House prices are now declining throughout the country, even in regions such as Canterbury and Queenstown-Lakes where the chilling effects of the current market downturn have been slower to take hold.

According to the Real Estate Institute of New Zealand's House Price Index, prices across NZ were 5.4% lower in June than in March.

Just as importantly, prices nationally are now just 0.7% higher than they were in June last year, meaning properties are likely to have lost virtually all of the spectacular capital gains they accumulated in the second half of last year.

The REINZ's House Price Index is probably the most reliable indicator of movements in residential property prices because it is compiled from sales made by REINZ members as they become unconditional, making it very timely, and it adjusts for movements in the composition of sales each month.

Other measures, such as median and average prices are also useful, but they can be affected by movements in the composition of sales each month.

For example, if more upmarket properties than usual are sold in a month, that can push up the median price, even though prices of individual properties may not have moved, while an increase in sales at the bottom of the market can have the opposite effect.

The HPI adjusts for those changes and gives a better indication of overall price movements.

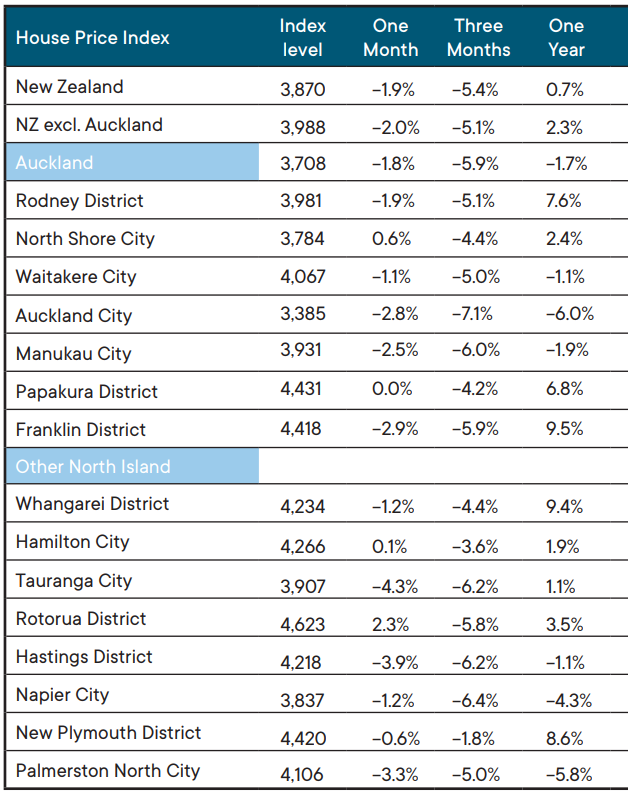

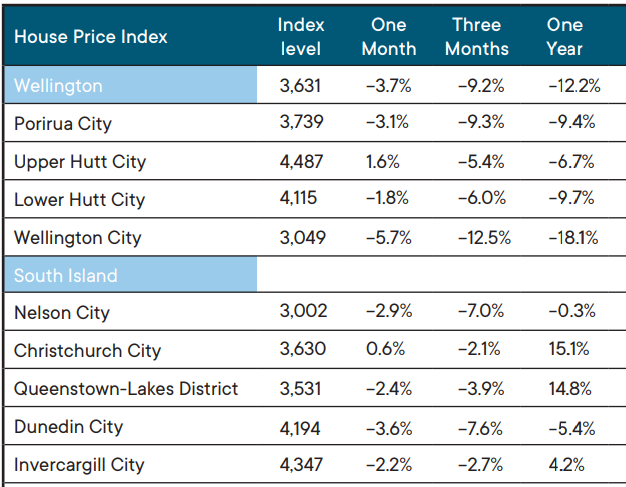

The table below shows how much the HPI has changed over the three, six and 12 months to June in the country's 23 main urban districts.

It shows that prices in June were lower than they were in March in all 23 districts as well as nationally.

And they were lower in June this year than they were in June last year in 11 of those districts, which means prices are now lower on an annual basis in many parts of the country.

The biggest price falls have been in Wellington, where the HPI for the Wellington region is down 9.2% compared to a year earlier. In Wellington City it's down 18.1% for the year. Ouch! That big a price fall has got to hurt.

Across the Auckland region prices are down 5.9% over the three months to June, and down 1.7% for the year.

Prices are even falling in Nelson, Christchurch and Queenstown-Lakes - all markets that had until now remained relatively buoyant.

With interest rates continuing to rise and an abundant supply of listings in a market that's only half way through winter, the outlook for house prices doesn't look great.

The comment stream on this story is now closed.

REINZ House Price Index June 2022

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

196 Comments

House price crashes usually take place over many, many months, and years - but already this data shows some spectacular regional falls. If the RBNZ can't ride to the rescue (and they can't for probably at least another 12 months) then these epic falls will continue.........

As an aside - it is somewhat hilarious how the REINZ and associated hangers on are doing their best to minimize and hide the on-going crash. You would have thought a better strategy from them would be to highlight it and thus try and influence the RBNZ. I am not sure whether they are just too dumb or just too shell shocked.

RBNZ get the underlying data so know what's up regardless of REINZ spin (they make their own charts using the REINZ index in their online documents).

A few "C" words are just a no go like Carlos, Crash, Crisis and a few other choice no go long term favourites.

Remember that in NZ society is divided between haves and haves-not, like everywhere but here is between speculators - so called investors and FHB and people in power, decession makers - so called experts, media.....influencer.......all have vested biased interest.....so.......but this time fundamentals have taken over and will be hard to manipulate by ........

