Here's my Top 10 items from around the Internet over the last week or so. As always, we welcome your additions in the comments below or via email to bernard.hickey@interest.co.nz.

See all previous Top 10s here.

My must read is #1 on the topic of good deflation and bad deflation.

1. Good deflation or bad deflation? - New Zealand is rapidly being dragged into a global debate about deflation.

Yesterday's CPI figures showed prices fell in the December quarter and annual inflation is headed for a negative number in the March quarter.

This is well below the Reserve Bank's 1-3% target band and raises questions about whether the Reserve Bank has run monetary policy too tight and should cut the Official Cash Rate.

It all boils down to a debate over whether this deflation is structural, and whether it is 'good' deflation or 'bad' deflation.

The 'good' stuff is driven by some type of structural change that is increasing productivity and real wages. Some argue that central banks should let this stuff go through to the keeper because it's not the 'bad' inflation caused by a lack of demand.

I read The Second Machine Age over the summer, which makes a persuasive argument that the latest waves of computing technology are generating the same sort of productivity and growth surge as the invention of the steam engine in the late 1700s. That unleashed a period of very low inflation and occasional deflation.

I think there are some deeply structural elements to the waves of deflation now racing around the globe, both because of new technology and ageing populations.

Should that encourage central banks to cut interest rates to zero and start printing money to stave off deflation? The US, Japan and Europe chose that path and it has generated enormous asset price inflation deflation.

Our Reserve Bank is no doubt thinking about these same issues. Up until now it has been able to avoid it because our inflation has been high enough not to worry. That grace period may be ending and the Reserve Bank will face some tough decisions.

Does it cut interest rates to keep within its 1-3% target band for inflation and risk pouring more rocket fuel onto the Auckland property market fire? Or does it use Macro-Prudential tools in conjunction with rate cuts to try to limit the damage? Graeme Wheeler said in December he wasn't looking at more Macro-Pru. I wonder how long that will last.

Here's a useful discussion via Ambrose Evans Pritchard of this same issue in Europe, where it looks like the European Central Bank will tonight announce plans for more than 1 trillion euro of money printing. There is less doubt in Europe that they have plenty of 'bad' deflation caused by a lack of demand and high unemployment, but no doubt a lot of the same structural issues are underneath the problem.

Pritchard quotes William White, the economist from the BIS that predicted the 2008 crisis, on the dangers of the ECB's QE plan.

"Sovereign bond yields haven't been so low since the 'Black Plague': how much more bang can you get for your buck?" he told The Telegraph before the World Economic Forum in Davos.

"QE is not going to help at all. Europe has far greater reliance than the US on small and medium-sized companies (SMEs) and they get their money from banks, not from the bond market," he said.

"Even after the stress tests the banks are still in 'hunkering down mode'. They are not lending to small firms for a variety of reasons. The interest rate differential is still going up," he said.

2. 'Let nature take its course' - White is in the camp that says central banks should let the 'good' deflation take its course. He might need to read a little Dickens to get a sense of how those periods of deflation and occasional Depression in the late 1800s weren't a lot of fun for everyone. Those deep Depressions and the resulting social stresses helped cause a few ructions in the early 1900s...

Here's White:

He deplores the rush to QE as an "unthinking fashion". Those who argue that the US and the UK are growing faster than Europe because they carried out QE early are confusing "correlation with causality". The Anglo-Saxon pioneers have yet to pay the price. "It ain't over until the fat lady sings. There are serious side-effects building up and we don't know what will happen when they try to reverse what they have done."

The painful irony is that central banks may have brought about exactly what they most feared by trying to keep growth buoyant at all costs, he argues, and not allowing productivity gains to drive down prices gently as occurred in episodes of the 19th century. "They have created so much debt that they may have turned a good deflation into a bad deflation after all."

3. Dodgy figures? - There was a lot of excitement this week about China's GDP growth rate falling to a 24 year low of 7.3% in 2014, but there remain many doubts about how legitimate that figure is, and other economic statistics in China.

Jamil Anderlini has a look at China's unemployment rate, which has remained remarkably stable between 4.0 and 4.3% for the past five years. It seems there are 'internal' numbers that are different and China may be more sanguine about the risks of unemployment than it should be.

The Economist Intelligence Unit released a report last week, based on research conducted with the IMF and the International Labour Organization, in which it estimated China’s real unemployment rate in 2014 was actually 6.3 per cent.

