other than food.

Yes - credit cards have been put away, but that isn't a bad thing - only banks win out of credit cards, and people thinking strategically for the long term will take advantage of present circumstances and get good deals.

Maybe ‘dead’ was an exaggeration. But demand is certainly pretty sickly.

How do only banks win out of credit cards?

I pay mine in full every month and meanwhile that money sits offsetting part of my mortgage.

Oh and I get cash back on my purchases for the trouble.

When I was working for a bank, something like 50% of people paid off their credit cards every month. About 25% were where they made their money and it was essentially the poorer end of the market who could only keep up the exorbitant interest rate payments. IMO for these people the banks are basically legalised loan sharks, but at least they don't employ people with baseball bats?

Yeah agree, went to a test drive with a dealer. Sales person is trying to set me into FOMO mode by showing their stock level in their data base. Most recent upcoming shipments have been already pre ordered. Nah, it doesn't look like a recession to me soon even if ORC hiked to 3%. For popular items, most people are struggling to find stocks instead of struggling to have enough money to pay for them.

Yeah but you know most of those cars are bought on credit via the "value" of their house right? That's why when house values drop, suddenly there are a lot of cars for sale...

So it is a toss between soft landing and hard landing and no one knows, so why have reserve bank :

1 : They created the mess by going overboard with emergency measure.

2 : Can understand that they panic and went overboard but why did they not take reverse action when it was clear that inflation is running towards Hyper Inflation.

3 : If they too are tossing the coun and have no control, why have them and pay to experiment.

4 : As they manipulated and lied when it was evident just after six months of pandemic that measures are though activated should be pulled back, they did not.

Just like lotto result are live on TV, let the finance minister come live on TV and flip the coin to decide and save millions on RBNZ.

There are alternatives but none of them is a soft landing.

The soft landing option has long since gone

KeithW

... I was in Australia back when Treasurer Paul Keating said " it's the recession we have to have "

... all hell broke loose in the media after that comment ... but , he was proven correct ...

Same here , same now : we need a recession to flush out the economy , a good dose of economic epsom salts to cleanse the financial system ...

11% Unemployment. 17% for 20-25 year olds. Beyond the comprehension of most people today.

Careful Keith! You might be labelled a Doom and Gloom Merchant with that kind of attitude!! :D

Simple solution - raise the interest rate up by 1 whole percent, not merely half or a quarter.

The banks all appear to have already factored in a minimum 0.5% rise and we need to get inflation under control.

... second solution : remove the mad mandate this government put on the Reverse Bank to also focus on employment ....

Give Orr just one chore : control inflation ...

We are at record low unemployment. Everyone is just stealing staff from competitors and paying more for the privilege. It like Orr wants more inflation, not less.

Why? Through what channel or mechanism would that make any difference to the price of things / cost of living? You might get a short-term 'sugar hit' on the strength of the NZD I guess - but at what cost?

Most commenters on this website are throwing out such statements without any rational basis.

The only rational basis seems to be a desire to destroy the housing market, which I get because it's been to stupid and damaging, but....

There's just no way any increases are going to be 75 or 100 BPs, even 50 BP's is only an outside chance.

Inflation rates are the highest they have been in 40 years. Globally. And they are rising fast. Many other smallish economies have been raising 100bps at a time. These are unusual times, so it makes sense to expand our definition of "possible".

It's not going to happen, and it shouldn't happen.

All I'm saying is that things are already happening that none of us saw coming. Remember when we all thought that inflation was dead? The future might bring lots of surprises.

Perhaps we need to look to ego to deduce what will happen on Wednesday.

And by this I mean that apparently we were the first country to start increasing the interest rates since Covid hit, and now we have a chance to be the first country to bump interest rates by 0.5%. A chance to say you're leading the world - who wouldn't take it?

But wait ...all the signs are out for a global recession of some size.....Grant Robertson and Adrian Orr together have burnt their chips...and they really have no room to throw money willy nilly around again like they did with their Covid response. Saying a morning karakia is not going to help Adrian one bit...with the coming financial pandemic!

With interest rates at 0%, if we have an even greater fiscal intervention with falling gdp it’s possible that we create even more inflation and end up in an even bigger hole..

i.e. even more $$ chasing a lower quantity of goods and services produced within the economy.

Is the author of famous book Rich Dad Poor Dad right :

https://finbold.com/robert-kiyosaki-warns-rising-inflation-will-wipe-ou…

Real state agents are still trying to invoke FOMO to lure FHB.