This is the sad truth. We tell ourselves we live in a democracy, where everyone has an equal say in our government and democracy.

The truth is that capital has far more influence than any individuals vote. From influencing the media narratives and Overton window. From directly lobbying and influencing decision makers. Using think tanks and other opaque organisations to alter and influence policy. All of these elements give capital an outsized influence other the wants/needs of voters

To me the first stage in fixing this is public funding of political parties, and no donations. The usual argument to this is do you want to pay, from me the answer is a resounding yes. I am paying anyway its just through unjust laws that cost me more in the long run.

The article I saw in the Herald was hanging on the median trying to make it look like prices were still rising....

Why would RBNZ ride to the rescue?

Because their main job is to ensure that the commercial banks never end up with negative equity.

Indeed why would the RBNZ bail out speculation, as this is just a return to mean after a decade of the cheap debt driven speculation frenzy?

House price crashes usually take place over many, many months, and years - but already this data shows some spectacular regional falls.

Kind of like the ol' rat poison and other associated cryptocurrencies. Just as well everyone's in for the long haul, except the boomers perhaps.

I wouldn't be loading up on any of those retirement village shares at the moment.

Adrian 'Sitting Bull' Orr needs to retreat to his teepee, smoke his peace pipe and channel the Gods to think about where this is all heading. His tribe of 5 million rely on him.

Hopefully NZ housing market is not used as a refrence point when discussing Boom and Doom replacing Ireland.

Case study for future generation to come.

The rate of falls we are seeing really are quite extreme when compared with other major housing corrections …. Yet most media outlets and commentators seem to just keep telling everyone it’s no big deal and looks like a soft landing.

https://imgur.com/Ln6xCot

At least we have people such as Greg who can actually drill into the data. Unfortunately too many people will just listen to things like ZB or oneroof and commentators with a vested interest who downplay the nature of the falls

I was hoping you'd update this graph, Miguel. Thank you very much for posting. It is possibly the most relevant piece of information available on the status of the housing market (i.e. house market crash) at the moment.

Great work Miguel

Unfortunately too many people will just listen to things like ZB or oneroof

Or homes.co.nz. A home in Porirua I've got on my watchlist has an estimated price of $1.12m. It's still listed as for sale on homes.co, even though the seller is a family member and told us yesterday it sold in the $800,000s. So a $300,000-odd lower sale price than predicted on spruiker.co.nz...

Here's another example of Homes.co.nz being absolute garbage: I watched a house not sell on trademe for a very long time. First it was passed in at auction, then listed asking price $1.4m, then $1.3m, then $1.2m, then finally $1.1m over the course of 6 months before it was finally pulled from trademe in May. I kept an eye on homes.co.nz for a while to see if it had actually sold and I'd missed it, checked this morning and they have just updated their Homes Estimate to $1.71m! After it failed to attract any attention at $1.1m two months ago! Something is badly wrong with homes.co.nz.

You get what you pay ( or not pay ) for. Just like QV/Corelogic and Oneroof etc

dp.

Many of this website are funded - gets ther revune from real estate industry, so is heavily biased with ulterior motive.

Government should ban such website or ask them to justify their data or price.

A properties sale history has to be lodged with the Territorial Authorities, this information should be public domain. QV is a state owned enterprise for goodness sake, they should be publishing the sale prices as they occur for everyone to see.

They do (sort of). If you go to QV.co.nz you'll see the last sales price QV has received, bearing in mind they only get them once settled and reported via the councils.

That's weeks / months after the sale agreement date though which only the real estate agent / REINZ has access to and they have no obligation to publish / disclose that.

Thanks, that's quite helpful!

When selling privately I tried registering so I could list my house on there. My account lasted a day. Still, I got more than Homes.co.nz said I would, so that was a balm. Trademe is a nice big equaliser - no REA-wall there.

Trademe owns Homes.co.nz

https://www.stuff.co.nz/business/300233055/trade-me-says-deal-signed-to…

and Apax partners own Trademe

You're quite right - just looked it up on the companies office website.

Better go delate my above post! I thought it was a conglomerate of RE agencies.

What's interesting is that often the TradeMe Property Insights estimates vary from the homes.co.nz ones. (the latter usually being higher, but I haven't checked/compared for a while).

Yesterday’s news ;-P

I actually appreciate interest.co.nz writing a separate article about HPI to give some insightful analysis. HPI definitely deserves a separate full report. It's much better journalism than other MSM medias just writing couple sentences about the same thing in my opinion.

Yes but I think as per my comment yesterday that, if they can’t write about the HPI on the day of release, at least they should allude to HPI.

If there is indeed an embargo on writing about HPI on the day of release, then that seems pretty cynical and pathetic - but maybe there’s a less cynical reason for it? Anyone know?

I actually agree with you, HouseMouse. I also found it's odd that they covered so much of median price but almost ignored more important house price index data. But then I found this shouldn't be a surprise, media being bias is no news these days. My guess would be after many months housing market downturn, media wants to talk up the market, which is reasonable. I think this is why they mainly reported on median price as it goes with their agenda or their vested interest group's agenda.

There's no embargo on the HPI. The table shown above is included in the main media release and both the Property Report (median sales prices) and HPI Report are published on the reinz website at the same time.

Thanks.

so question to this website’s editors - why an article on median prices, and not one on HPI until the following day?

What is the peak to current price decline for these?

I think the peak was more than 3 months ago, so these figures are actually deceptively positive.