That was higher than both the UK, which the EIU estimated had an unemployment rate last year of 6 per cent, and the US, at 6.2 per cent.

The picture is complicated further by the 274m rural migrant workers who power China’s economy but are almost entirely ignored by unemployment statistics.

When most migrant workers lose their jobs they return to their homes in the countryside.

4. Not so fast - Derek Scissors writes here in an FT blog that China's growth rate is not nearly as fast as the official figures suggest. He looks at money supply.

There is an indicator both revealing as to the accuracy of headline GDP growth and the extent of the economic challenge facing Beijing: money supply. Broad money M2 breached $20tn at the end of December, a staggering 70 per cent larger than in the US, where monetary policy has hardly been tight.

There’s a tremendous amount of liquidity, the problem is no one is using it. Growth in narrow money M1 has collapsed. It was a dangerously excessive 32.4 per cent in 2009. It was a dangerously anemic 3.2 per cent in 2014.

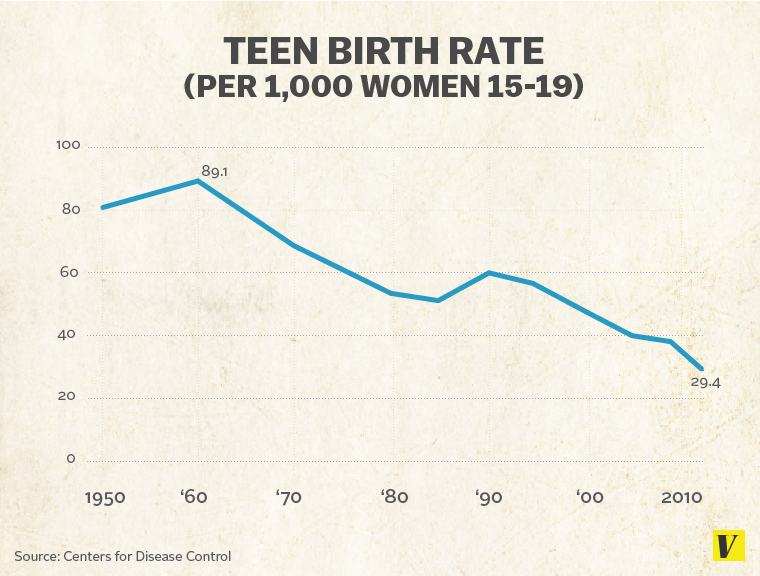

5. Why are teen pregnancy rates falling so fast? - The National Government has trumpeted a sharp fall in the last couple of years in the number of young mums on the DPB. It has claimed credit because of benefit reforms, but there may be a few other things going on.

Something strange is happening to teenage pregnancy rates all over the world. They're dropping sharply. This is great news in many ways, but it's a mystery.

The most interesting theory is that the MTV reality TV sensations, 16 and Pregnant and Teen Mom, have had an impact. I've watched the programme with my wife (who can't help herself and I have to admit I found them fascinating) and I can see why it works so well. If the Government is keen on its investment-led approach it could pay for a New Zealand version of the programme to air on prime time. Just a thought.

One piece of research suggests the two TV shows were responsible for a third of the drop in the teen pregnancy rate. And then there's a drop in lead levels in teenagers. No one is really sure.

Vox has a look at the issue here:

Levine and Kearney began looking at changes in the teen birth rate in places where the MTV shows had high Nielsen ratings — and those where it didn't do well at all. And what they saw was areas of the country with high Teen Mom viewership had significantly faster declines in their teen birth rates. They published their first results last year, in a working paper titled "Media Influences on Social Outcomes: The Impact of MTV's 16 and Pregnant on Teen Childbearing."

6. Focus on the Middle Class -I wonder if Larry Summers had a chance for a chat with John Key at Davos about the need to bolster the developed world's middle classes.

Here's what he might have said (via an Op-Ed):

If it is to benefit the middle class, prosperity must be inclusive and in the current environment this is far from assured. If the US had the same income distribution it had in 1979, the bottom 80 per cent of the population would have $1tn — or $11,000 per family — more. The top 1 per cent $1tn — or $750,000 — less. There is little prospect for maintaining international integration and co-operation if it continues to be seen as leading to local disintegration while benefiting a mobile global elite.