They are very well aware this recession / downturn will be different and worse than anything witnessed before, so is real shame. Can feel the pain and the recession has not even started or has just begun.

As they say Karma is a Bitch.

... no .... he's wrong ... very wrong ... he claims " America produces nothing but bubbles " .... that sort of dumb rhetoric shows that Kiyosaki ( whose earlier books I enjoyed ) is himself blowing hot air ....

I thought they'd do 50bps last time, there hasn't been any substantial change in the underlying case so of they went for a 50bps raise now it'd appear inconsistent.

"Yes, aggressive hikes now raise the odds of a hard landing for the economy in the near term, but going too slowly would raise the risks of an even harder landing further down the track."

The case for aggressive hikes right now could not be any clearer.

The chorus of hawks today is something to behold. You realise that you are all shouting for higher unemployment right? Because 270,000 kiwis wanting a job or more hours is just too low a number?

Would you also agree that if NZ needs this army of involuntarily unemployed people to supposedly suppress wages and prices, then they should at least be paid for their trouble - put unemployment benefits up to minimum wage maybe?

Imagine living in a village 1,000 years and a couple of the landlords start asking for more rent, or the farmer wants more gold coin for his potatoes, or the price of a new thatched roof gets too high because of a dispute between some other villages. Would the solution be to put some people out of work?

The chorus of hawks today is something to behold.

Yes it's quite bizarre.

As I say above, I think it's often coming from an understandable position of wanting to see this very silly and destructive housing bubble pop.

But popping the bubble is NOT the RBNZ's mandate...

I agree on the need to increase the OCR, but the levels some people are talking of are quite silly.

This is more of a critique on central banking and fiat money. If the USD was still backed by gold similar to your example, the banks couldn't recklessly inflate the dollar into worthless, causing asset bubbles sensitive to economic contraction. I get that if there is an actual food and energy shortage whatever the central banks do doesn't really change that. They control the money supply, not grow crops but nobody on this site created the rules and inflation targets, or took the world off the gold standard, central entities did.

Appreciate the considered response.

A critique of fiat? Perhaps. I guess my point was that real resources are what matters. So when real resources get harder to get, take more hours of labour, more time to deliver, then the price of those real resources go up. Increasing the cost of credit in the village or in NZ doesn't change that. In fact it could make it worse.

No, I agree. I think the reason for the inflation matters absolutely. Increasing interest rates so people pay more to service their mortgage doesn't grow more food.I just feel its likely that central bank haven't given this sort of consideration in the past. Maybe they didn't have to lower interest rates so low in the past decade, maybe deflation in consumer goods was OK if caused by globalisation and technology but they lowered rates and caused massive asset bubbles. It would have been good if there was some entity in place to identify that maybe an asset bubble is an indicator that the central banks have got it wrong. Like Housemouse said, mostly people want them to act now and increase as they acted when the decreased, more to reduce asset prices to reset or balance the market.

Exactly. Mind you, most people who comment on this site are wealthy boomers who have benefited from successive programs of austerity and monetarism, and have come out the other end with a big fat term deposit, a mortgage free house and a Ford Ranger. Stuff everything and everyone else.

It's their choice to hike 25 or 50 at any time. But as many people mentioned here, the longer they wait, the higher OCR goes, the bigger hikes they will need to do. Inflation doesn't go away by itself.

Absolutely correct. Wish it were otherwise ....

No one seems to be talking about the possibility that CPI inflation in the next 1-2 quarters may not be as high as people assume.

Fuel prices have been somewhat tamed, and we have half price public transport for a few months.

rent inflation is flattening out.

the big question is what will happen to food. Hard to see groceries increasing much more, and very hard to see the cost of eating out being able to sustain increases given it is discretionary.

Foodstuffs and Progressives can absorb the increases. They've been ripping us off for years :)

Yeah, and they must be conscious of the public angst on the issue of rising food prices. I can't say for sure, but I would have thought that might start to play on how much they consider rising their prices from here.

Also, nothing like high prices (eg. on some veges) to bring down demand for a particular item, and hence moderate prices!

Some of the stuff I import is being quoted at 70% increases, I would say we will average out at 10% this year, we pushed 10% last year and were still going backwards with the freight craziness. Im picking we arent alone in this.

