Here's my summary of the key issues from over the weekend that affect New Zealand, with news of big job gains in America.

From data out on Saturday morning, US employment levels improved substantially more than markets were expecting in February.

In fact, the American unemployment rate fell to its lowest level in seven years and will encourage the Federal Reserve to raise interest rates - probably in June - on a path back to 'normal'.

This data had an electric impact on both the bond and currency markets, raising yields and the US dollar sharply. Stock markets dropped, fearing the coming rate hike - another taper tantrum?

Perhaps missed in the surprise was that wage growth was not as strong as first thought in earlier surveys although the jump in hours worked - and therefore take-home pay - was the largest since 1998.

In Europe, Greece sent its euro zone partners an expanded list of its proposed reforms over the weekend, but EU and ECB officials tightened their stance of more funding for embattled country.

In China, data out over the weekend showed their exports jumped 48% in February from a year earlier - the strongest in nearly five years and comfortably beating market expectations - while imports slipped 20% on lower oil costs. That produced a record trade surplus of US$61 bln for the month. The jump in exports is because of rising demand from the US.

A growing American economy is probably the only thing that can turn around China's slowing growth.

The UST 10yr yields raced higher in New York after the non-farm payrolls report to 2.25%. That's a +13 bps gain in one day. Interest rate markets now seem convinced the Fed will raise rates by mid-year. New Zealand swap rates will probably respond today. Maybe mortgage rates are now as low as we are going to see them in this cycle.

Interestingly, CDS spreads for investment grade Australasian corporate bonds - essentially the risk premium local banks pay for their debt - fell to their lowest level since January 2008, at 69 bps on Friday. In March 2009 their reached a record 442 bps.

The crude oil price also fell on Friday and is now under US$50/barrel and the Brent crude price is now under US$60/barrel. US rig counts fell again last week but rose internationally.

The gold price fell even harder and starts the week at US$1,164oz down more than US$35/oz.

The New Zealand dollar starts today substantially lower against a surging US dollar at 73.6 US¢ - that is down -2½¢ from Thursday - at 95.2 AU¢, and the TWI is down to 78.2.

If you want to catch up with all the local changes on Friday, we have an update here.

The easiest place to stay up with event risk is by following our Economic Calendar here »

Daily exchange rates

Select chart tabs

9 Comments

Economists drive through the passage of time looking through the rear vision mirror. What they see in the mirror are all the data, graphs and charts informing them what the economy has been doing.

While they are busy looking in the rear view mirror they do not see the big hole in the road ahead called the Global Financial Crisis.

These same economists are now analysing the same data to see if there is deflation ahead or not. They are not sure.

Have they seen the real signs, just like ordinary people see?

When your average person drives through the passage of time, this is what they see:

Initially they see lots of second hand shops and lots of repair shops. Not much is throw away. There are repair shops to mend just about anything, from washing machines to fridges to stereos to radios and much more.

As they go further along through time they see the repair and second hand shops all starting to close. As these shops close they also notice an increase in the amount of rubbish being collected.

Of course everyone knows the reason for this is “Productivity”. It is becoming cheaper to manufacture things and prices have become so low it is no longer cost effective to repair these items. Best to just dump them and buy a new one.

“But wait” for decades economists have been saying how good “Productivity” is,

But

Productivity = reduced costs = lower prices – And this is great, so they say

And Deflation also = reduced costs – And this is real Bad, so they say

If prices fall because of productivity gains this is good and everyone can buy more.

Now they tell us falling prices = deflation and this is bad because people will put off buying

Boy what a crazy mixed up lot these economists are.

The point of all this of course is to point out that we have had deflation for decades, its just that we haven’t noticed. And the reason we haven’t noticed is because of our ponzie money scheme with its artificial inflation rigging.

Just to remind people that inflation is the constant and exponential falling value of our money. You have to keep paying more for the same thing because your money is loosing value.

And “Yes” you can have Inflation and Deflation at the same time.

You can become more efficient and produce goods more cheaply, but the price does not fall because the value of your money is falling faster. The Global Financial Crisis has exposed deflation that has been with us for decades. Their ponzie scheme has been exposed.

Deflation has been with us for decades and is not going away. The only question remaining is “Who will reap the benefits of this deflation”

PS: I hope you also read this Steven

I should add that in the period leading up to the GFC inflation was much higher that everyone realise. We had, say 5% deflation (see above) and, say, 8% inflation. The net result was that the data showed inflation to be 3%.