The focus of international co-operative efforts in the economic sphere must shift. Considerable progress has been made in trade and investment. Less progress has been made in preventing races to the bottom, in areas such as taxation and regulation. Only with enhanced international co-operation will the maintenance of progressive taxation and adequate regulatory protection be possible. And only if ordinary citizens see benefit in an ever more open global economy will it come about.

These three concerns — secular stagnation and deflation, slow underlying economic growth and rising inequality — are real. But they are no grounds for fatalism.

The experience of many countries and many eras shows that sustained growth in middle class living standards is attainable. But it requires elites to recognise its importance and commit themselves to its achievement. That must be the focus of this year’s Davos

7. Negative yield curves - David Chaston put out a very useful piece a few days ago asking if New Zealand's bond yield curve was about to go into 'inversion', where it is cheaper to borrow long term than short term. It's the natural consequence of money printing overseas flowing its way down here and pushing our bond yields down at the same time as the Reserve Bank is holding our short term rates relatively high.

We've been here before. Back in the 2004-07 period our Reserve Bank lost control of monetary policy to an extent because cheap foreign money drove down fixed mortgage rates to well below floating rates.

We're headed back there pretty quickly.

Here's TD Securities with a useful chart.

8. Inflationary expectations - Yesterday's inflation figures also showed that inflation is dead outside of Government and the electricity industry. Yet still the inflation comes down from on high in places where poor consumers have no choice but to take it.

Here's MPI with a 16% increase in fees and charges. Somehow this Government had the gall to accuse the Opposition of proposing three new taxes in the election. Shortly after the election it announced a pseudo tax increase. It has done this before with all sorts of fees and charges. The higher petrol taxes for road spending was just one example.

9. Fresh money and fools - This is a cracker from Manny Roman about freshly printed money and asset price inflation.

A few months ago in New York, a private collector handed over a small fortune to buy a white canvas on which four letters had been stencilled in black ink: FOOL. The painting, by an American artist named Christopher Wool, had changed hands three years ago for $8m. Its new owner paid nearly twice as much.

Prices have been rising in other markets, too, in large part due to quantitative easing. This tool for central bankers was forged in the aftermath of the financial crisis, and involves buying assets with newly created money.

10. Totally John Oliver on New Year's celebrations. I sympathise.

(Updated to correct inflation/deflation in number 1)

49 Comments

Interesting discussion on deflation.

It may be too late now for the RBNZ to make much difference. They have kept the tightening on too long since the GFC and deliberately ignored the deflation risk.

I dunno. I'm just not sure what "deflation risk" means? If it means the world plunges into another Great Depression - then for starters, banks start calling in mortgages, can't recover their losses and default - but Wheeler's got that sussed with the OBR and existing savings/savers bearing the brunt of that deflation effect.

So following on from that, we need a government in the position to be able to provide emergency support to a rising unemployed public which will be faced with rapidly rising prices for basic necessities - and a government able to keep schools and hospitals open and law and order functioning. Meaning, a government able to continue to borrow during what is likely to be a period of international capital volatility/flight.

Would that not suggest that to pre-position NZ for such a Great Depression event, that raising the OCR (thus increasing the incentive for more local savings/deposits) and providing a greater degree of wiggle room to fight the inevitable rampant inflationary effect on basic commodities be the way to go?

That is, of course, if one still believes that central banks generally still have some kind of hold/influence in managing such events.

Got to wonder when the tradeables sector has been so bad for so long just what the hell is going on in the Govn's mind. Or maybe the answer is simple, it is an empty mind with nothing going on but an eye to continuing to keep the income stream from the SOE's coming.

Pity that the voter has not and probably will not hold them to account.

"pre-position NZ" oh god no, a huge no.

If you accept the premise that the way the global economy is set up is it has to grow and being on a finite planet cannto for ever then the Q is when you cannot grow any more, what happens next?

Im not sure what good calling in mortgages will do, also I dont think that is the order of events. If nothing else once a bank starts doing this en-mass the political fallout will be so severe that the Govn will nationalise them, it will have no choice on the matter IMHO.

I also think that the OBR event will happen before mortgages are called in. The reason the OBR event will occur is that house prices (and / or farms) will have dropped so much in value (like 30%+) that the banks are technically insolvent as thier assets are worth so much less and they cannot get additional external funding to cover that loss. Then we see the OBR take place and then we see the receiver calling in mortgages, or more likely selling them to other banks.

?