Apologies in advance for the formatting, would be nice if Interest supported markdown. Heres a subset of those districts, the month they peaked in the HPI, how many months ago that was and what the fall is from that peak. If you are interested in any particular district let me know, I can add it.

District Peaked Months Ago Fall from Peak

Auckland City 13-Dec-21 7 -15.7%

Christchurch 14-Mar-22 4 -4.2%

Hamilton 13-Dec-21 7 -7.2%

Manukau City 13-Dec-21 7 -15.4%

North Shore City 13-Dec-21 7 -9.7%

Rodney 14-Mar-22 4 -5.4%

Waitakere City 13-Dec-21 7 -13.4%

Wellington City 11-Nov-21 8 -20.1%

Thanks very much for posting! Very informative.

Legend! (even more so if you had to go back through old reports)

"Soft landing"

" ladies & gentleman please ensure your lifejackets are donned before exiting to the wing ... "

Said at 20,000 feet.

Yup. Prices back to 2016. Speculators will continue to hold on waiting for National to role speculation back to high gear. Meanwhile agents will need food stamps.

How dem apples...?

I think that would depend on (a) if there is a brain drain, and (b) what's driven it.

Be a big gamble for National to change settings back to punishing our youth.

Because that's what Luxton and co have been saying they will do. They have shown their cards as clearly pro speculation.

RE lobby, property spruikers talk as if National's comeback in 2023 is a given thing. Dreams founded on wishful thinking. Keep on dreaming.

Money buys elections...those industries will be donating hard out to National/ACT and will be expecting payback.

To go back to 2016 prices would be a good start.

Honestly when you look at the homes.co.nz values in Auckland (almost any area) and take $500K off them they still look overvalued.

Thank goodness the ponzi is unwinding

Re my post above - a family member's sale of a house in Porirua was around $300k lower than homes.conz

Waikato district within Waikato region, please.

District Peaked Months Ago Fall from Peak

Waikato 18-Jan-22 6 -9.9%

When you have a spare moment, Could you take a peek at Dunedin City? Thank you for the constructive discourse!

District Peaked Months Ago Fall from Peak

Dunedin 11-Nov-21 8 -11.7%

So Wellington city the first part of the market to go into crash territory of >20% declines. Looks like many others will follow and I would suggest we are only halfway through the pain of higher interest rates being the main cause of the crash.

Will be increasingly hard to pick the bottom here on out, but -2% for each of the winter/spring months looks like a real possibility. Particularly as it looks like emigration may be picking up. How many people know young people leaving? I know of 2 in my office who are already booking tickets/packing up.

Yep crash has already arrived in Wellington, and is approaching elsewhere.

Tony Alexander’s January forecast of +5% gains in 2022 will go down in history as one of the worst forecasts ever. The guy needs to look himself in the mirror and self critically question himself and the way vested interest has clouded his judgement. And to think I was coming around to him a bit last year.

I've been wondering why Wellington is such an outlier in terms of leading the pace of the crash? Any ideas?

Anything to do with wage freeze's in the public sector possibly? Or it could simply be that Wellington appeared to have one of the most extreme jumps in 2020-2021 when viewing the HPI charts (it was vertical there for a while). The more extreme the price gain, the more extreme the drop.

But trying to rationalise irrational human behaviour is never rational to begin with of course.

Yeah that’s my theory - boomed so much, there will be a larger compensatory correction/crash.

I have been watching closely. My perception, based on anecdotal observation, is Wellington sales are only those heavily discounted. I look at inner-city suburbs such as brooklyn, and there was only one sale last month. However, if you look at rentals they are still high. I look at lower hutt and suspect it will fall further than Wellington City by end of year.

Wellington region has a lot of sales bolstered by large sections prime for subdivision.

Personally I would see bigger medium term discounts in Auckland than Wellington.

Along with a lot of other experts, so many people have taken their advice and will be paying for it for years. Huge amount of people on here warned everyone but were called doom and gloom merchants, the truth sometimes is unpopular but facts are facts anyone could see housing market was in huge bubble.

If he looked in the mirror he would see he has dyed his hair , again. Just not purple this time .

I am sure he looks in the mirror a lot. But not for self reflection.

✈️✅

They are smart cookies. There is a big and beautiful world outside the mental asylum.

Anyone know how many FHB's there were in Wellington last year? Those on a low LVR (10%) will most likely be in negative equity now and those with a 20% LVR approaching negative equity...

We haven't even officially entered into recession yet with rising unemployment....

As I witnessed in the US during the GFC, being in negative equity and losing a job can leave you in a very dark space....keep an eye out for friends/family you know who might find themselves in these circumstances. Its not a great place to be (stress levels = extreme). And hence the warnings over years about the risks of pumping up a housing bubble.

Thanks for posting - great information.

So Wellington is in CRASH Territory

The blood bath has only just started. Look on the bright side, we won't have a labour shortage when we are in a depression, retail is boarded up, cafe's closed. -50% by December.

Whangarei district please. Thanks

Nothing to see here, our resilient market shall see to it that the lemmings jump back on the leverage bandwagon momentarily, TTP told us so!

Never mind rampant inflation, rising cost of living and unending rate hikes.

In Nu Zullund we're difrunt and PrIcEs AlWayS Go uP.

P.S - What an absolute weak play, 50bps? 75 should've been the minimum.

Yes, there are few things more insulting than a Property Broker minimizing the financial carnage they helped create.

I have found one.

TTP said a little while back that the softest part of a Property Broker was his teeth.

I guess these teeth are looking very soft. I am insulted by the look of them.

https://www.stuff.co.nz/business/91418098/property-brokers-manawatu-and…

"Mordaunt said the penalty was "extraordinarily expensive", considering "no-one" suffered financial loss"

Life really sucks when you're arrogant.