This data had an electric impact on both the bond and currency markets, raising yields and the US dollar sharply. Stock markets dropped, fearing the coming rate hike - another taper tantrum?

There are two glaring, but little discussed factors impacting upon the pricing of global securities.

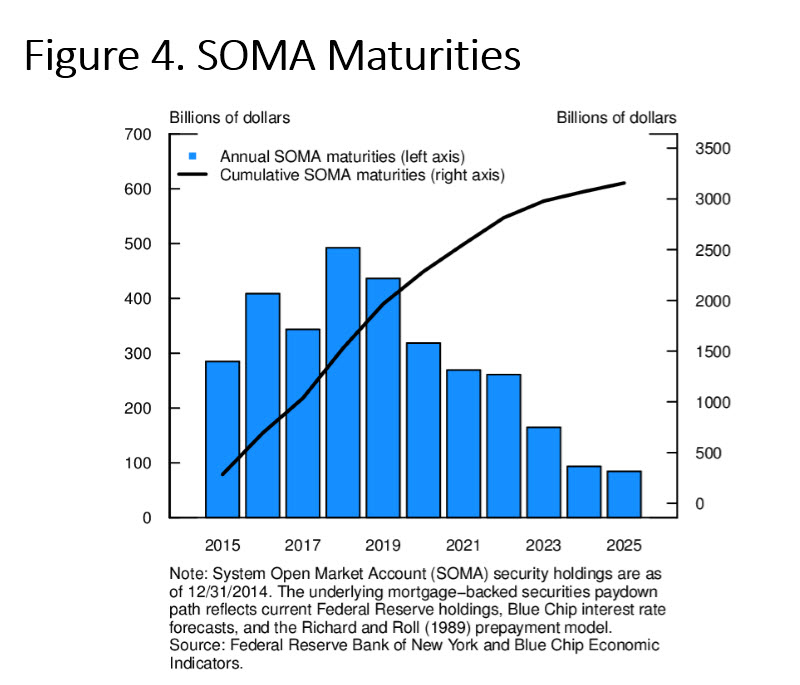

Finally, with regard to balance sheet normalization, the FOMC has indicated that it does not anticipate sales of agency mortgage-backed securities, and that it plans to normalize the size of the balance sheet primarily by ceasing reinvestment of principal payments on its existing securities holdings when the time comes As illustrated in figure 4, cumulative repayments of principal on our existing securities holdings from now through the end of 2025 are projected to be about $3.2 trillion. As a result, when the FOMC chooses to cease reinvestments, the size of the balance sheet will naturally decline, with a corresponding reduction in reserve balances. Read more

{kind=link}

And by implication a growing understanding that an acute shortage of USD funding is evolving due to global central bank policy divergences.

The decline in the cross currency swap basis across most USD pairs in recent months is raising questions regarding a shortage in dollar funding. The fx basis reflects the relative supply and demand for dollar vs. foreign currency funds and a very negative basis currently points to relative shortage of USD funding or relative abundance of funding in other currencies. Such supply and demand imbalances can create big shifts in the fx basis away from its actuarial value of zero. Figure 1 shows that the dollar fx basis weighted across eight DM and EM currencies, declined significantly over the past year to its lowest level since mid 2013, although it remains well above the lows seen during the depths of the Lehman or the Euro debt crisis. Read more

NZD/USD 5yr FX basis swap quotes have fallen significantly over recent months. At the margin NZ foreign wholesale bank funding costs will rise.

Fantastic news to listen to while enjoying my latte this morning. Ben Bernanke is an unsung hero of the world. QE vs austerity - USA vs Eurozone - Bernanke has won.

Only 10 minutes have been played so far, hard to say he has won. There is the matter of a few $trn to sort out.

If it took 6 or 7 years to pump trillions into the economy how many years will it take to remove it?

Courtesy Stephen Hulme above - the answer to your question is

A 10 year PLAN

cumulative repayments of principal on our existing securities holdings from now through the end of 2025

Depends.

Since it isnt actual printing, as quickly as you want or the economy can stand it, in theory, LOL...

If on the other hand you see a perma-recession caused by being in a post-peak oil world, well never.

6~7 years and yes we are not out of it, arguably its actually getting worse.

Or is there anyone who things the world now looks a lot better than say the last 4 years?

.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.