"rising unemployed public" yes I expect so.

"rising prices for basic necessities" not so sure as the defination of deflation is dropping prices. I think we will see a mixed message, overall deflation but sure some things costing more or also likely not available as its priced out of what people can or are willing to pay.

"a government able to keep schools and hospitals open and law and order functioning"

We can look at similar events overseas for this, Russia and Cuba spring to mind.

"borrowing" um no no one will be lending, or doing so at a rate we can afford ie > 7%.

"huge no" frankly based on what has happened overseas to such a rise is it caused the very mess we seek to avoid. We wont have inflation we can control is the simple answer, or not without killing the patient.

The savings rate as far as I can determine bears no relationship to amount saved as far as I can see. Lets say it does, well the money taken out of the economy and put into savings contracts teh economy causing said recesion/depresion, bad idea. The second whammy is businesses see it as to expensive to borrow to expand and may even contract and pay down debt costing jobs.

"inevitable" no I dont agree.

Change of subject slightly but you, or some other reader may know the answer to this.

In the event of the OBR provisions requiring a portion of savings deposits being frozen, who owns the bank. From what I have read this morning the shareholders investment is exhausted at that point. It is not stated anywhere but to me it seems only fair that if the government is taking the depositors money to keep the bank running then this is the equivalent of an injection of cash from an investor. Accordingly the depositors should become owners of the bank. Is this the case, and if not what happens?

The other related question is; does the NZ arm of the Australian banks become seperated from the Australian parent in the event of an OBR event? If not how is the whole mess untanggled if with respect to NZ depositors if the Australian banks go into distress?

The depositors' money are not used "to keep the bank running" - the "haircut" accounts for losses that would have already occurred. This is the same as if the bank was being liquidated: i.e., the depositors may receive only part of their funds (deposits minus the losses).

A cash investment, that would be required to keep the bank functioning, will come from elsewhere (a private source or/and the Government, who then become the new owners).

As to the Australian subsidiary – related question, the NZ banks are separate legal entities and therefore the parent banks do not carry financial liabilities. Having said that, the OBR does create a bit of an incentive for the parent bank to come to the rescue, both financially and from brand reputation viewpoint.

Thanks Alex. That is corrupt. The big money boys are well and truely looking after each other. It should belong to the people whose money was stolen to pay for the profligate lending to the gambling speculators. It will be interesting to see how much money is invested by the banks new owners compared to the theft from the depositors, how much the bad debts are over inflated and how much of that bad debt is eventually recovered.

Perhaps it is timely to recall the history of the sale of the Rural Bank. As I recall them the details are:-

The turmoil of 1987 resulted in the removal of a lot of subsidies to farmers. This impacted on farm values and accordingly the bad debt provisions of the government owned Rural Bank.

A young female auditor was tasked with signing off the audit of the banks accounts. She refused to do this because it was her belief that the the bad debt provisions were far too high. She was crucified in the media by the authorities but still she refused to sign them off. Eventually somebody else signed them off and presumably her future employment in the position was not healthy.

Soon after this, the bank was sold to the banking arm of Fletcher Challenge for a hand full of dollars. The reason being that the bad debt provisions were so high that the value of the company was minimal. After a few years the new owners revised these bad debt provisions to more realistic levels and to reflect the the fact that the farmers were not as badly effected as first feared. A while later the bank was then sold to one of the main banks (National I think) for a high number of $100's of Millions (Nearer $1 billion I think but I can't be certain)

What does that all add up to and what does it tell us about what could happen if our present banks get into trouble?

Given that the depositors will have had part of their deposits stolen then then they should be given the first option to buy all the shares of the bank, not just some token fob off. No body else has a greater or indeed any moral claim.

Once the OBR has taken place all deposits in the bank are then Guaranteed. As long are you are not in the first bank that goes into OBR, you should have time to move your deposits to the OBR bank and get a government guarantee.

Keep away from banks with high LDR, like the BNZ and you should be Ok.

Why are they guaranteed? there is no loss left to cover, yes...ergo you shouldnt lose any more, for a while anyway.

Once the first bank goes I suspect that the rest will follow almost immediately if only for the action that you have reccomended. (not to mention that they all are likely to be in a similar financial position) Obviously all other banks would be cleaned out by depositors shifting their money to the first OBR bank with it's deposit gaurentee. This will create quite a problem for the reserve bank. They cannot put all the banks into OBR unless are in a state that requires it and presumably have accepted their fate. To do so would create a hell of a legal stoush.