He even speaks from experience:

by tothepoint | 16th Apr 18, 5:58pm

I'd sooner have a property than popcorn.

Popcorn will only make you fat and rot your teeth. (Losers spend their money on popcorn.)

Property will secure your livelihood and improve your self esteem. Give me a nice property any day!

TTP

A very weak play, especially as the Fed may be raising theirs by 100 points after their CPI announcement today. I'm thinking the RB are moderating our increases otherwise the sh*t would really hit the fan here.

Thanks Greg. I'd be in favour of you swapping the ordering of your reports on the HPI and the median. To the uninitiated who don't understand the limitations of the medians, the medians are basically misinformation. (Those people take them as indicating the underlying direction of the market).

The first story is most impactful (it gets reposted on Reddit and sometimes the FHB and Investor Facebook groups). I suspect other media players also sometimes are influenced by interest.co stories, and then dumb it down in an even more misinforming way.

Absolutely. Make the HPI the focus - it's not as though the REINZ don't make a song and dance about how its the best available measure - take them at their word! Relegate the median to a foot note on the date - it would be a good point of difference with all the other media on the monthly release day.

I think, at best, most media outlets basically just reprint the REINZ commentary from the press release. At worst, they wilfully misinterpret the data (looking at you Newstalk ZB)

To her credit, Susan Edmunds (Stuff.co.nz) used the REINZ HPI to show peak to trough for the last release (hopefully another article on its way?).

But then this month they followed that article up with this

https://i.stuff.co.nz/business/property/129256802/median-house-prices-i…

Is the full monthly report available at the same time as the REINZ press release? I would hope so, otherwise it's an easy way for REINZ to control how the statistics are going to get reported.

Yes it is. I wouldn't say it's buried on their website, although they tend to only report annual movements of HPI in the press release. It should be taken as given that REINZ is going to spin things: This one's on the media.

100% agree - I was saying this to my friends. I seem to be the only one I know that actually tracks this (the shock on their face when i said Wellington was down 18% since June 2021 they couldn't believe it) and it just makes me think no one actually has any idea how much prices are falling other than people on this website, economists and real estate agents on the ground.

It definately should be the focus as the index is literally the only proper sole measure of house prices in NZ, all the rest are skewed. Especially when you think in a market like this, higher priced homes tend to be sold more as the people buying them usually don't have mortgages and are wealthier so their the transactions being done.

Auckland city a 15.7% drop from peak in 6 months.

Inflation and currency pressures are going to keep the RBNZ from influencing this for 6-9 months more I believe. That would predicate a 30-45% drop from peak to the bottom based on this trend.

Once at the trough I'd like to see a DTI introduced commensurate with prices and wages at that time to prevent another boom bust cycle.

Agreed.

Some people who bought in Auckland City last year may be starting to regret that decision.

Yeah people were paying $2.5-3m for repainted villas in Kingsland.ouch

US Inflation in at over 9%. They will continue to lift rates as well causing our dollar to continue down. If we dont keep lifting rates todays fuel will look downright cheap. So we have another at least another 50bp in August, but should be 100bp.

Soft landing...what a crock.

Be quick...to foop your pants.

The REINZ's House Price Index is probably the most reliable indicator of movements in residential property prices because it is compiled from sales made by REINZ members as they become unconditional, making it very timely, and it adjusts for movements in the composition of sales each month.

Other measures, such as median and average prices are also useful, but they can be affected by movements in the composition of sales each month.

The headline and first sentence of the REINZ press release for the June 2022 statistics, widely re-published yesterday, including here:

For immediate release

REINZ June data: Annual median price increases nationally, but market activity tempered

The New Zealand median price increased 4.2% annually in June, from $816,000 in June 2021 to $850,000 in June 2022.

I fully expect REINZ to do whatever they can to cherry pick statistics that suit them. It's pretty sad to see that echoed across NZ media though.

Exactly. A quick scan of headlines confirms my assumption that media outlets just take the press release and reprint it with little/no analysis.

With the current situation of high interest and the house bubble popping, can anyone tell me how buying a first home makes any financial sense nowadays?

This is my calculation, please correct me if I'm wrong or I missed something. Bear in mind that I tried to be quite moderate in my calculations

You borrow 600K at 6% interest mortgage = - 36K

Devaluation 10K/month X 12 = - 120 K

Maintenance, insurance, rates... = - 10K

Loss of return in your term deposit for 200K = - 8K

Equals----------------------------------------------- = -174K

Rent Payment 650/week = +34K

TOTAL LOSS FOR THE YEAR = -140K

Some big assumptions there regarding values and based on short term thinking...

Most people buy a house for a place to live long term rather than seeking a short term return...

"Most people buy a house for a place to live long term rather than seeking a short term return..."

....not lately they haven't. This is why we're in this mess to start with. Why have Brightline for starters? There will be many "Accidental Landlords" out there not to mention those who have no choice but to backpedal their faltering investment strategy to their friends "yes we bought it as a long term investment"

Joaquin specifically mentions he is talking about whether buying makes financial sense. He is not talking about people buying houses for other reasons, such as to live in (which seems to have been a subordinate reason for buying a property in NZ lately).

It definitely doesn’t make financial sense.

Rental outgoings for equivalent properties are much lower than mortgage payment, and house prices have some way to fall.

Unless a bargain can be snapped up - ie. at least 25% lower than peak value - then for many FHBs it will make much more financial sense to wait perhaps one more year.

by then their KiwiSaver balance would have shot up ( assuming cash fund), prices will be much lower, and interest rates will be heading downwards.