The government forced the Reserve Bank to focus on sustainable employment rather than OCR. Previously it focused on OCR. The unemployment rate looks fabulous but the reality is that focus should have been on OCR & OCR should be at least 2% now. Stagflation is now going to bite & instability of economy is now a real threat. Our populist government plans to spend lots of money in the hope of getting elected. Short-term gain for long-term pain. Such a poor strategy for this country.

Please explain why you think that thousands of people should be thrown out of work so you can get a cheap latte.

Unemployment was at record highs back in the 1990's when Don Brash was hiking interest rates every other day, and for those fortunate enough to have a job, wages were for the most part, held down.

50

It will not matter how much the RB move the OCR Economist will not be content. I think Orr has done a good job walking a very tight rope. Wow i can feel the arrow flyng

So it occurs to me how weird this all is. We have a centralised bureaucracy that makes rigidly scheduled changes to interest rates, constrained to be 25-percentile increments, whose outcome makes or breaks us. Isn't this weird? Could we rather have a world where interest rates are determined automatically by a market of buyers (borrowers) and sellers (lenders) and don't depend on the whims of a government bureaucracy? Do we really need a central bank?

We can be sure, as night follows day, that the wealthy boomers on interest.co.nz are calling for interest rates to go up to protect the returns on their nest eggs, while homeowners, low income workers, the poor, those on benefits, etc will get wiped out when the OCR goes up.

We all know higher interest rates lead to low wages, reduced services, less jobs, higher rents, higher mortage payments, and over all, more financial pain for those at the bottom, while the interest.co.nz boomers laugh all the way to the bank in their Ford Rangers from their mortage free home.

Keep the OCR as it is. For once, workers in this country are getting half decent wage increases and able to find work with relative ease. We just need to cut people a bit of slack for once, and let the working people enjoy their spending power.

Your nest eggs can wait.

3% wage increases v 7% inflation does not increase spending power.

Hiking mortage rates by $100-$200 (and rents, etc) doesnt either. Nor does throwing people out of work.

There are plenty of jobs, and wages havent been this high for 40-50 years. And people like you, with your desire for a cheap latte, want to kill it stone dead.

You assume a lot about me from my 1 simple sentence.

I don't drink latte.

And I fully support increased real wages in this country. However if inflation is greater than wage increases people are WORSE off, not better. Is there something in that you don't grasp?

Also you state wages haven't been this high in this country for 40-50 years, Really? Relative to what? Certainly not house prices, rent and the general cost of living. I believe the middle class in NZ is currently been hammered like never before.

Before your mates, Roger, Richard, Bill, Bolger, Shipley and Richardson came to power and started stripping wealth out of the workers to enrich your investment portfolio, this country had very high wages, across the board. Now after 1991, wages pretty much fell right thru the floor, and most work because casualised and part time. Minimum wage was frozen for 10 years.

Now wages are prertty much back up to where they were, people like you want to cut them again. That is wrong.

I've seen this kind of thing posted a lot and really struggle with it. Assuming your wage is in fact more (hopefully significantly more) than your expenses, it is quite reasonable that a 3% wage increase leaves you with more money after bills even when those bills go up by 7%

It only really becomes a problem if you are right on the edge, with a mortgage and bills that eat up close to 100% of your income.

We have a strong/tight labour market. Definitely enough capacity for 50bp hikes.

No. It will wipe a lot of workers out. Wages will crash and rents/mortages will go up?

Can you not realise we just need to let the working people of this country, just for once, have some sort of disposable income.

Let's be clear. It won't be possible to reduce inflation without hitting economic activity and putting upward pressure on unemployment. That is just the way it is. Unfortunately, our Reserve Bank has been behaving as though it can magically coax inflation down while simultaneously stimulating the economy. And look where it has got us. The MPC need to collectively 'grow a pair'.

That is why the OCR should remain as it is, decreased even. Too many people will be financially wiped out. Those that are lucky enough to keep their jobs will have to find a way to shit out what could be $200 extra in rent or mortage payments. I cannot understand how people like you want wages cut, people thrown out of work, and living standards wrecked, simply because you want to keep lattes cheap.

In any case, if the RBNZ hiked interest rates to Shylock-like levels, the cost of your latte wouldnt go down in any case. All it will lead to is the barista making it for you having to live in their car.

The RB has enough quality research to look through the hype and see that economic conditions are weakening and a 0.25% increase will be enough

The RB has enough quality research to look through the hype and see that economic conditions are weakening and a 0.25% increase will be enough

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.