If the bank is sold to a third party after restructuring who gets the proceeds of the sale?

Any investment is a risk....some obviously so. Simple if you do not like the contract leave.

This is not an investment it is a bank deposit and does not carry the risks and rewards of an investment. When you deposit money in a bank they promise to give it back with interest.

It is not unreasonable to expect that the depositors should be made fully aware of all these fish-hooks. Maybe Interest .co could fully research and lay out clearly, the full provisions of of how a banking colapse will be handled in NZ. We don't seem to have anything like this from the crooks in government.

What are you talking about Chris-M

A bank deposit is definately an investment... although a pretty poor one.

You lend the bank $x, often with top ups, and they use it for their business, and promise to pay you a yield based on the amount you lent them, with the surrender of the whole loan if you request it.

Just the same as shares, private loans, investment accounts, you give them $X, they promise a yield based on your investment, and that you can get back your investment under conditions in the loan documents. (eg shares, when the company offers to buy back)

All investments involve OPM and yield. Therefore there is always a risk, and so it is the _investors_ money and the _investors_ responsibility to inform themselves about _their_ investment. Just get that through your head...because it is their property, their money, the responsibility is on them to protect _their_ asset. that's what asset ownership is, the requirement of responsibility....lose that and they just become a proxy for those who take the responsibility.

The bank (etc) responsibility is not to misrepresent themselves when asked, and to have the information available as best possible.

a) wtf is interest? it is a profit on your capital.

b) if you dont like the risk, take your money out.

c) Stop being a parasite and expecting others to cover your loss.

d) read the docs for your investment.

e) if you want answers pay for them.

Chris I'm not really understanding this repeated "stolen" comment I keep hearing. I personally spread my risk around investments and banks, and see banks as nothing special. If I'm dumb enough to invest too much in a bank that falls over, I expect myself and bond holders to be the next to lose some or all of my "investment with them i.e. after the shareholders are wiped out. Theyre not Govt guaranteed, they are low risk comparitive to others, but nonetheless a risk - I do not expect taxpayers to bail out my bad decsion unless it is stated as Govt guaranteed.

It is stolen because what I am being told here is that the depositors will take a hair cut, the bank will carry on and then be sold to another party. That is there will be a lot of equity left in the bank that will not be available to repay the loss to the depositors. This is not the way any bankrupcy is handled. Debtors have full access to all assets untill they are extinguished.

While you could argue that the bank has no equity left and the new owners investment is the recapitalising of the bank, the example of the Rural Bank illustrates that this sort of process may be severly flawed at best and open to outright corruption at worst. I think that the creditors should be given first refusal on purchasing the bank as a counter to this. The typical proportion of the equity to deposits in banks is so low that I suspect that their haircut would only have to be marginally increased to equate to what a new owner would contribute. This would be a fair measure to counter sloppy handling or abuse of the process.

It is not stolen. As an investor you enjoyed interest on your investment that carried risk, you chose to accept that by leaving money in the bank.

My understanding is (please correct me if not),

The chequeing side of the bank carries on trading so we get to eat and our economy and society does not implode in the event of a insolvency.

The investment side of the bank will be insolvent, depositors hsould lose all their money. So say its assets (mortgages, share etc) on paper have gone down 30%, ergo those assets get sold on (ie mortgages) and the money coming back gets returned to you NET of the losses.

If you dont like that, then leave.

Ok thanks Chris - I now understand your thinking

I've put my $ in Australian banks, - in Australia.

There you have a govt guarantee up to $100k per person, per bank. So just spread it over a few banks and you're covered.

Mark L., where did you get the $100k number from?

Sorry, looks like $250k. I thought they lowered it, - well they did - from 1mill. but not to $100k as i thought. And thats $250 per person so joint accounts are covered to half a mill.!

True.

I am sure quite a few people have transferred their savings to Oz. No wonder why the NZ Govt and the NZ banks are not particularly enthusiastic about informing people about the OBR policy.

Had a chat with a decent young bloke at the CBA in Sydney. He questions whether the garauentee would apply to non Australians and said that it may be garaunteed, but you may have to wait an awfully long time to get it all back and in an emergency it can all be changed in the course of an overnight meeting of the government. The message seems to be you cant trust or rely on anything.