How would you identify how much a house is down from peak value, HM? I'm trying to base it on CV to get a rough estimate of fair price in this falling market.

Seems to me that Auckland houses are selling around their Jun 2021 CV at the moment, which is down about 12-13% from peak?

I'm eyeing the 2017 CVs for Auckland now, which is about 30% down from peak, I think. I'm noticing that the best deals in East Auckland (which is where I'm tracking sales) are selling at about 10% above the 2017 CV. Note that Auckland prices were mostly stagnant between 2016 and 2019, so going back to 2019 vs 2016 is more or less the same thing.

Yeah maybe 2017 CV as a general proxy for a great deal, Tui

Thanks, HM.

My partner and I are both professionals earning good money, but we've been raising our kids in a tiny, tired 2-bed rental in Auckland while saving every extra cent for a house deposit. Last year, we 'missed out' at an auction on a tiny, tired little 3-bed place, but here's hoping we'll be able to afford an actual house in the next few months. My kids are middle-school age already and too many of their childhood memories will be of growing up in this grotty little rental.

Your kids are lucky to have you. Good luck.

That is so sweet of you - thanks, Mountie. I could add that we have been filling our little rental to the brim with fun times, bedtime stories and love. You don't need a big house for that.

Great work. In the current environment though we have NOT hit the bottom, if you can hold out for another 6 months, that's 6 more months of savings while properties are probably going to get a lot cheaper over that time. Bide your time, if you are able to.

We grew up in some shitty houses during our childhoods. You don't really remember how small stuff is or anything, you do remember the shared family good times. IMO the smaller the house, the better the memory, from experience! We moved to a bigger house and everyone talked to each other a lot less and spent more time in their rooms, not exactly a conducive family environment. I have fonder memories of the smaller houses than the bigger ones.

Wise words, blobbles. Thanks for the encouragement.

And thanks for sharing your childhood experience. I think you're spot on. I grew up in a big house full of rooms and corners where we could hide from, and avoid each other. On the other hand, my kids are closer than I could ever have hoped for.

Hi Nifty, I completely agree with you, we have never thought about a house as an investment but a place to live, and the simple idea of talking about this human right as a financial decision is obscene. However, we were thinking about buying but after making some numbers I realised that it's not a good idea for us to lose all this money that we worked so hard to make.

it's not a good idea for us to lose all this money that we worked so hard to make.

What are you losing if you buy? House prices may drop in the short term but long term they may increase. If you don't sell, you don't lose anything. Same principal applied last year, people felt wealthy when their properties were increasing in value but they actually weren't any better off if they didn't sell.

There's never a good time to buy for most interest.co.nz commentators, just keep that in mind.

"If you don't sell, you don't lose anything"

Are you sure?

Would you rather have a $600,000 mortgage, or a $300,000 mortgage? (to buy the same house).

Imagine the additional spending capacity and quality of life you would have if your mortgage was half the size at the outset of its 30 year term.

This is what we could be facing....that people who purchased in 2020-2021 could have mortgages 20, 30, 40, 50....% larger than those who buy a few years later and will have to navigate the same mortgage market/interest rates over the term of the mortgage.

Just keep that in mind. These aren't inconsequential issues when viewed over the long term...and are a result of crazy market fluctuations (.e.g prices going up 40% in 1-2 years and could potentially drop by the same in subsequent years). Could be the difference between being mortgage free at 50 vs mortgage free at 65.

Exactly. Well put.

a house price decline of 10% is neither here nor there.

However a decline of 25-30% is a very different story.

Is it going to happen though... equally could prices increase in the next 3-5 years? It's always a risk, it's easy to paralyze yourself by thinking about worst case scenarios and never moving forward with life.

On the law of probability I would suggest there’s a good chance of further 10-15% falls. And very little chance that prices will rise.

Very little chance prices will rise... in what time frame...

Over the next year of course, as I have been talking about that timeframe above in terms of FHBs.

Ever tried to move house if you owe the bank $600k and your house is worth $500k?

Nah, have you?

Not personally, but the Irish experience is pretty well understood. Around 314,000 mortgages were underwater which massively restricted mobility, so Ireland had big problems with people being unable to relocate for work.

https://www.independent.ie/business/personal-finance/property-mortgages…

Nifty,out of interest,what is your position?

Owner occupier,renter,investor...always nice to have some context.

He is definitely not a first home buyer, that is very obvious!

Is there any context to people giving advice here? I'm just providing an alternative view on matters rather than the straight DGM stance you often see here...

Man, "DGM" again? Now I am seeing people are using "DGM" more as an excuse to avoid some factual based discussion... All you need to do is to call someone DGM and you think you are on the high ground... But actually you are not...

Was going to call this out too. I don't see DGM here so much anymore, just an increasing consensus that the market is crashing backed up by actual evidence in the form of HPI data.

Yeah I thought Nifty was better than that

Lol better than that...

The comments section is flooded with unfounded predictions of 40%-50% house price drops, housing very soon being affordable again & advice to lock your funds away in term deposits.

As soon as there's a view that's slightly outside of this, it's shot down.

If you look back at the comments section you'll see the trend that interest.co.nz commenters dwell in doom & love it...

Balance is key, especially if you want to take advantage of opportunities that you might be blinded to if you think the sky is falling...

Clearly, misery likes company.

So what constitutes a DGM? Flip it around the other way - never ending house prices gains is 'doom and gloom' for prospective FHBs. For FHBs, property spruikers are DGMs.