I kind of wondered on that. There are no votes to be made and indeed probably lost by guaranteeing foreign funds unless domestic funds are already 100% paid out. Even then the OZ tax payer would be paying so I cant see how that's saleable politically. " we need to tax our over-streched ozzies more so NZers get their money back"......yeah right.

I am all for that. I would love to get our banks back from them also.

Still may be worth opening a couple of accounts over there with a few thousand in them. To stop them closing due due to inactivity you would need to regularly automatically circulate funds between them. Then if things start looking dodgey here you could quickly shift cash out of the country without the delay of setting up accounts.

deflation risk means that it's worth holding onto your money because prices will be cheaper tomorrow.

With inflation, borrow now, buy assets, get income, make profit, pay off the debt, keep the yield.

With deflation, if you borrow now, your house will be worth less tomorrow, you won't get enough revenue from sales because people aren't spending, profit is absent, your principal debt will actually get harder to pay off, result is no or negative effective yield. Doing this makes for very poor investment/capital markets !!!

Problem with stagflation, we have low inflation, so it looks like things are moving, but in reality some areas are inflating in a bad way (eg capital gain turnover in Auckland) that masks poor returns in same market (outside auckland) but that bad inflation masks the overall deflation in the overall market. Dealing with median and spread information, as well as looking for regional/niche outliers, helps identify the problem areas.

and the changeover?

If you buy assets with debt however and pay x2 if not x3 its real worth then in a depression you are wiped out.

"bad returns" indeed, so it looks like ppl are gambling that there is a bigger fool to make a capital gain off.

bound to end well.

When it happens it certainly will be.

I dont think the propsect of deflation ever seriuosly entered the RBNZ debate, parlance or sights .

Wheeler was schooled in a time of inflation , he is a very clever man , but his prejudices are ingrained .

I reckonn the RBNZ were focussing on the wrong numbers and looking in the wrong places ..... a bit like an Irish Catholic priest walking around with his eyes fixated on the heavens above waiting for the second coming .

Inflation will return , but like the second coming we dont know when .

As someone who is meticulous about our household budget , what I did see was there was NO INFLATION impacting on us as a household , for example :-

- our weekly grocery bill did not go up in 2 years

- our massive new TV cost less than the one we bought 20 years ago ( that was a full 2 weeks wages back then with tarriff protecvtion and import duties and monopoly pricing )

- our clothing spend halved between 2010 and 2014.

- a secondhand car cost about half of what it cost us 7 years ago .

- Our Municpal Rates came down when the supercity was cobbled together

- Now our petrol and diesel account has come down by abourt $100 a month

We have never had it so good

Personally I think the comments by the right VIPs" (the deluded, self proclaimed very important persons) on such things as good v bad deflation is utter rubbish. Really its just a new take on "things are going to be bad because of all the money printing". When it reality it is a symptom and not the cause.

Re:#1 -

I think there are some deeply structural elements to the waves of deflation now racing around the globe, both because of new technology and ageing populations.

Should that encourage central banks to cut interest rates to zero and start printing money to stave off deflation? The US, Japan and Europe chose that path and it has generated enormous asset price deflation (sic).

Bernard I think you mean asset inflation? - well I certainly think the Mrs Watanabes if not the BoJ via its agents would be seeking such an outcome.

The Ministry of Finance just reported that Japan bought JPY 657 billion (over $5.6 billion) of foreign stocks last week. That is the biggest weekly purchase of foreign equities since records began in 2001. The huge size of the purchases- more than double the average size of recent weekly purchases - appears to have been 'spent' on European stocks (and perhaps some Chinese). It is unclear whether this is direct buying by the banks as a proxy for The BoJ's quid pro quo or merely front-running this week's exuberance from Draghi by Mrs.Watanabe now that her Swissy trade exploded... Read more

Stephen

Thanks for spotting my typo/transposition. I have corrected.

cheers

Bernard

#6 - Hoping that this government will give any thought to middle class needs is as likely as it including "the common good" in its rhetoric or thinking.