It's a lazy, cheap and kind of insulting term.

And who is a DGM?

Am I a DGM for predicting peak to trough falls of 15-20%? (they will probably be more than that, perhaps 25-30%) Or is that not gloomy enough? I've been called a DGM many times on this website.

I don't think that it is at all likely that prices will fall 40-50%. But it's not impossible and people are entitled to that view.

And even if I don't think it's especially credible, at least it's a nice change from the near universal spruiking of house prices that one encounters almost everywhere.

It's good to have different opinions and I usually value yours, it's just a pity you've landed in the gutter by using the term 'DGM'.

I'd say you've got more balanced views than most here at the moment.

Not sure how DGM would be offensive but yeah, my prior comment explains what I'm seeing here and I use DGM lightly...

Nifty

What is happening was totally predictable - anyone not vested and impartial could see it coming years ago.

Sadly, as Kiwis we’re not the sharpest lot… we have a pretty poor education system and it’s only getting worse. We’re also lazy as a whole compared to other cultures.

So it was fairly easy to con the masses with a get rich quick scheme. Those that were vested have had a field day with the sheeple.

Guys like Tony A, Ashley Church totally cleaned up. Constantly paid to preach residential property as bulletproof etc. Property can’t crash, we’re different etc. Everyone wants to wheel them in to hear it from an ‘authority on the market’.

It will likely all come out in some sort of Royal Commission in a few years. It will be the easiest thing for a Govt to do. Ask how it all went so wrong.

When the answer always comes down to too much debt concentration. Same problem, different generation, different market.

Have you ever asked yourself this simple question - why do all the richest people not have all their money in residential property?

Because they’re not stupid. But you’ll find plenty of kiwis who are.

Sadly, most just want a home to raise a family. They are the ones that don’t deserve the pain.

The clowns and charlatans screeching about the "DGMs" and "doom goblins" last year have all but disappeared from this site.

It's very sad, but entirely predictable, the lot of them were a bunch of has-beens and dropkicks.

The "doom goblins" were actually right on the money.

If you check the final page of the report, you'll see a number of the results are moving averages of up to 6 months -> which indicates to me 1) those areas have had very few sales, and 2) the reported value is 3 months old, even for them.

Hopefully the huge amount of people on this website who did not see crash coming will now understand house prices are hugely over valued and need to come back down to a place where average wage couples can afford a house, with rates and inflation climbing and NZD tanking anyone who purchased in last couple of years will soon see deposit gone and be in negative equity over coming year. Sometimes it’s better to sell at a loss than lose it all, plenty of people made money on way up only to reinvest into more expensive house you’re profits are now disappearing quickly this downturn is here to stay and will stop speculators from playing in housing market.

I think you really should lead with the HPI rather than the median sales prices as per yesterday. I know the hoi poloi only see $ signs, and index movements are abstract, but if you'd only read yesterday article, you'd have a false sense of the market and I've already heard it parroted elsewhere that the market has stabilised.

Even REINZ's press release headline "Annual median price increases nationally, but market activity tempered" was grossly misleading.

What's actually happening to medians, in my observations, are that luxury properties are still selling, especially north of Auckland, but low value has fallen off a cliff (apart from Papakura which is the only place still affordable for FHBs and investors with rising interest rates).

Clearly that's only Auckland, but as they have the lions share of sales, it will impact across the whole country.

Hamilton. Slight gain last month and 1.9 last 12 months. I'll take that.

Nice steady downwards trajectory on the graph, just like most places. Page 7.

https://www.reinz.co.nz/Media/Default/Monthly%20Press%20Release%20Asset…

Edit: except Wellington City which is apparently in freefall.

Actually Hamilton is doing well comparatively. Median rose MoM and YoY, not many areas achieved that. So it is good in the Tron

It won’t be soon. The Tron isn’t immune to this.

Oh shush. Hamiltron house prices are on par with London because Hamiltr0n is the city of the future. Or whatever the **** its going to be called after year zero.... echo "gravel sandpit" | google translate

I have tried to give it the benefit of the doubt a few times but…. It’s godawful

HM I know you adore the hole at the bottom of the NI, some say the capital should be moved to Hamilton. If it wasnt for the capital why would anyone choose to live in Wellington? Hamilton from a natural perspective has got to be the safest city in the country. Volcanoes no, tsunamis no, floods no, earthquakes lowish risk.

Nah I reckon somewhere in Wairarapa should be the new capital, maybe Masterton. Pick up the Beehive and tow it over the Remutaka hill, should be fun.

From a truly selfish point of view I would like to see it fall in line with the other regions. It would be good to understand how/why the Waikato is still holding up fairly well in comparison, lots of Waikato houses on trade me are now being priced under the 2021 issued CV.

Hamilton economic growth is above average. There is a Stuff article if you wish to Google

What are its areas of strength, and how vulnerable are they?

I would say for starters, cheap housing and compact city

I meant in terms of industries. House construction has been booming right? That will likely slump

DYOR HM

DMOR? Can't you provide a quick answer as a Hamiltonian?

Oh well, I just looked and it seems to be healthcare, manufacturing and .......housing construction. If the latter plummets, as it is likely to, that will be quire painful for Hamilton.

I also note by current NZ standards Hamilton has quite high unemployment at 4.8%.

Construction has been massive in Hamilton and for the past 3-4 years, houses on large sections have been removed and replaced by lots of proxy town houses. Surrounding towns like morrinsville, Taupiri and Ngaruawahia booming with construction. I really do wonder if we have enough households to fill all the houses constructed in the past few years. The Tron is a great place to live, don’t tell any one last thing we need is more people heading here and buying houses. probably considered centre of the mighty Dairy Industry too.