1. Good deflation or bad deflation?

Could be a bit of both. Either way one thing might address it. Raising wages and salaries would share the benefit of productivity gains and encourage people to take their hands out of their pockets. As things are at the moment wealth has accumulated in the pockets of a minute number of people, while the bulk of the populace have gone backwards. This seems to be happening as a result of both ecconomic management that is powerfully skewed in favour of the mega wealthy, and the fruits of increased productivity not being shared equitably. I would like to think that this was unsustainable in the long run but it is concievable that we could all end up effectively slaves to a handful of people. It has happened before in history and we seem to be well on our way to this now. Looking to history these sorts of situations end up with some form of revolution. The silly thing is that while the mega rich may feel great at having cleaned up all the money on the monopoly board, they may well be better off and certainly no worse off if the masses had more wealth, could afford decent housing and enjoy a reasonable level of material consumption. That is, the ecconomy would grow and everybody would benefit. Otherwise the mega rich will hang onto more and more of the weath and strangle the ecconomy.

With wealth equitably shared, ultimately we will reach the point when everybody can enjoy all the material goods that they can reasonably want. At that point (possible to some extent before) increasing productivity must be reflected in reduced working hours if everybody is to be meaningfully employed. In this environment we certainly do not need an increasing population (apart from the unsustainable environmental pressures from the all ready too large population ).

All this points to the fact that our so called leaders need to have a much deeper and longer term look at what they should be doing insteading of racing round like headless chooks with knee jerk reactions to a series of crises of their own making.

What exactly is the evidence base for the statement "wealth has accumulated in the pockets of a minute number of people while the bulk of the populace has gone backwards"?

You want equitable sharing of wealth. What share of the wealth created by your labour do you think it would be equitable to award to me?

Not knowing what your personal circumstances are, how can I possibly answer that?

Perhaps it isn't so much a deline in labour but a compounding effect of finance and other sources of unearned income. Isn't going to get better if so.

not about material wealthy for everyone.... for them who "arrive" it's about power. eg the 10 table

You will still be buying your cattle drench, fuel for your car a new TV when the old one blows up etc. It won't be that bad, as long as you can manage your debts.

In reply to " The silly thing is that while the mega rich may feel great at having cleaned up all the money on the monopoly board, they may well be better off and certainly no worse off if the masses had more wealth, could afford decent housing and enjoy a reasonable level of material consumption. That is, the ecconomy would grow and everybody would benefit."

Assumes that they want other people to benefit. they do not waqnt other people to benefit, wealth gives other people options and ideas above their station. very dangerous to assume others are reasonable or want goals the same as yours.

I get the sense of a herd mentaility .........and a bit of unease about deflation

Lets face it , we in NZ have got out of jail free in the world economic crisis.

We have the best GDP growth in the OECD , but lets not fool oursleves and think we are smart-arses with tons of hubris .

Rebuilding a whole earthquake ruined city with insurance money in a tiny country of 4 million and immigration of 1000 new faces a week has put our economy on steroids .

Take these factors out of the equation , and we are likely to have been in a not-so-good-space.

The thing about the prospect of deflation , is that logically, armed with this knowledge , we will all want to pay down debt as quickly as possible , and stay out of new debt .

Problem is , if we all do that then demand collapses and deflation is a sure thing .

House building in Auckland , and Chch rebuild will keep demand strong and keep us out of trouble .......... for now

In the meantime I am going along with the herd on this , taking on no new debt and saving , saving , saving our monthly surplus.

I dont know why I am doing this because we dont want for anything , but its instinctive to do what the rest of the herd is doing and I too have a sense of unease about things when they get to be too-good-to-be-true .

And lets face it , we are going gangbusters.

We have never had it so good , and frankly personally with no debt , we have never had as much money or as much surplus as we have now , not in my entire life.

Maybe we I are getting old and life has smacked us around a bit , but I get the feeling this is too good to last .

Perhaps, Bernard, the next intake re- world-wide-ponzi isn't stepping up to the plate? Hence deflation. The large swathes of un-employed youth throughout the western economies, and the over-indebted/over-taxed and out of breath middle classes just dont have it any more.

The broad cross-section of commodities suffering ongoing price reductions arent through new technology or new discoveries offering new abundance. In fact in many cases the costs of provision exceed by some margin the returns being offered. Oil is peculiar in its association with financial shenanigans, whereby more money is pumped than product for a great number of swing producers.

What we are witnessing is bad deflation; a collapse of demand (not want- demand is want in association with means).

The train is leaving the tracks!

#6. That correlates nicely to the general world decline in population growth since it peaked at 2.08% in 1961, it is now under 1% and still falling. That is an energy event not a bloody TV sideshow.

Inflation only suits crooks and fools. All thrift is good.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.