What’s great about it?

I don't have the stats to prove it, but if we follow the post-covid trend in the US (https://www.economist.com/interactive/graphic-detail/2022/04/30/america…), then the Waikato may be benefiting from remote white collar workers spreading out from Auckland.

Auckland is down about 13.2% from peak.

Good article with some good explanation 😀Wellington is in crash territory, Auckland not quite yet.

Next quarter Auckland will hit crash territory. Higher rates and inflation just starting to take hold and with NZD tanking inflation will stay high for a while.

NZD falling also helps our exporters as prices for meat timber diary fall, and are based in USD not NZD, two edged sword....

Summary, the "boom" during Covid is being rolled back and then some. As it should. It was completely artificial and founded purely on record low debt and nothing else.

I'm by no means a conspiracy theorist, but I find it awfully suspicious that REINZ (I presume) only allows reporting of the median report on the day of release. Yesterday we saw the Herald and Stuff both run stories around the increase in the median.. and today.. nothing. Then, if they do turn around and actually cover the HPI, the average punter is left confused and thinking - but they told us it was going up yesterday?

The RE industry and MSM are in bed together.

I thought it was very telling that I never got a response from the Herald, despite multiple follow ups.

I thought about taking that to the press council, but decided I wouldn’t waste my time as apparently all they can do is slap the Herald over the hand with a wet bus ticket…

Better just to accept that objective reporting in the MSM has been totally corrupted.

I will cancel my Premium subscription out of principle (if I miss a few good articles a week - only a few - so be it)

I'm by no means a conspiracy theorist, but I find it awfully suspicious that REINZ (I presume) only allows reporting of the median report on the day of release.

There's no embargo on reporting on the HPI. All the data is available at the same time, but most media outlets just cut and paste much of the press release provided (which are written specifically for that purpose, even down to the quotes of the spokesperson.

Investors are starting to lose money then. And as sales were going down a year earlier, less tickets can be clipped (phrase borrowed).

I must say that given these house prices trends, the economy and employment is fairly resilient.

I would remain very surprised if it remains so, what do people think is going on here?

I am assuming lag effect at this stage.

does anyone know how much lag effect there was in Ireland between the start of the house price collapse and unemployment rising?

Its a bit like musical chairs....the music has stopped, so people are looking for a chair, but they don't realise yet that there aren't enough (chairs) to go around. So they're just looking around for a chair in an orderly manner.

The panic starts when people realise what is happening (not enough chairs and some people will miss out)....but that tipping point hasn't been reached yet. I think if we start to see rising unemployment later this year (with inflation still above mandated levels) then panic could set in. Its a snowball effect - at least that is what I experienced in the US during the GFC...the change in sentiment starts small but it grows bigger and bigger to the point that it becomes a whole new narrative that is unstoppable..

Agreed the failure to keep everything ticking over as normal will now result in huge fluctuations and overreacting. Panic is looking more and more likely by the day.

Probably also a bit of ‘fat’ in employment given how big the shortages have been in many areas.

There was a piece last week on Interest that job adverts saw the ‘first non trivial fall’ since Covid delta. Mostly due to falls in property related services. Will be interesting to see if sector specific high unemployment can have an affect. Obviously there are huge shortages in medical and tech areas but they are fields that you can’t necessarily easily transfer into.

I subscribe to WSJ & have noticed in the last month or so that there's a lot more employment type stories appearing - both of the shortage of good labour available (for some 12 months or more) & of companies not hiring or planning to hire. So from my reading, that means they (USA) are right on the tipping point right now. We won't be far behind.

Agree. I think many firms will still be wanting to hire top talent, it will be quality over quantity For now.

True but also more ammo for the RBNZ to keep raising rates...'see unemployment isn't rising'.

Yep agree.

If there’s no major impacts on employment, then that’s one reason to keep hiking.

At what point do risks to financial stability from large house price declines start to affect decisions on the OCR?

we have been led to believe that stability will not be badly affected by falls of 20%, but maybe if they hit 30% it’s a different story?

"At what point do risks to financial stability from large house price declines start to affect decisions on the OCR?"

View this in reverse....did the RBNZ care that house prices were going up 30% p.a. when they dropped rates? No they said that house prices aren't their mandate.

So I can see a scenario later this year or early 2023 where house prices are down 30% but inflation is still in the 5-10% range and unemployment still isn't an issue, and the RBNZ will say 'inflation is our mandate, not house prices'. So they keep raising rates.

How the economy responds to such a drop in house prices is hard to say...as you point out its been pretty resilient so far, which could actually be even worse for house prices going forward because inflation isn't dropping yet, nor is unemployment rising.

Ah, we have arrived at a really interesting contrarian point IO! That unemployment, by staying low, may actually be bad for house prices, as it will provide more scope for OCR hikes!

That totally turns on a head the economists’ narrative that house prices won’t fall that much if unemployment stays low.

Nice!!!

Yes there are some very different economic factors playing out at present:

- boomers retiring leaving gaps in the workforce

- younger people leaving the country

- limited new migrants/international students

- massive expansion in money supply/debt in the previous 2 years.

- lots of jobs

- persistent inflation

Given these factors, we may have to have a very severe recession to start seeing a bit dent in the unemployment rate (because the demand to be in NZ and work in NZ isn't the same as it has been in the past....think a crashing 'rock star economy' that everyone wanted to be apart of might now be dead...akin to what happened to the celtic tiger when the party ended). If we had lots of people wanting to com here and work here then you could see downward forces on wage inflation and employment...but that isn't the case (at least how I see it for now).....of course this could change if the world flips into a severe deflationary recession...but we will have to completely crush demand to do that....and that would require a 1929 style event.

It might not be as clear cut as that. It looks like unemployment was a bigger factor in defaults than declining equity, and defaults were a major factor in declining house prices.

Changes in unemployment rates are found to have a stronger influence on default probabilities compared to house price movements - showing ability to pay considerations have a stronger influence than house equity for delinquency rates

https://www.dnb.nl/media/chtlufcw/robert-20kelly-20-20final-20version_tcm47-279034.pdf

Huge lag I would say and that's the problem there are huge lags all over the place. We should have never let it get in this mess to start with its now almost impossible to control.

You're starting to sound like me...but just 5 years late. Hence my desire to try and avoid/prevent these circumstances from developing when we had the opportunity to do so....but being ridiculed by those with vested financial interests to make a personal gain from the circumstances.

To be fair it was ticking along fine until COVID arrived. I predicted a bit of a property crash then and had the RBNZ not stepped in with free cash and a complete overreaction we wouldn't be here now.

"To be fair it was ticking along fine until COVID arrived"

Asset bubbles always are....until they aren't.

And yes without the extraordinary market intervention back in 2020...the price declines we are seeing now, we would have witnessed in 2020-2021.

Question is...will we see extraordinary market intervention again next year? And create more of the inflation problems we already have as a result? (because they only solution they have is to devalue money even more....)

I.e. the current solution to the problem is to make the problem even worse! (does that not sound insane to you?)

@HM...might be good that the immigration flood gates are not being opened yet,even though the business community is calling for it.

I think we are overdue for the bank economists to update their house price declines guesses.

They know it's bad, but cannot be completely honest from the outset otherwise they will spook the horses.

It's like during the start of Covid then the government announced that the borders will be closed for 2 weeks, then another review said 2 months, but all along they knew it was gonna be at least 2 years.

So they are dishonest rather than incompetent?

They may be trying to offload their portfolios quietly,whilst spruiking the market to everyone else...

Zollner tweeted yesterday...but just indicating that house prices are going negative (annual basis).

https://pbs.twimg.com/media/FXf3OWcaMAABAH4?format=png&name=small

She’s the best of a bad lot, but that’s not saying much.

They're gonna need a bigger chart.

Well, housing market is a zero-sum game, someone loses out will be someone's gains! But with interest rate is heading north, the joy party is getting thinner!

The house price falls have significant differences in locations with annual HPI comparison for Wellington as -18.1% fall compared to Christchurch as 15.1% rise. If both were both to fall a further 5% with Wellington -23.1% and Christchurch 10.1%. One NZ city is crashing while the other has still experienced significant growth. Unsure if we have had these significant differences with past declining/bust property markets in NZ.

Early days yet. Ireland's crash took 3 years to play out.

Does anyone know if there is same-house sales data available for NZ? ie:

“25a Beach St, Napier just sold for $1m. It last sold for $800k 5 years ago, representing an annualised gain of 4.4%”

Like Same-Store Sales data for retail.. I feel that would be a helpful addition to house sales data.

There is, but it's held by groups like REINZ & CoreLogic and not published for consumption by the great unwashed. You can track this data yourself with the use of things like homes.co.nz which does report some sales prices. The REINZ HPI is pretty much the closest thing available to what you want, the way it's calculated means it will be quite close to a same-house sales dataset but aggregated at a district level.

There is a subscription database service that provides this and many other cool features.... its around 1k a month tho.....

What crash, new houses are still being listed as auctions in Christchurch….Don’t think the buyers/FHB there are reading the news

Getting very excited about buying everything at the bottom. #specuvestor

Bitcoin and Ethereum are at the bottom - knock yourself out in buying!

Which bottom?

Anyone else concerned with bank stability?

Yeah. Deposit Takers Act isn't coming into force until 2023 either.

Apparently the banks are absolutely fine with a 40% drop and can likely survive a 60% drop, according to RBNZ stress tests, without any RBNZ intervention.

But those stress tests are run by the RBNZ and their record when imagining future scenarios is not exactly brilliant.

Honestly, I'm pretty concerned about this too, but where exactly is safe?

Buy a big angry dog or two and get a shotgun licence. Draw down all your money in cash and hide it inside an internal wall of the house, away from the damp bathroom. Remember not to tell anyone . There's normally enough room to stuff it in between the framing nogs behind a power plug socket and you can reach in with your hand. :)

Lol! Let’s not forget 7 yr supply of cans of spaghetti and baked beans. If I buy now, I can get ahead of inflation at the same time. Win-win!

Can someone please take a 10 year HPI and put a trend line through it to see where the the HPI would be without Labour's $$ lolly scramble lining the pockets of every man and his dog to put into property from October 2020. I have a suspicion that we are simply getting back to where we would have been on the long term graphs, given that pre covid things were slowing down anyway. My prediction is a leveling off in Sept of HPI around 3400 and while this does equate to a short term fall, it is the market getting back to normality after a very abnormal few years coupled with poor decision making from the top.

I know we love to predict a crash apologies for the rationality...

RBNZ sole mandate now is to tame inflation.

They wont care about people struggling to pay mortgages.

It will be slow and painful as the cloud of uncertainty hangs everywhere.

Wage induced inflation wont last as businesses bail out.

Disagree watch the OCR rises stop at 3.5 to 4% regardless.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.